Вам также может понравиться

- Jaiib Module AДокумент25 страницJaiib Module Aeknath2000Оценок пока нет

- 1 - 2018 Introduction To Banking Operations UBA-Day 1 PDFДокумент111 страниц1 - 2018 Introduction To Banking Operations UBA-Day 1 PDFAustinОценок пока нет

- Financial ServicesДокумент46 страницFinancial Servicessunny patwaОценок пока нет

- Indian Financial SysemДокумент14 страницIndian Financial SysemRajat SharmaОценок пока нет

- What Is Financial System?Документ46 страницWhat Is Financial System?Soumya Ranjan SwainОценок пока нет

- Commercial Banking Lending Policies of BanksДокумент47 страницCommercial Banking Lending Policies of Banksrahul8909Оценок пока нет

- 1.IFS and Functions of Merchant BankerДокумент27 страниц1.IFS and Functions of Merchant BankerDr.R.Umamaheswari MBAОценок пока нет

- Features of Cooperative Banks: "One Person, One Vote"Документ68 страницFeatures of Cooperative Banks: "One Person, One Vote"Arpit MalviyaОценок пока нет

- International Trade FinanceДокумент33 страницыInternational Trade FinanceHaji AliОценок пока нет

- Credit Appraisal ProcessДокумент19 страницCredit Appraisal ProcessVaishnavi khot100% (1)

- 1 Bank LendingДокумент56 страниц1 Bank Lendingparthasarathi_inОценок пока нет

- Merchant BankingДокумент14 страницMerchant Bankingamitmali.armОценок пока нет

- Bank of IndiaДокумент15 страницBank of Indiashreyaasharmaa100% (1)

- Credit Management - IIBFДокумент11 страницCredit Management - IIBFteju16sy0% (1)

- Bank Risk AssessmentДокумент52 страницыBank Risk AssessmentWessam IbrahemОценок пока нет

- Week 5.pptx - WatermarkДокумент57 страницWeek 5.pptx - Watermarkkhushi jaiswalОценок пока нет

- Credit Appraisal Process GRP 10Документ18 страницCredit Appraisal Process GRP 10Priya JagtapОценок пока нет

- Basics of Merchant BankingДокумент18 страницBasics of Merchant Bankingsunita prabhakarОценок пока нет

- Commercial Banks1Документ26 страницCommercial Banks1jenal147Оценок пока нет

- Bank Financial Analysis PresentationДокумент24 страницыBank Financial Analysis PresentationlevuthiОценок пока нет

- Finance Specilization: Asst. Professors, MBA Department, Bhagawan Mahavir College of Management, SuratДокумент85 страницFinance Specilization: Asst. Professors, MBA Department, Bhagawan Mahavir College of Management, Suratpravesh malikОценок пока нет

- CF Unit 2Документ30 страницCF Unit 2Saravanan ShanmugamОценок пока нет

- Financial Services ManagementДокумент43 страницыFinancial Services ManagementChandan ParsadОценок пока нет

- Indian Financial SystemДокумент53 страницыIndian Financial SystemSiddharth BansalОценок пока нет

- Fm302 Management+of+Financial+ServicesДокумент83 страницыFm302 Management+of+Financial+ServicesVinayrajОценок пока нет

- Credit Mgt. - WEBILT - DeckДокумент287 страницCredit Mgt. - WEBILT - Decksimran kaur100% (1)

- Origin and Merchant Banking in IndiaДокумент26 страницOrigin and Merchant Banking in IndiaTeena PoonachaОценок пока нет

- Presentation On Corporate Finance: By: Sunita SasankanДокумент21 страницаPresentation On Corporate Finance: By: Sunita SasankanLauren MontoyaОценок пока нет

- Module 1 - Bank and BankingДокумент23 страницыModule 1 - Bank and Bankingwelcome2jungleОценок пока нет

- Credit RatingДокумент30 страницCredit Ratingtejosh84Оценок пока нет

- FMBOДокумент10 страницFMBOHimani ChavanОценок пока нет

- M BankerДокумент41 страницаM BankerNishi SinghОценок пока нет

- Financial Markets and Institutions BanksДокумент47 страницFinancial Markets and Institutions BanksAntonio GorgijovskiОценок пока нет

- Macro Economics: Institution of Money & Modern EconomicsДокумент36 страницMacro Economics: Institution of Money & Modern EconomicsApeksha ShaniОценок пока нет

- Introduction To BankingДокумент38 страницIntroduction To BankingNusrat papiyaОценок пока нет

- Credit ManagementДокумент29 страницCredit ManagementDipesh KaushalОценок пока нет

- UNIT3Документ37 страницUNIT3lokesh palОценок пока нет

- Merchant BankingДокумент20 страницMerchant BankingDileep SinghОценок пока нет

- Merchantbanking 170302071154Документ38 страницMerchantbanking 170302071154Smitha K BОценок пока нет

- Unit II L2 Money Market InstrumentsДокумент67 страницUnit II L2 Money Market InstrumentsHari chandanaОценок пока нет

- Presented By-Aakriti Gupta Arora Gaurav Singh 94972238253 94972238262Документ71 страницаPresented By-Aakriti Gupta Arora Gaurav Singh 94972238253 94972238262sayedmaruf7866807Оценок пока нет

- Merchant BankingДокумент41 страницаMerchant BankingPooja balwaniОценок пока нет

- Financial RegulatorsДокумент70 страницFinancial Regulatorsanmaya agarwalОценок пока нет

- Sapm Unit 2 Part 1Документ43 страницыSapm Unit 2 Part 1Sushma KumarОценок пока нет

- EPM-3.1 Performance Evaluation of BanksДокумент19 страницEPM-3.1 Performance Evaluation of BanksSandeep Sonawane100% (1)

- Retail Banking: Drivers of Retail Business in IndiaДокумент3 страницыRetail Banking: Drivers of Retail Business in Indiaamar dihingiaОценок пока нет

- Credit Appraisal System of PUNJAB NATIONAL BANKДокумент36 страницCredit Appraisal System of PUNJAB NATIONAL BANKManish Kanwar78% (9)

- Unit 4 - Credit RatingДокумент40 страницUnit 4 - Credit RatingANUSHKA CHATURVEDIОценок пока нет

- Indian Fixed Income MarketДокумент27 страницIndian Fixed Income MarketNitesh GoyalОценок пока нет

- Credit Rating: - Kanika KhuranaДокумент40 страницCredit Rating: - Kanika KhuranaAnunay AroraОценок пока нет

- Depository SystemДокумент36 страницDepository SystemRabia PearlОценок пока нет

- Banking N Session-4 & 5Документ49 страницBanking N Session-4 & 5Vaibhav AggarwalОценок пока нет

- Role of Financial SystemДокумент30 страницRole of Financial SystemAhmed HabibОценок пока нет

- I. Banking-Merchant BankingДокумент25 страницI. Banking-Merchant BankingHanika JulkaОценок пока нет

- MBFS Mod 5Документ20 страницMBFS Mod 5Kiran Kumar S SОценок пока нет

- Corporate BankingДокумент57 страницCorporate BankingSoumya TiwaryОценок пока нет

- FS Mod 7Документ35 страницFS Mod 7sonaОценок пока нет

- Unit-3 Commercial Banking & Retail BanksДокумент97 страницUnit-3 Commercial Banking & Retail BanksAbhikaam SharmaОценок пока нет

- Financial Services Firms: Governance, Regulations, Valuations, Mergers, and AcquisitionsОт EverandFinancial Services Firms: Governance, Regulations, Valuations, Mergers, and AcquisitionsОценок пока нет

- Ecs 12112012Документ6 страницEcs 12112012Abhijit PhoenixОценок пока нет

- Banks Sectorial Credit - SR - 01122022 - Retail-01-December-2022-235836502Документ20 страницBanks Sectorial Credit - SR - 01122022 - Retail-01-December-2022-235836502leoharshadОценок пока нет

- SUBEXLTD 28102021225228 InvestorPresentationДокумент30 страницSUBEXLTD 28102021225228 InvestorPresentationleoharshadОценок пока нет

- Monthly Report Dec 2022-01-December-2022-1527676764Документ5 страницMonthly Report Dec 2022-01-December-2022-1527676764leoharshadОценок пока нет

- 2012 - FRM Part 1 Book No. 11Документ29 страниц2012 - FRM Part 1 Book No. 11leoharshad100% (1)

- SUBEXLTD - Investor Presentation - 01-Feb-22 - TickertapeДокумент37 страницSUBEXLTD - Investor Presentation - 01-Feb-22 - TickertapeleoharshadОценок пока нет

- Sbi Internet Banking FormДокумент3 страницыSbi Internet Banking Formrajandtu93Оценок пока нет

- Excel Formulas and FunctionsДокумент16 страницExcel Formulas and Functionsgoyal.pavan100% (1)

- For The Chole Masala:: MethodДокумент4 страницыFor The Chole Masala:: MethodleoharshadОценок пока нет

- Harshad Doc2Документ2 страницыHarshad Doc2leoharshadОценок пока нет

- Insert An Existing Word Document Into A Master DocumentДокумент1 страницаInsert An Existing Word Document Into A Master DocumentleoharshadОценок пока нет

- 03 2 David GraceДокумент15 страниц03 2 David GraceleoharshadОценок пока нет

- Project ReportДокумент78 страницProject ReportSurendra ShuklaОценок пока нет

- DasbodhДокумент255 страницDasbodhPradeep Shinde67% (3)

- Nism Series IIA Register & Transfer AgentsДокумент103 страницыNism Series IIA Register & Transfer AgentspratikgildaОценок пока нет

- Trade Finance GuideДокумент23 страницыTrade Finance Guideabhishek0902Оценок пока нет

- Excel 2010 FormulasДокумент16 страницExcel 2010 FormulasZaheer Ahmad100% (1)

- San DeepДокумент3 страницыSan DeepleoharshadОценок пока нет

- Deposit Insurance and Credit Guarantee CorporationДокумент5 страницDeposit Insurance and Credit Guarantee CorporationleoharshadОценок пока нет

- Project ReportДокумент78 страницProject ReportSurendra ShuklaОценок пока нет

- Accounting Standard 26Документ7 страницAccounting Standard 26leoharshadОценок пока нет

- Q 1 - Concept of Strategy? AnsДокумент15 страницQ 1 - Concept of Strategy? AnsRohan ShirdhankarОценок пока нет

- Accounting Standard 26Документ7 страницAccounting Standard 26leoharshadОценок пока нет

- Business ModelДокумент5 страницBusiness ModelleoharshadОценок пока нет

- SIP Auto Debit Nov 2011Документ2 страницыSIP Auto Debit Nov 2011leoharshadОценок пока нет

- Difference Between Administration /management: Nature of WorkДокумент3 страницыDifference Between Administration /management: Nature of WorkleoharshadОценок пока нет

- Capital Market (2.1)Документ33 страницыCapital Market (2.1)leoharshadОценок пока нет

- WhitePaperUrbit (ENG) PDFДокумент30 страницWhitePaperUrbit (ENG) PDFTessa HallОценок пока нет

- Roy v. Herbosa 2016Документ4 страницыRoy v. Herbosa 2016kimoymoy7Оценок пока нет

- Tutorial Chapter: Risk and Return: (Answer 12.5%, 20%) (Answer 5.12%, 20.49%) (Answer 0.4, 1.02)Документ19 страницTutorial Chapter: Risk and Return: (Answer 12.5%, 20%) (Answer 5.12%, 20.49%) (Answer 0.4, 1.02)FISH JELLYОценок пока нет

- ACCTG 201 - Financial Accounting & Reporting Part IДокумент17 страницACCTG 201 - Financial Accounting & Reporting Part IRahul HumpalОценок пока нет

- DividendДокумент34 страницыDividendquoteОценок пока нет

- ACTG311 Long Quiz PDFДокумент3 страницыACTG311 Long Quiz PDFKRIS ANNE SAMUDIOОценок пока нет

- Comparative Analysis of Stock Brokers in CHANDIGARH Region - Manjit GogoiДокумент100 страницComparative Analysis of Stock Brokers in CHANDIGARH Region - Manjit GogoiManjit GogoiОценок пока нет

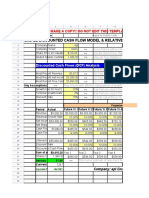

- Simple Discounted Cash Flow Model & Relative ValuationДокумент14 страницSimple Discounted Cash Flow Model & Relative ValuationlearnОценок пока нет

- FR Ind As 102Документ56 страницFR Ind As 102Dheeraj TurpunatiОценок пока нет

- Savita Oil RRДокумент34 страницыSavita Oil RRanushreegoОценок пока нет

- Project 4 - Forecasting Financial StatementsДокумент56 страницProject 4 - Forecasting Financial StatementsTulasi ReddyОценок пока нет

- Module 5 - Cost of CapitalДокумент5 страницModule 5 - Cost of Capitaljay-ar dimaculanganОценок пока нет

- Ia 1BДокумент553 страницыIa 1BTipsywinkieОценок пока нет

- WRD 27e SE PPT Ch16Документ24 страницыWRD 27e SE PPT Ch16Hằng Nga Nguyễn ThịОценок пока нет

- Stock ValuationДокумент18 страницStock ValuationDianne MadridОценок пока нет

- 20 - Segismundo - Gilead - Exercise #1Документ1 страница20 - Segismundo - Gilead - Exercise #1Maria IsabellaОценок пока нет

- BBMF2093 CF Tutorial1Документ55 страницBBMF2093 CF Tutorial1Kar EngОценок пока нет

- Introduction To Security AnalysisДокумент456 страницIntroduction To Security AnalysisSandipan Das100% (2)

- GSIS Law 1Документ13 страницGSIS Law 1Arbie Dela TorreОценок пока нет

- Blackrock PeriodicДокумент2 страницыBlackrock Periodicsameer1987kazi4405Оценок пока нет

- Portfolio Management: Sample Questions and AnswersДокумент11 страницPortfolio Management: Sample Questions and AnswersRam IyerОценок пока нет

- Exercises-Chapter-10 2012 Mba 683 SolutionsДокумент8 страницExercises-Chapter-10 2012 Mba 683 SolutionsAlonzo KotiramОценок пока нет

- Unit 1 To 4Документ102 страницыUnit 1 To 4Durvesh BhavsarОценок пока нет

- Worksheet On Profit and Loss AppropriationДокумент66 страницWorksheet On Profit and Loss AppropriationAditya ShrivastavaОценок пока нет

- How Much Commission Mutual Fund Agent GetsДокумент19 страницHow Much Commission Mutual Fund Agent GetsjvmuruganОценок пока нет

- How To Buy Apple Stock For One DollarДокумент38 страницHow To Buy Apple Stock For One DollarMartin WickhamОценок пока нет

- Inside Financial Markets: Khader ShaikДокумент71 страницаInside Financial Markets: Khader ShaikDaviОценок пока нет

- Income Taxation NotesДокумент14 страницIncome Taxation Notescristiepearl100% (2)

- The Nairobi Stock Exchange (NSE) Sectors ReconfiguredДокумент5 страницThe Nairobi Stock Exchange (NSE) Sectors ReconfiguredPatrick Kiragu Mwangi BA, BSc., MA, ACSIОценок пока нет

- YPF - Petersen ComplaintДокумент30 страницYPF - Petersen ComplaintFilesDotComОценок пока нет