Вам также может понравиться

- Corporate Finance Model AnswerДокумент3 страницыCorporate Finance Model AnswersrikanthОценок пока нет

- Session 10-11, CVP Analysis - PPTX (Repaired)Документ35 страницSession 10-11, CVP Analysis - PPTX (Repaired)Nikhil ChitaliaОценок пока нет

- Financial StatementДокумент36 страницFinancial StatementKopal GargОценок пока нет

- Chapter 2-Descriptive StatisticsДокумент18 страницChapter 2-Descriptive StatisticsAyn RandОценок пока нет

- Corporate Finance-Assignment June 2017 PDFДокумент2 страницыCorporate Finance-Assignment June 2017 PDFnbala.iyerОценок пока нет

- Corporate Finance - Assignment September 2017 isuTxyQsX4 PDFДокумент3 страницыCorporate Finance - Assignment September 2017 isuTxyQsX4 PDFA Kaur MarwahОценок пока нет

- HRM Case and Solution On JAДокумент13 страницHRM Case and Solution On JAAshhab Zaman RafidОценок пока нет

- Assignment of Corporate FinanceДокумент3 страницыAssignment of Corporate FinanceSakshi PanwarОценок пока нет

- Assignment DMBA103 MBA 1 Set-1 and 2 Mar 2022Документ3 страницыAssignment DMBA103 MBA 1 Set-1 and 2 Mar 2022Assignment SolveОценок пока нет

- Developments in International Safety Glass Test Method StandardsДокумент30 страницDevelopments in International Safety Glass Test Method StandardsKedar A. MalusareОценок пока нет

- Waiting Time ParadoxДокумент9 страницWaiting Time ParadoxmelanocitosОценок пока нет

- Assignment - Corporate Finance Capital Budgeting Case Study Project Details Year Project A Project BДокумент4 страницыAssignment - Corporate Finance Capital Budgeting Case Study Project Details Year Project A Project BAnshum SethiОценок пока нет

- Corporate FinanceДокумент11 страницCorporate FinanceShamsul HaqimОценок пока нет

- FINS3625 Case Study Report Davy Edit 1Документ15 страницFINS3625 Case Study Report Davy Edit 1DavyZhouОценок пока нет

- Sampling and ItДокумент14 страницSampling and ItNouman ShahidОценок пока нет

- Management Accounting Chapter 4Документ53 страницыManagement Accounting Chapter 4yimer100% (1)

- Sem 2 Question Bank (Moderated) - Financial ManagementДокумент63 страницыSem 2 Question Bank (Moderated) - Financial ManagementSandeep SahadeokarОценок пока нет

- Management Accounting Exam Paper August 2012Документ23 страницыManagement Accounting Exam Paper August 2012MahmozОценок пока нет

- MR - Ksenou L&T PrecastДокумент53 страницыMR - Ksenou L&T PrecastHarssh ShahОценок пока нет

- CF Assignment 1 Group 4Документ41 страницаCF Assignment 1 Group 4Radha DasОценок пока нет

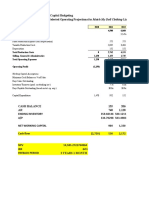

- New Heritage Doll Company: Capital Budgeting Exhibit 1 Selected Operating Projections For Match My Doll Clothing Line ExpansionДокумент9 страницNew Heritage Doll Company: Capital Budgeting Exhibit 1 Selected Operating Projections For Match My Doll Clothing Line ExpansionIleana StirbuОценок пока нет

- QTIA Report 2012 IQRA UNIVERSITYДокумент41 страницаQTIA Report 2012 IQRA UNIVERSITYSyed Asfar Ali kazmiОценок пока нет

- Valuation of Bonds and SharesДокумент45 страницValuation of Bonds and SharessmsmbaОценок пока нет

- Corporate Finance Assignment PDFДокумент13 страницCorporate Finance Assignment PDFسنا عبداللهОценок пока нет

- Management Accounting MAY 2013Документ21 страницаManagement Accounting MAY 2013MahmozОценок пока нет

- Corporate FinanceДокумент4 страницыCorporate FinanceSaurabh Singh RawatОценок пока нет

- Waiting Line ManagementДокумент19 страницWaiting Line ManagementStephAlvaradoBlanzaОценок пока нет

- Assignment Corporate FinanceДокумент3 страницыAssignment Corporate FinanceRose Abd Rahim50% (2)

- Free Cash FlowДокумент31 страницаFree Cash FlowKaranvir GuptaОценок пока нет

- Corporate Finance (United Pigpen) AssignmentДокумент1 страницаCorporate Finance (United Pigpen) AssignmentPhilip HabersaatОценок пока нет

- New Heritage Doll CompanyДокумент8 страницNew Heritage Doll CompanyKDОценок пока нет

- Assignment 1Документ3 страницыAssignment 1Abbaas AlifОценок пока нет

- MA Exam Paper May 2010Документ23 страницыMA Exam Paper May 2010MsKhan0078Оценок пока нет

- SYBCom Semster III Business Economics 2014-15Документ56 страницSYBCom Semster III Business Economics 2014-15ginga716Оценок пока нет

- Assignment No 2Документ3 страницыAssignment No 2Adeel AwanОценок пока нет

- Chapter 24. Tool Kit For Portfolio Theory, Asset Pricing Models, and Behavioral FinanceДокумент22 страницыChapter 24. Tool Kit For Portfolio Theory, Asset Pricing Models, and Behavioral Financetreeken2Оценок пока нет

- Research QuestionsДокумент37 страницResearch QuestionsAmmar HassanОценок пока нет

- Management AccountingДокумент17 страницManagement AccountingAndi RavОценок пока нет

- Assignment Inferential Statistics 1Документ5 страницAssignment Inferential Statistics 1maudy octhalia d4 kepОценок пока нет

- Business Statistics Etf1100 Notes Business Statistics Etf1100 NotesДокумент56 страницBusiness Statistics Etf1100 Notes Business Statistics Etf1100 NotesIshan MalakarОценок пока нет

- New Heritage Doll CompanyДокумент11 страницNew Heritage Doll CompanyLightning SalehОценок пока нет

- Ch05 Mini CaseДокумент8 страницCh05 Mini CaseSehar Salman AdilОценок пока нет

- Corporate Finance AssignmentДокумент4 страницыCorporate Finance AssignmentShamim NoorОценок пока нет

- Management Accounting Exam Paper May 2012Документ23 страницыManagement Accounting Exam Paper May 2012MahmozОценок пока нет

- Bond ValuationДокумент12 страницBond ValuationvarunjajooОценок пока нет

- HCL TechnologiesДокумент10 страницHCL TechnologiesDwi Setiadi Nugroho - VTIОценок пока нет

- Module 4 Inferential Statistics PDFДокумент25 страницModule 4 Inferential Statistics PDFQueency DangilanОценок пока нет

- Valuation of Bonds and Shares: Problem 1Документ29 страницValuation of Bonds and Shares: Problem 1Sourav Kumar DasОценок пока нет

- Carlos Hilado Memorial State College: College of Business Management and AccountancyДокумент14 страницCarlos Hilado Memorial State College: College of Business Management and AccountancyMa.Cristina JulatonОценок пока нет

- Et Iso 12543 2 2011Документ11 страницEt Iso 12543 2 2011freddyguzman3471Оценок пока нет

- Irr and NPVДокумент13 страницIrr and NPVAbin VargheseОценок пока нет

- Heritage Dolls CaseДокумент8 страницHeritage Dolls Casearun jacobОценок пока нет

- Corporate Finance ProjectДокумент13 страницCorporate Finance ProjectAbhay Narayan SinghОценок пока нет

- Corporate Finance Assignment 1Документ3 страницыCorporate Finance Assignment 1tientran91Оценок пока нет

- Amtrak Case SummaryДокумент1 страницаAmtrak Case SummarySteve SmithОценок пока нет

- Engineering Economics: Rate of Return AnalysisДокумент29 страницEngineering Economics: Rate of Return AnalysisEkoОценок пока нет

- Capital Budgeting April2021Документ28 страницCapital Budgeting April2021MikhailОценок пока нет

- Practical Task 3 PROBLEM SOLUTIONДокумент7 страницPractical Task 3 PROBLEM SOLUTIONTanya PribylevaОценок пока нет

- Solution - Problems and Solutions Chap 10Документ6 страницSolution - Problems and Solutions Chap 10سارة الهاشميОценок пока нет

- Stock MarketДокумент47 страницStock MarketswastikОценок пока нет

- Corporate Restructuring Assignment #6Документ7 страницCorporate Restructuring Assignment #6Natt NiljianskulОценок пока нет

- CR2013Assignment#5-ICS Recovery Fund - NattДокумент11 страницCR2013Assignment#5-ICS Recovery Fund - NattNatt NiljianskulОценок пока нет

- Corporate Restructuring Assignment #5Документ9 страницCorporate Restructuring Assignment #5Natt NiljianskulОценок пока нет

- 2013 Registration Confirmation Calendar For MEXT Students: April OctoberДокумент1 страница2013 Registration Confirmation Calendar For MEXT Students: April OctoberNatt NiljianskulОценок пока нет

- Case - Capital BudgetingДокумент2 страницыCase - Capital BudgetingRenz PamintuanОценок пока нет

- Abandonment Option (Contd..)Документ9 страницAbandonment Option (Contd..)Pranav PОценок пока нет

- Real Estate GlossaryДокумент52 страницыReal Estate GlossaryJustine991Оценок пока нет

- Dhaka Ashulia Pre Feasibility ReportДокумент332 страницыDhaka Ashulia Pre Feasibility Reportsayed126Оценок пока нет

- Innovation Portfolio Management Balancing Value and RiskДокумент18 страницInnovation Portfolio Management Balancing Value and Riskvineetagr80100% (1)

- Country Risk Assessment: See Answer Here Expertanswer - OnlineДокумент1 страницаCountry Risk Assessment: See Answer Here Expertanswer - OnlineM Bilal SaleemОценок пока нет

- Chapter 6 KT322HДокумент25 страницChapter 6 KT322HDuong Gia Linh B2112435Оценок пока нет

- Alemayehu MetallicДокумент20 страницAlemayehu Metallicmuluken walelgnОценок пока нет

- QuestionsДокумент10 страницQuestionsYat Kunt ChanОценок пока нет

- ch11 Fin202Документ51 страницаch11 Fin202Nguyễn Thanh Nhàn K16Оценок пока нет

- Costs: PM (25 Weeks Hr/Week $/HR) Staff (25 Weeks Hr/week $/HR) Outsourced Software and ServicesДокумент2 страницыCosts: PM (25 Weeks Hr/Week $/HR) Staff (25 Weeks Hr/week $/HR) Outsourced Software and Servicesthorn lewarsОценок пока нет

- 041924353041-Review Chapter 31Документ6 страниц041924353041-Review Chapter 31Aimé RandrianantenainaОценок пока нет

- Chapter 2: Transportation PlanningДокумент12 страницChapter 2: Transportation PlanningISABIRYE BAKALIОценок пока нет

- Financial Management. EBS ML. 4 Course Students. Case Study. Phuket Beach Hotel. Valuing Mutually Exclusive Capital Projects. QuestionsДокумент33 страницыFinancial Management. EBS ML. 4 Course Students. Case Study. Phuket Beach Hotel. Valuing Mutually Exclusive Capital Projects. QuestionsEric NadalОценок пока нет

- ROI and The ArchitectДокумент15 страницROI and The ArchitectkinoaurumОценок пока нет

- Investment DetectiveДокумент25 страницInvestment DetectiveTestОценок пока нет

- Capital Budget Impact in Banking SectorДокумент85 страницCapital Budget Impact in Banking SectorVickram JainОценок пока нет

- Edoc - Pub - Jaiib Made Simple Paper 2 PDFДокумент148 страницEdoc - Pub - Jaiib Made Simple Paper 2 PDFSindhu Arauvinth RaajОценок пока нет

- Assignment MmeiДокумент12 страницAssignment Mmeisheela ShashiitharanОценок пока нет

- NPV: Cortland Manufacturing Company Net Present Value Case AnalysisДокумент1 страницаNPV: Cortland Manufacturing Company Net Present Value Case AnalysisPricelda VillaОценок пока нет

- Risk and Capital BudgetingДокумент51 страницаRisk and Capital BudgetingSanaNaeemОценок пока нет

- N P VДокумент8 страницN P VCatalin Marius SpataruОценок пока нет

- Rizky Chandra Ariesta, Mohammad Sholichan Arif, and Hutami Putri PuspitasariДокумент10 страницRizky Chandra Ariesta, Mohammad Sholichan Arif, and Hutami Putri PuspitasariSholichatul IlmiahОценок пока нет

- Case Study: Aerocomp LTDДокумент12 страницCase Study: Aerocomp LTDWahidОценок пока нет

- Original Principles of Managerial Finance Brief 8Th Edition by Chad J Zutter Full ChapterДокумент41 страницаOriginal Principles of Managerial Finance Brief 8Th Edition by Chad J Zutter Full Chapteralton.hopper106100% (21)

- FM SMДокумент399 страницFM SMDj babu100% (1)

- Financial Analysis 105-115Документ10 страницFinancial Analysis 105-115deshpandep33Оценок пока нет

- Groupe Ariel - SolutionДокумент6 страницGroupe Ariel - SolutiontrangngqОценок пока нет

- HW 1, FIN 604, Sadhana JoshiДокумент40 страницHW 1, FIN 604, Sadhana JoshiSadhana JoshiОценок пока нет

- Chapter 15 M&A, Takeovers, Corporate Control5Документ22 страницыChapter 15 M&A, Takeovers, Corporate Control5toshiba1234Оценок пока нет