Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- India Ratings Assigns Kanchi Karpooram IND BB-' Outlook StableДокумент4 страницыIndia Ratings Assigns Kanchi Karpooram IND BB-' Outlook StableoceanapolloОценок пока нет

- Solution Manual For Introduction To Finance 17th Edition Ronald W MelicherДокумент36 страницSolution Manual For Introduction To Finance 17th Edition Ronald W Melicherrabate.toiler.vv5s0100% (44)

- SMIC Series C and D Bonds Final Prospectus Dated June 21 2012Документ427 страницSMIC Series C and D Bonds Final Prospectus Dated June 21 2012dendenliberoОценок пока нет

- Part I Introduction To Financial SystemsДокумент57 страницPart I Introduction To Financial SystemsfisehaОценок пока нет

- California Last Will and Testament Will - 2022 - 12 - 25Документ9 страницCalifornia Last Will and Testament Will - 2022 - 12 - 25mmpress009Оценок пока нет

- Asset Liability ManagementДокумент32 страницыAsset Liability ManagementAshish ShahОценок пока нет

- Investment BankingДокумент23 страницыInvestment BankingAnkit BhatnagarОценок пока нет

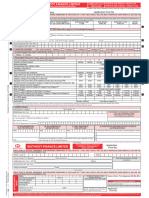

- Anand Rathi Wealth Limited: "AMFI-Registered Mutual Fund Distributor"Документ8 страницAnand Rathi Wealth Limited: "AMFI-Registered Mutual Fund Distributor"NurОценок пока нет

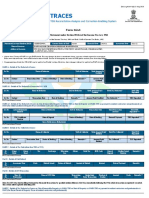

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Документ4 страницыForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961ManjunathОценок пока нет

- Ankit Jain Mba Iv The SemДокумент93 страницыAnkit Jain Mba Iv The Semrahulsogani123Оценок пока нет

- SubPrime Crisis and 911Документ55 страницSubPrime Crisis and 911Eye ON CitrusОценок пока нет

- Asia Amalgamated Holdings Corporation Financials - RobotDoughДокумент6 страницAsia Amalgamated Holdings Corporation Financials - RobotDoughKeith LameraОценок пока нет

- N D B Securities (PVT) LTD, 5 Floor, # 40, NDB Building, Nawam Mawatha, Colombo 02. Tel: +94 11 2131000 Fax: +9411 2314180Документ5 страницN D B Securities (PVT) LTD, 5 Floor, # 40, NDB Building, Nawam Mawatha, Colombo 02. Tel: +94 11 2131000 Fax: +9411 2314180Randora LkОценок пока нет

- Financial and Managerial Accounting 12th Edition Warren Test Bank DownloadДокумент90 страницFinancial and Managerial Accounting 12th Edition Warren Test Bank DownloadAbbie Brown100% (25)

- Corporation Law Reviewer NotesДокумент70 страницCorporation Law Reviewer NotesDaphne Dianne MendozaОценок пока нет

- PWC Guide Foreign Currency 2014Документ168 страницPWC Guide Foreign Currency 2014M.Medina100% (1)

- The Banking Law Reviewer Hot JuristДокумент28 страницThe Banking Law Reviewer Hot Juristgrego centillas100% (2)

- Quicknet Sure Success Series Ugc Net Solved Paper 2006 2017 For Paper IДокумент9 страницQuicknet Sure Success Series Ugc Net Solved Paper 2006 2017 For Paper IYousaf JamalОценок пока нет

- Application Form2024Документ22 страницыApplication Form2024anandhrock123Оценок пока нет

- Nido Home Finance LimitedДокумент640 страницNido Home Finance LimitedchhedamalayОценок пока нет

- Chapter 10 - Cash ManagementДокумент33 страницыChapter 10 - Cash ManagementHazel BorboОценок пока нет

- Valuation of SecuritiesДокумент4 страницыValuation of SecuritiesSaurabh KumarОценок пока нет

- Answers To The Most Frequently Asked Questions Concerning The First Application of The International Financial Reporting Standard 9 - Ifrs 9Документ23 страницыAnswers To The Most Frequently Asked Questions Concerning The First Application of The International Financial Reporting Standard 9 - Ifrs 9XОценок пока нет

- Issue of Capital Rules 2001Документ3 страницыIssue of Capital Rules 2001Al NahiyanОценок пока нет

- Credit and CollectionДокумент129 страницCredit and CollectionKim Ritua - Tabudlo40% (5)

- What Are Financial Markets?: Key TakeawaysДокумент2 страницыWhat Are Financial Markets?: Key Takeawayskate trishaОценок пока нет

- Theoretical Frame WorkДокумент23 страницыTheoretical Frame WorkVikram SingОценок пока нет

- The Great Taking PDFДокумент9 страницThe Great Taking PDFfather.mckenzie.twitterОценок пока нет

- Isaac Schwartz Hidden in Plain SightДокумент28 страницIsaac Schwartz Hidden in Plain SightValueWalk100% (1)

- 2019form - RevGIS - NonStock - Updated For Year 2020Документ6 страниц2019form - RevGIS - NonStock - Updated For Year 2020Joana Saquing100% (1)