Вам также может понравиться

- Exam Prep for:: Business Analysis and Valuation Using Financial Statements, Text and CasesОт EverandExam Prep for:: Business Analysis and Valuation Using Financial Statements, Text and CasesОценок пока нет

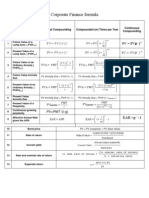

- Corporate Finance Formulas: A Simple IntroductionОт EverandCorporate Finance Formulas: A Simple IntroductionРейтинг: 4 из 5 звезд4/5 (8)

- Finance Cheat SheetДокумент4 страницыFinance Cheat SheetRudolf Jansen van RensburgОценок пока нет

- CheatSheet (Finance)Документ1 страницаCheatSheet (Finance)Guan Yu Lim100% (3)

- Kelly's Finance Cheat Sheet V6Документ2 страницыKelly's Finance Cheat Sheet V6Kelly Koh100% (4)

- Corporate Finance Formula SheetДокумент4 страницыCorporate Finance Formula Sheetogsunny100% (3)

- CorpFinance Cheat Sheet v2.2Документ2 страницыCorpFinance Cheat Sheet v2.2subtle69100% (4)

- BF2201 Cheat Sheet FinalsДокумент2 страницыBF2201 Cheat Sheet Finalssiewhong93100% (1)

- Overview of Financial Management Concepts and ToolsДокумент4 страницыOverview of Financial Management Concepts and ToolsPeixuan Zhuang100% (1)

- Cheat Sheet Corporate - FinanceДокумент2 страницыCheat Sheet Corporate - FinanceAnna BudaevaОценок пока нет

- Fnce 100 Final Cheat SheetДокумент2 страницыFnce 100 Final Cheat SheetToby Arriaga100% (2)

- Corporate Finance Math SheetДокумент19 страницCorporate Finance Math Sheetmweaveruga100% (3)

- Cheat Sheet Final - FMVДокумент3 страницыCheat Sheet Final - FMVhanifakih100% (2)

- Cheat Sheet - AccountingДокумент2 страницыCheat Sheet - AccountingJeffery KaoОценок пока нет

- Equation Formula: 1 1 FV PMT 1Документ3 страницыEquation Formula: 1 1 FV PMT 1JMSB09Оценок пока нет

- Cheat Sheet - EXAM Version - BARBARAДокумент2 страницыCheat Sheet - EXAM Version - BARBARAJosé António Cardoso RodriguesОценок пока нет

- FMV Cheat SheetДокумент1 страницаFMV Cheat SheetAyushi SharmaОценок пока нет

- Midsem Cheat Sheet (Finance)Документ2 страницыMidsem Cheat Sheet (Finance)lalaran123Оценок пока нет

- Corporate FinanceДокумент19 страницCorporate FinanceBilal Shahid100% (4)

- Formula Sheet Corporate Finance (COF) : Stockholm Business SchoolДокумент6 страницFormula Sheet Corporate Finance (COF) : Stockholm Business SchoolLinus AhlgrenОценок пока нет

- Fin Cheat SheetДокумент3 страницыFin Cheat SheetChristina RomanoОценок пока нет

- Session 2 - Doing VC Deals - Lecture Presentation Slides IM 5 Mar 12Документ58 страницSession 2 - Doing VC Deals - Lecture Presentation Slides IM 5 Mar 12Henry So E Diarko100% (1)

- CheatДокумент1 страницаCheatIshmo KueedОценок пока нет

- Finance ProblemSets11Документ323 страницыFinance ProblemSets11Stefan CN100% (2)

- The Ultimate Financial Management Cheat SheetДокумент3 страницыThe Ultimate Financial Management Cheat SheethazimОценок пока нет

- Accounting Cheat SheetДокумент2 страницыAccounting Cheat Sheetanoushes1100% (2)

- Balance of Payments:: Chapter Objectives & Lecture Notes FINA 5500Документ27 страницBalance of Payments:: Chapter Objectives & Lecture Notes FINA 5500Anonymous H0SJWZE8100% (1)

- Summary - Corporate Finance Beck DeMarzoДокумент54 страницыSummary - Corporate Finance Beck DeMarzoAlejandra100% (2)

- DCF Intrinsic ValuationДокумент38 страницDCF Intrinsic ValuationKritika KoulОценок пока нет

- FIN6215-Cheat Sheet BigДокумент3 страницыFIN6215-Cheat Sheet BigJojo Kittiya100% (1)

- Cfa Level I - Us Gaap Vs IfrsДокумент4 страницыCfa Level I - Us Gaap Vs IfrsSanjay RathiОценок пока нет

- Cheat Sheet For Financial AccountingДокумент1 страницаCheat Sheet For Financial Accountingmikewu101Оценок пока нет

- Accounting Cheat Sheet FinalsДокумент5 страницAccounting Cheat Sheet FinalsRahel CharikarОценок пока нет

- Corporate Finance Cheat SheetДокумент3 страницыCorporate Finance Cheat Sheetdiscreetmike50Оценок пока нет

- 3 - FCF CalculationДокумент2 страницы3 - FCF CalculationAman ManjiОценок пока нет

- Practice MidtermДокумент8 страницPractice MidtermghaniaОценок пока нет

- Cohen Finance Workbook FALL 2013Документ124 страницыCohen Finance Workbook FALL 2013Nayef AbdullahОценок пока нет

- Intl Finance Cheat SheetДокумент6 страницIntl Finance Cheat Sheetpradhan.neeladriОценок пока нет

- Corporate Finance FormulasДокумент3 страницыCorporate Finance FormulasMustafa Yavuzcan83% (12)

- Corporate FinanceДокумент24 страницыCorporate Financeapi-3719687100% (3)

- Financial Modeling and Analysis 3Ed-LibreДокумент14 страницFinancial Modeling and Analysis 3Ed-LibremjcstimsonОценок пока нет

- Managerial Accounting Mid-Term Cheat SheetДокумент6 страницManagerial Accounting Mid-Term Cheat SheetĐạt Nguyễn100% (1)

- Atlassian 3 Statement Model CompleteДокумент24 страницыAtlassian 3 Statement Model CompleteShrey JainОценок пока нет

- Corporate Finance Cheatsheet Zhiwei NewДокумент2 страницыCorporate Finance Cheatsheet Zhiwei NewZaggie NgОценок пока нет

- Technical Finance Interview Prep (Student)Документ261 страницаTechnical Finance Interview Prep (Student)fernando.torrealbatesiОценок пока нет

- Handout # 1 Solutions (L)Документ10 страницHandout # 1 Solutions (L)Prabhawati prasadОценок пока нет

- Finance Cheat SheetДокумент2 страницыFinance Cheat SheetMarc MОценок пока нет

- Dividend Discount and Residual Income Models ExplainedДокумент2 страницыDividend Discount and Residual Income Models ExplainedMohammad DaulehОценок пока нет

- Cheat SheetДокумент2 страницыCheat SheetDimana Dollo100% (1)

- Capital Structure and Cost of CapitalДокумент3 страницыCapital Structure and Cost of CapitalAbhijit PanditОценок пока нет

- FIN 401 - Cheat SheetДокумент2 страницыFIN 401 - Cheat SheetStephanie NaamaniОценок пока нет

- Corporate Finance Formula SheetДокумент9 страницCorporate Finance Formula SheetWilliamОценок пока нет

- Formulas - All Chapters - Corporate Finance Formulas - All Chapters - Corporate FinanceДокумент6 страницFormulas - All Chapters - Corporate Finance Formulas - All Chapters - Corporate FinanceNaeemОценок пока нет

- Financial Management - Formula SheetДокумент8 страницFinancial Management - Formula SheetHassleBustОценок пока нет

- R) (1 CF ...... R) (1 CF R) (1 CF CF NPV: Invesment Initial NPV 1 Invesments Initial Flows Cash Future of PVДокумент9 страницR) (1 CF ...... R) (1 CF R) (1 CF CF NPV: Invesment Initial NPV 1 Invesments Initial Flows Cash Future of PVAgnes LoОценок пока нет

- CFA Formula Cheat SheetДокумент9 страницCFA Formula Cheat SheetChingWa ChanОценок пока нет

- Cost of CapitalДокумент31 страницаCost of CapitalMadhuram Sharma100% (1)

- Accounting and Finance Formulas: A Simple IntroductionОт EverandAccounting and Finance Formulas: A Simple IntroductionРейтинг: 4 из 5 звезд4/5 (8)

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)От EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Рейтинг: 3.5 из 5 звезд3.5/5 (17)

- Geneva IntrotoBankDebt172Документ66 страницGeneva IntrotoBankDebt172satishlad1288Оценок пока нет

- Victor's Letter Identity V Wiki FandomДокумент1 страницаVictor's Letter Identity V Wiki FandomvickyОценок пока нет

- Course Syllabus: Aurora Pioneers Memorial CollegeДокумент9 страницCourse Syllabus: Aurora Pioneers Memorial CollegeLorisa CenizaОценок пока нет

- Lec - Ray Theory TransmissionДокумент27 страницLec - Ray Theory TransmissionmathewОценок пока нет

- Civil Aeronautics BoardДокумент2 страницыCivil Aeronautics BoardJayson AlvaОценок пока нет

- Tyron Butson (Order #37627400)Документ74 страницыTyron Butson (Order #37627400)tyron100% (2)

- Mayor Byron Brown's 2019 State of The City SpeechДокумент19 страницMayor Byron Brown's 2019 State of The City SpeechMichael McAndrewОценок пока нет

- CORE Education Bags Rs. 120 Cr. Order From Gujarat Govt.Документ2 страницыCORE Education Bags Rs. 120 Cr. Order From Gujarat Govt.Sanjeev MansotraОценок пока нет

- Asian Construction Dispute Denied ReviewДокумент2 страницыAsian Construction Dispute Denied ReviewJay jogs100% (2)

- Wind EnergyДокумент6 страницWind Energyshadan ameenОценок пока нет

- Benchmarking Guide OracleДокумент53 страницыBenchmarking Guide OracleTsion YehualaОценок пока нет

- Case Study 2 F3005Документ12 страницCase Study 2 F3005Iqmal DaniealОценок пока нет

- ZOOLOGY INTRODUCTIONДокумент37 страницZOOLOGY INTRODUCTIONIneshОценок пока нет

- Introduction To Succession-1Документ8 страницIntroduction To Succession-1amun dinОценок пока нет

- Chill - Lease NotesДокумент19 страницChill - Lease Notesbellinabarrow100% (4)

- Safety QualificationДокумент2 страницыSafety QualificationB&R HSE BALCO SEP SiteОценок пока нет

- ITSCM Mindmap v4Документ1 страницаITSCM Mindmap v4Paul James BirchallОценок пока нет

- ADSLADSLADSLДокумент83 страницыADSLADSLADSLKrishnan Unni GОценок пока нет

- NEW CREW Fast Start PlannerДокумент9 страницNEW CREW Fast Start PlannerAnonymous oTtlhP100% (3)

- Improvements To Increase The Efficiency of The Alphazero Algorithm: A Case Study in The Game 'Connect 4'Документ9 страницImprovements To Increase The Efficiency of The Alphazero Algorithm: A Case Study in The Game 'Connect 4'Lam Mai NgocОценок пока нет

- High Altitude Compensator Manual 10-2011Документ4 страницыHigh Altitude Compensator Manual 10-2011Adem NuriyeОценок пока нет

- Department Order No 05-92Документ3 страницыDepartment Order No 05-92NinaОценок пока нет

- DSA NotesДокумент87 страницDSA NotesAtefrachew SeyfuОценок пока нет

- Advance Bio-Photon Analyzer ABPA A2 Home PageДокумент5 страницAdvance Bio-Photon Analyzer ABPA A2 Home PageStellaEstel100% (1)

- Micromaster 430: 7.5 KW - 250 KWДокумент118 страницMicromaster 430: 7.5 KW - 250 KWAyman ElotaifyОценок пока нет

- 50TS Operators Manual 1551000 Rev CДокумент184 страницы50TS Operators Manual 1551000 Rev CraymondОценок пока нет

- 1LE1503-2AA43-4AA4 Datasheet enДокумент1 страница1LE1503-2AA43-4AA4 Datasheet enAndrei LupuОценок пока нет

- International Convention Center, BanesworДокумент18 страницInternational Convention Center, BanesworSreeniketh ChikuОценок пока нет

- GS Ep Cor 356Документ7 страницGS Ep Cor 356SangaranОценок пока нет

- Resume Ajeet KumarДокумент2 страницыResume Ajeet KumarEr Suraj KumarОценок пока нет