Вам также может понравиться

- CRNT IR Presentation August 2019 FinalДокумент25 страницCRNT IR Presentation August 2019 FinalCesar QОценок пока нет

- Haziq Project Finance1Документ17 страницHaziq Project Finance1Ali RazaОценок пока нет

- OracleДокумент12 страницOracleandre.torresОценок пока нет

- CTRA Results Presentation 12M17Документ36 страницCTRA Results Presentation 12M17WINARTO CHANDRAОценок пока нет

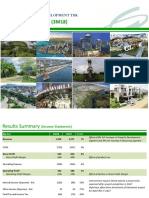

- CTRA Results Presentation 3M18Документ36 страницCTRA Results Presentation 3M18anthony cs100% (1)

- Cisco Q2FY11 Earnings SlidesДокумент14 страницCisco Q2FY11 Earnings SlidesCisco Investor RelationsОценок пока нет

- France Telecom: Morgan Stanley TMT ConferenceДокумент13 страницFrance Telecom: Morgan Stanley TMT Conferenceshahid10Оценок пока нет

- T-Mobile US Q4 and Full Year 2013Документ18 страницT-Mobile US Q4 and Full Year 2013Spit FireОценок пока нет

- Idea Cellular Limited: Investor PresentationДокумент20 страницIdea Cellular Limited: Investor PresentationjoydeoraОценок пока нет

- Usha Martiri: Bourse deДокумент17 страницUsha Martiri: Bourse deKumar V. S.Оценок пока нет

- Nov 2019 PresentationДокумент39 страницNov 2019 PresentationCatarinaNhuОценок пока нет

- Nokia Financial Report 2023 Q2Документ20 страницNokia Financial Report 2023 Q2Ahmed HussainОценок пока нет

- Oracle eДокумент10 страницOracle eAndre TorresОценок пока нет

- PTCL Financial ReportДокумент26 страницPTCL Financial Reportfazal hadiОценок пока нет

- UK Short Mobile 2008Документ22 страницыUK Short Mobile 2008solo12344322Оценок пока нет

- Reliance Communications: Group 8 Presented By: Nichelle Kamath Mitali Mistry Komal Tambade - F65 Mansi Morajkar - F39Документ31 страницаReliance Communications: Group 8 Presented By: Nichelle Kamath Mitali Mistry Komal Tambade - F65 Mansi Morajkar - F39sachinborade11997Оценок пока нет

- UMTS Multi-Sector Deployment StrategyДокумент31 страницаUMTS Multi-Sector Deployment StrategySangwani Nyirenda100% (1)

- Idea Cellular Limited: Investor PresentationДокумент20 страницIdea Cellular Limited: Investor Presentationankush23Оценок пока нет

- Business CaseДокумент11 страницBusiness CasesomeshОценок пока нет

- Merak Fiscal Model Library: Colombia Association (2002)Документ2 страницыMerak Fiscal Model Library: Colombia Association (2002)Libya TripoliОценок пока нет

- Q3 2021 Financial Highlights: October 27, 2021Документ23 страницыQ3 2021 Financial Highlights: October 27, 2021gvrabbitОценок пока нет

- Embassy Office Parks REIT: 1Q FY2022 Earnings MaterialsДокумент51 страницаEmbassy Office Parks REIT: 1Q FY2022 Earnings Materialsmohit niranjaneОценок пока нет

- Juniper Networks: Investor RelationsДокумент33 страницыJuniper Networks: Investor RelationsTuPro FessionalОценок пока нет

- Advanc Investor Presentation PDFДокумент24 страницыAdvanc Investor Presentation PDFtat angОценок пока нет

- MediaRing AR04Документ68 страницMediaRing AR04Karan Henrik PonnuduraiОценок пока нет

- July 24, 2023: Execution With Pace & ComfortДокумент25 страницJuly 24, 2023: Execution With Pace & ComfortNostalgic MediatorОценок пока нет

- Shanghai Ifc Chiller Plant OptimizationДокумент45 страницShanghai Ifc Chiller Plant OptimizationYen NguyenОценок пока нет

- Final Work - Corporate Finances For UtilitiesДокумент15 страницFinal Work - Corporate Finances For UtilitiesThor Batista AvengersОценок пока нет

- 3Q09 Business Conference)Документ19 страниц3Q09 Business Conference)sdey003Оценок пока нет

- WABCO 2018 Corporate Overview FINAL - Web VersionДокумент25 страницWABCO 2018 Corporate Overview FINAL - Web VersionMilton EncaladaОценок пока нет

- CVA Range: Linear and Quarter-TurnДокумент32 страницыCVA Range: Linear and Quarter-Turnmani_208eeОценок пока нет

- Siemens Business Fact SheetsДокумент9 страницSiemens Business Fact Sheetszain shafiqОценок пока нет

- Grameenphone: Ceo - Erik AasДокумент18 страницGrameenphone: Ceo - Erik AasMohammad AdnanОценок пока нет

- Shaikha Al-Jabir - Strategic InnovationДокумент12 страницShaikha Al-Jabir - Strategic InnovationictQATARОценок пока нет

- Charla12AGO2022 TelcoTRENDS Mckinsey 2023-2026CEДокумент29 страницCharla12AGO2022 TelcoTRENDS Mckinsey 2023-2026CEalejandro claroОценок пока нет

- Full Report 1Документ10 страницFull Report 1Kajune ChithilaphaОценок пока нет

- 593 05 24-16-Cisco Voice Over Wi-Fi CKN May 2016 FinalV1 PDFДокумент29 страниц593 05 24-16-Cisco Voice Over Wi-Fi CKN May 2016 FinalV1 PDFAkash SainiОценок пока нет

- Monthly PnLTrackerДокумент6 страницMonthly PnLTrackerjohnОценок пока нет

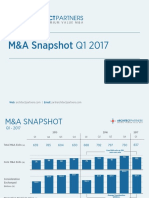

- AP M&A Q1 2017 SnapshotДокумент18 страницAP M&A Q1 2017 SnapshotArchitectPartnersОценок пока нет

- Turkcell Summary Data Document Q123 ENG VfinalДокумент2 страницыTurkcell Summary Data Document Q123 ENG Vfinalmahmoud.te.strategyОценок пока нет

- Wipro Annual Report 2004 2005Документ308 страницWipro Annual Report 2004 2005raghu myОценок пока нет

- Eitc - P - 2022 Q3Документ24 страницыEitc - P - 2022 Q3Abdisalam UnshurОценок пока нет

- Power Plant Costing-Iii-IndusДокумент9 страницPower Plant Costing-Iii-IndusgmsangeethОценок пока нет

- The Fortinet Security Fabric: Broad Integrated AutomatedДокумент12 страницThe Fortinet Security Fabric: Broad Integrated AutomatedMUMОценок пока нет

- Nokia Financial Report 2023 Q1Документ21 страницаNokia Financial Report 2023 Q1Ahmed HussainОценок пока нет

- 4q23 Pressrelease June FinalДокумент13 страниц4q23 Pressrelease June Finaljalajsingh1987Оценок пока нет

- Telkomsel 5G - IndoTelko - Final Present PDFДокумент19 страницTelkomsel 5G - IndoTelko - Final Present PDFBudi Susanto Abdul QudusОценок пока нет

- PirelliДокумент18 страницPirellisantiago foriguaОценок пока нет

- Oracle Announces Fiscal 2022 Second Quarter Financial ResultsДокумент12 страницOracle Announces Fiscal 2022 Second Quarter Financial ResultsAndrea MinelliОценок пока нет

- CTRA Results Presentation 6M20Документ48 страницCTRA Results Presentation 6M20Ami HamidahОценок пока нет

- Weir Capital Markets Day 17 June 2014Документ83 страницыWeir Capital Markets Day 17 June 2014iman_pumpОценок пока нет

- Scatec Third Quarter Presentation 2022 1Документ20 страницScatec Third Quarter Presentation 2022 1adsafasОценок пока нет

- 7750 SR VP Ls White PaperДокумент23 страницы7750 SR VP Ls White PapermarioОценок пока нет

- 03d. Schubert, Usa (Ing)Документ15 страниц03d. Schubert, Usa (Ing)Jose AltamiranoОценок пока нет

- Monthly PnLTrackerДокумент6 страницMonthly PnLTrackersyamsudin mohОценок пока нет

- Atc&c (Dikko)Документ10 страницAtc&c (Dikko)Chidiebere Samuel OkogwuОценок пока нет

- Distributed Process Control ReportОт EverandDistributed Process Control ReportОценок пока нет

- Crisil SmeДокумент60 страницCrisil SmeUtkarsh PandeyОценок пока нет

- Chapter 23 CPWD ACCOUNTS CODEДокумент17 страницChapter 23 CPWD ACCOUNTS CODEarulraj1971Оценок пока нет

- Detecting Breakouts From Flags & PennantsДокумент9 страницDetecting Breakouts From Flags & PennantsdrkwngОценок пока нет

- Working Capital MangementДокумент92 страницыWorking Capital MangementSunil ThakurОценок пока нет

- Addressing Working Capital Policies and Management of ShortДокумент17 страницAddressing Working Capital Policies and Management of ShortAnne MoralesОценок пока нет

- The CFA Conundrum - Does CFA With MBA in Finance Add Value - Inside IIMДокумент9 страницThe CFA Conundrum - Does CFA With MBA in Finance Add Value - Inside IIMashokyerasiОценок пока нет

- 2015 Two BrothersДокумент43 страницы2015 Two BrothersAnonymous Wu0bxv6p7Оценок пока нет

- Accomplishment AssignmentДокумент6 страницAccomplishment AssignmentAditJoshiОценок пока нет

- MCQ FinalДокумент6 страницMCQ FinalihtishamОценок пока нет

- Types of Financial Decisions: Investment Decision, Financing Decision, Dividend Decision and Working Capital Management DecisionДокумент4 страницыTypes of Financial Decisions: Investment Decision, Financing Decision, Dividend Decision and Working Capital Management DecisionCjhay MarcosОценок пока нет

- Indochina Capital Vietnam Holdings LimitedДокумент46 страницIndochina Capital Vietnam Holdings LimitednghoangmaiОценок пока нет

- Café Coffee Day - VRIO AnalysisДокумент2 страницыCafé Coffee Day - VRIO AnalysisShilpa Isabella D'souza100% (1)

- Secondary MarketДокумент32 страницыSecondary MarketMrunal Chetan JosihОценок пока нет

- US Internal Revenue Service: F1040sab - 1992Документ2 страницыUS Internal Revenue Service: F1040sab - 1992IRSОценок пока нет

- Week 3 Tutorials - PDF PDFДокумент9 страницWeek 3 Tutorials - PDF PDFDaniel NgoОценок пока нет

- Achievements CimbДокумент6 страницAchievements CimbShirlie ChongОценок пока нет

- Financial Management TheoryДокумент7 страницFinancial Management TheoryAnandhi SomasundaramОценок пока нет

- IAPMДокумент2 страницыIAPMKeshav RanaОценок пока нет

- Swift Training CatalogДокумент55 страницSwift Training Catalogscribdirrfan100% (1)

- Business Proposal - Solar Street LightДокумент4 страницыBusiness Proposal - Solar Street LightAhmad Rum33% (3)

- EME500 ProblemSet1 F18 Revised-1 (Traore, Abdelmoumine)Документ5 страницEME500 ProblemSet1 F18 Revised-1 (Traore, Abdelmoumine)Abdel Lee Moomine TraoréОценок пока нет

- Shashi FinalДокумент86 страницShashi FinalVidyaОценок пока нет

- Tunisia - Country Profile: 1 Background 2 2 Population 2Документ18 страницTunisia - Country Profile: 1 Background 2 2 Population 2stand4xОценок пока нет

- Ratio Analysis M&M and Maruti SuzukiДокумент36 страницRatio Analysis M&M and Maruti SuzukiSamiSherzai50% (2)

- Centurion Bank of PunjabДокумент7 страницCenturion Bank of Punjabbaggamraasi1234Оценок пока нет

- Wild Ib8 PPT 04Документ22 страницыWild Ib8 PPT 04TINОценок пока нет

- CAPA - Ground Handling ReportДокумент25 страницCAPA - Ground Handling ReportTed0% (1)

- A Comprehensive Study On Benefits of Mutual Fund Schemes To The Individual InvestorsДокумент23 страницыA Comprehensive Study On Benefits of Mutual Fund Schemes To The Individual InvestorsswetaleenaОценок пока нет

- The Great Divide Over Market EfficicnecyДокумент10 страницThe Great Divide Over Market EfficicnecynamgapОценок пока нет

- 2019-04-01 North & South PDFДокумент124 страницы2019-04-01 North & South PDFMichel HaddadОценок пока нет