Вам также может понравиться

- Russell 2000 Value Membership ListДокумент18 страницRussell 2000 Value Membership ListSatyabrota DasОценок пока нет

- C. CIR V PhilAm Accident G. R. No. 141658. March 18, 2005Документ2 страницыC. CIR V PhilAm Accident G. R. No. 141658. March 18, 2005Chino SisonОценок пока нет

- Understanding Procurement Law and ProcessДокумент126 страницUnderstanding Procurement Law and ProcessJenny Bascuna100% (2)

- High Fructose Corn Syrup Causes Mouth SoresДокумент8 страницHigh Fructose Corn Syrup Causes Mouth SoresA Ali Khan100% (1)

- An Introduction To Airline EconomicsДокумент271 страницаAn Introduction To Airline Economicsavcs175% (4)

- Internal Rate of Return - IRR - CalculatorДокумент3 страницыInternal Rate of Return - IRR - Calculatorapi-3809857Оценок пока нет

- Class 17 - Dabhol Case Study PDFДокумент28 страницClass 17 - Dabhol Case Study PDFBaljeetSinghKhoslaОценок пока нет

- New Cerc NormsДокумент18 страницNew Cerc Norms123harsh123Оценок пока нет

- Thermal Power Tariff Calculation MethodologyДокумент15 страницThermal Power Tariff Calculation Methodologymanishxlri100% (1)

- Quezon Coal Plant Case StudyДокумент74 страницыQuezon Coal Plant Case StudyVyacheslavSvetlichnyОценок пока нет

- Renewable Energy Guideline On Biomass and Biogas Power Project Development in IndonesiaДокумент204 страницыRenewable Energy Guideline On Biomass and Biogas Power Project Development in IndonesiaMaryati DoankОценок пока нет

- Financing Renewable Energy - Green Finance and Innovative SolutionsДокумент29 страницFinancing Renewable Energy - Green Finance and Innovative SolutionsADBI EventsОценок пока нет

- Capital Budgeting: Unit - 1Документ31 страницаCapital Budgeting: Unit - 1RajapriyaОценок пока нет

- Deloitte - Establishing The Investment CaseДокумент14 страницDeloitte - Establishing The Investment Casejhgkuugs100% (1)

- Investment and Operation Cost Figures - Electricity Generation VGB 2011-2011-912-0054-01-EДокумент8 страницInvestment and Operation Cost Figures - Electricity Generation VGB 2011-2011-912-0054-01-EberanoshОценок пока нет

- Energy Audit of Auxiliary Power Consumption: Atar Singh Dy. Director Npti FaridabadДокумент27 страницEnergy Audit of Auxiliary Power Consumption: Atar Singh Dy. Director Npti FaridabadHiltonОценок пока нет

- (JICA - S) Renewable Sector Cooperation in Indonesia 2018Документ5 страниц(JICA - S) Renewable Sector Cooperation in Indonesia 2018haqiОценок пока нет

- Interview With GMRДокумент8 страницInterview With GMRAnupamaa SinghОценок пока нет

- Renewable energy targets in 2022: A guide to designОт EverandRenewable energy targets in 2022: A guide to designОценок пока нет

- Coal-Fired Power Plant Heat Rate Improvement Options, Part 2 - PowermagДокумент11 страницCoal-Fired Power Plant Heat Rate Improvement Options, Part 2 - PowermagRavi SatyapalОценок пока нет

- McKinsey Energy Insights Global Energy Perspective 2019 Reference Case SummaryДокумент31 страницаMcKinsey Energy Insights Global Energy Perspective 2019 Reference Case SummaryOkwudiliОценок пока нет

- Improving Skills for the Electricity Sector in IndonesiaОт EverandImproving Skills for the Electricity Sector in IndonesiaОценок пока нет

- Impact of Ifrs Power and UtilitiesДокумент36 страницImpact of Ifrs Power and UtilitiesBlazen MinicОценок пока нет

- Biaya PembangkitanДокумент28 страницBiaya PembangkitanblackzenyОценок пока нет

- Solar Power GenerationДокумент21 страницаSolar Power GenerationRiddhi PaulОценок пока нет

- Gravimetric Feeders - InstrumentationДокумент15 страницGravimetric Feeders - InstrumentationAakanksha GahlautОценок пока нет

- MRO On The Move: Outsourcing Maintenance, Repair and OperationsДокумент12 страницMRO On The Move: Outsourcing Maintenance, Repair and Operationssha_yadОценок пока нет

- LectureFive HybridSystemДокумент25 страницLectureFive HybridSystemmuluken eliasОценок пока нет

- Top 30 Large-Scale Solar Portfolios in VietnamДокумент14 страницTop 30 Large-Scale Solar Portfolios in VietnamChoky SimanjuntakОценок пока нет

- Session 6 - Case Study On Haripur 360 MW Combined Cycle Power Plant by Nazrul IslamДокумент27 страницSession 6 - Case Study On Haripur 360 MW Combined Cycle Power Plant by Nazrul IslamFarukHossainОценок пока нет

- Fuel ManagementДокумент27 страницFuel Managementpprasad_g9358100% (1)

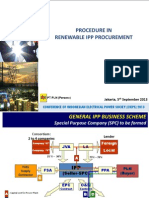

- IPP Procedure ConferenceДокумент10 страницIPP Procedure ConferencekongbengОценок пока нет

- Combined Cycle Power PlantsДокумент11 страницCombined Cycle Power Plantswellington freitasОценок пока нет

- A Higher Chromium Weld Overlay Alloy For Water Wall & SHeaterДокумент7 страницA Higher Chromium Weld Overlay Alloy For Water Wall & SHeaterHalim SelamatОценок пока нет

- Combined Cycle Gas Turbine Gyanendra Sharma NPTI DelhiДокумент148 страницCombined Cycle Gas Turbine Gyanendra Sharma NPTI DelhiNPTIОценок пока нет

- Maintain turbine plant feed systemsДокумент21 страницаMaintain turbine plant feed systemsVIBHAV100% (1)

- Improving Thermal Power Plant PerformanceДокумент7 страницImproving Thermal Power Plant PerformanceJaydeep kunduОценок пока нет

- History of Desalination Cost EstimationsДокумент17 страницHistory of Desalination Cost EstimationsGiovanniStirelliОценок пока нет

- Energy Efficiency Through Better OM PracticesДокумент21 страницаEnergy Efficiency Through Better OM PracticessrinivasgillalaОценок пока нет

- 11i Asset Management Fundamentals Supplemental Practices StuДокумент106 страниц11i Asset Management Fundamentals Supplemental Practices StureddypallyОценок пока нет

- EPRI2009HeatRateConference FINALДокумент14 страницEPRI2009HeatRateConference FINALcynaiduОценок пока нет

- Legal Bases for Mining Rights and PermitsДокумент16 страницLegal Bases for Mining Rights and PermitsNeil Rivera100% (1)

- REVIEW: Literature on Combustor Design ModelsДокумент4 страницыREVIEW: Literature on Combustor Design ModelsNesdale BuenaflorОценок пока нет

- Project ReportДокумент101 страницаProject Reportसुभाष सिँहОценок пока нет

- Enms at TPDDLДокумент18 страницEnms at TPDDLapoorva sethОценок пока нет

- Enhancing The Corporate Energy Performance: Energy Efficiency and Renewable Energy, GridДокумент8 страницEnhancing The Corporate Energy Performance: Energy Efficiency and Renewable Energy, GridSnehasis HotaОценок пока нет

- TSPL GST Petition - AnnexuresДокумент407 страницTSPL GST Petition - AnnexuresVIVEK anandОценок пока нет

- Case Study On Power PlantДокумент9 страницCase Study On Power PlantMusaОценок пока нет

- Dessert Dilemma - A Capital Case StudyДокумент9 страницDessert Dilemma - A Capital Case StudyBurhan Bakkal0% (1)

- News Brazil Biomass Export Wood ChipsДокумент18 страницNews Brazil Biomass Export Wood Chipsmar4478100% (2)

- Case Analysis-Sasan Power LTDДокумент19 страницCase Analysis-Sasan Power LTDpranjaligОценок пока нет

- Analysis of PepsiCo's Acquisition of Quaker OaksДокумент2 страницыAnalysis of PepsiCo's Acquisition of Quaker Oaksaza_ma100% (2)

- Exactspace: Power Plant AnalyticsДокумент24 страницыExactspace: Power Plant AnalyticsK Senthil Ram KumarОценок пока нет

- Optimized VCB drawing titleДокумент23 страницыOptimized VCB drawing titleDevas ShuklaОценок пока нет

- Waterfall chart showing company revenues by categoryДокумент10 страницWaterfall chart showing company revenues by categoryEvert TrochОценок пока нет

- Global Wood Pellet Fuel Market Research Report 2017Документ2 страницыGlobal Wood Pellet Fuel Market Research Report 2017Eric Bendic0% (1)

- Final Mid-Term Report 141208Документ248 страницFinal Mid-Term Report 141208Cuttie CatzОценок пока нет

- Fabby Tumiwa - Indonesia FiT Implementation and Improvement ChallengesДокумент13 страницFabby Tumiwa - Indonesia FiT Implementation and Improvement ChallengesAsia Clean Energy ForumОценок пока нет

- Sustainable Finance: The Imperative and The OpportunityДокумент70 страницSustainable Finance: The Imperative and The OpportunityNidia Liliana TovarОценок пока нет

- Performance Monitoring - A Study On ISO 14001 Certified Power PlantДокумент10 страницPerformance Monitoring - A Study On ISO 14001 Certified Power Plantredbeanz138Оценок пока нет

- Policy For CaptiveДокумент17 страницPolicy For CaptiveRamesh AnanthanarayananОценок пока нет

- Power Plant 635 6.KSTPS 0Документ21 страницаPower Plant 635 6.KSTPS 0Mayank SharmaОценок пока нет

- Functioning of Power ExchangesДокумент36 страницFunctioning of Power ExchangesMuqthiar AliОценок пока нет

- PAT MV Guidelines by Mr. S. Vikash Ranjan Technical Expert GIZДокумент45 страницPAT MV Guidelines by Mr. S. Vikash Ranjan Technical Expert GIZVenkata Krishna PОценок пока нет

- RelianceДокумент28 страницRelianceMrudu PadteОценок пока нет

- Clean Energy Investment Trends 2020 - Full ReportДокумент44 страницыClean Energy Investment Trends 2020 - Full ReportevelynОценок пока нет

- Research ServicesДокумент25 страницResearch Servicesmittaldivya167889Оценок пока нет

- Cross-Channel Customer Experience Is Key To Success For Retail IndustryДокумент59 страницCross-Channel Customer Experience Is Key To Success For Retail Industrymittaldivya167889Оценок пока нет

- Crafting Integrated Multi-Channel Retailing StrategyДокумент41 страницаCrafting Integrated Multi-Channel Retailing StrategyNatalie Shimin LiОценок пока нет

- Transition To IFRS 1Документ42 страницыTransition To IFRS 1cajitendergupta100% (2)

- International Financial Reporting Standards (: Ifrs)Документ12 страницInternational Financial Reporting Standards (: Ifrs)samimustОценок пока нет

- BopsДокумент24 страницыBopsmittaldivya167889Оценок пока нет

- US Gaap Vs IFRSДокумент76 страницUS Gaap Vs IFRSmittaldivya167889100% (1)

- 5thslidescapital MarketДокумент37 страниц5thslidescapital Marketmittaldivya167889Оценок пока нет

- UnderwriterДокумент9 страницUnderwritermittaldivya167889Оценок пока нет

- Sbi and HDFC Comparative Study of Customer S Satisfaction TowardsДокумент67 страницSbi and HDFC Comparative Study of Customer S Satisfaction TowardsMõørthï Shãrmâ75% (4)

- Concorde Airlines RoutesДокумент10 страницConcorde Airlines RoutesFauziah FarhahОценок пока нет

- Mylan Matrix MergerДокумент14 страницMylan Matrix MergerShobhit Saxena0% (1)

- INFOДокумент1 страницаINFOJeff MaysОценок пока нет

- Merger & AcquisitionДокумент16 страницMerger & Acquisitionvarsha_kuchara01Оценок пока нет

- Aeropostale AnalysisДокумент6 страницAeropostale AnalysisHani WaniОценок пока нет

- Ch13-Cash Flow STMДокумент44 страницыCh13-Cash Flow STMAnonymous zXWxWmgZEОценок пока нет

- Organograms - All Directorates IOM 17.8.2018Документ7 страницOrganograms - All Directorates IOM 17.8.2018Sanjai bhadouriaОценок пока нет

- MUDRA – Empowering Micro, Small & Medium EnterprisesДокумент20 страницMUDRA – Empowering Micro, Small & Medium EnterprisesAbhishek RastogiОценок пока нет

- causelistALL2022 08 25 2Документ160 страницcauselistALL2022 08 25 2Akash TandonОценок пока нет

- WealthДокумент2 страницыWealthRaghav IssarОценок пока нет

- Corpo CaseДокумент3 страницыCorpo Caseeunice demaclidОценок пока нет

- Fall of Anil AmbaniДокумент4 страницыFall of Anil AmbaniIshwar SinghОценок пока нет

- C Law T2Документ5 страницC Law T2hudaОценок пока нет

- Panoramic - Full Info of Group Cos.Документ14 страницPanoramic - Full Info of Group Cos.JnanamОценок пока нет

- Case StudyДокумент2 страницыCase StudyMD75% (8)

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceДокумент1 страницаStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancemrcopy xeroxОценок пока нет

- LOBOFinal Exam 2. 2008Документ4 страницыLOBOFinal Exam 2. 2008Jason ZenereОценок пока нет

- Case On SitaraДокумент13 страницCase On SitaraOmer Khalid KhanОценок пока нет

- June 2017Документ60 страницJune 2017PROMonthlyОценок пока нет

- The Determinants of Venture Capital: Research PaperДокумент12 страницThe Determinants of Venture Capital: Research PaperSehar SajjadОценок пока нет

- Building SC for Advantage at M&MДокумент1 страницаBuilding SC for Advantage at M&MChaitanya R KodavatyОценок пока нет

- Emirates - Manage A Booking - View TicketДокумент2 страницыEmirates - Manage A Booking - View Ticketshuvro911100% (2)