Вам также может понравиться

- Rightward Drift in NepalДокумент4 страницыRightward Drift in NepalShay WaxenОценок пока нет

- Maoist Defeat in NepalДокумент4 страницыMaoist Defeat in NepalShay WaxenОценок пока нет

- PS XLIX 4 250114 Postscript Nabina DasДокумент2 страницыPS XLIX 4 250114 Postscript Nabina DasShay WaxenОценок пока нет

- PS XLIX 4 250114 Postscript C K MeenaДокумент2 страницыPS XLIX 4 250114 Postscript C K MeenaShay WaxenОценок пока нет

- Historical Validity of Mullaperiyar ProjectДокумент5 страницHistorical Validity of Mullaperiyar ProjectShay WaxenОценок пока нет

- ED XLIX 4 250114 A Hare-Brained ProposalДокумент2 страницыED XLIX 4 250114 A Hare-Brained ProposalShay WaxenОценок пока нет

- From 50 Years AgoДокумент1 страницаFrom 50 Years AgoShay WaxenОценок пока нет

- Can AAP Slay The DragonДокумент2 страницыCan AAP Slay The DragonShay WaxenОценок пока нет

- Status Quo MaintainedДокумент1 страницаStatus Quo MaintainedShay WaxenОценок пока нет

- Statistically MotivatedДокумент3 страницыStatistically MotivatedShay WaxenОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- SSI FAQs Updated 2021Документ2 страницыSSI FAQs Updated 2021Indiana Family to FamilyОценок пока нет

- VA - Sankalp Parihar - 142Документ13 страницVA - Sankalp Parihar - 142Sankalp PariharОценок пока нет

- International Taxation OutlineДокумент138 страницInternational Taxation OutlineMa FajardoОценок пока нет

- Your GIRO Payment Plan For Income Tax: DBS/POSB xxxxxx9205Документ2 страницыYour GIRO Payment Plan For Income Tax: DBS/POSB xxxxxx9205Karaoui LaidОценок пока нет

- Public Debt FlowchartДокумент1 страницаPublic Debt FlowchartRbОценок пока нет

- Tax Sem OuputДокумент43 страницыTax Sem OuputAshlley Nicole VillaranОценок пока нет

- Mark Horton and Asmaa El-Ganainy - 2017 - Fiscal Policy Taking and Giving Away' - Finance and DevelopmentДокумент5 страницMark Horton and Asmaa El-Ganainy - 2017 - Fiscal Policy Taking and Giving Away' - Finance and Developmentrolandgraham29Оценок пока нет

- Semi Quiz 1Документ2 страницыSemi Quiz 1jp careОценок пока нет

- Sample Copy - Mphasis &finsource PDFДокумент2 страницыSample Copy - Mphasis &finsource PDFSameer ShaikhОценок пока нет

- Jurnal Transfer PricingДокумент11 страницJurnal Transfer PricingMitha Kartika NabilahОценок пока нет

- Republic V Dela RamaДокумент2 страницыRepublic V Dela RamaKarenliambrycejego Ragragio100% (2)

- FRBM ActДокумент2 страницыFRBM ActSpideycodОценок пока нет

- No Plastic Packaging: Tax InvoiceДокумент15 страницNo Plastic Packaging: Tax Invoicehiteshmohakar15Оценок пока нет

- Income Taxation Quiz 1Документ2 страницыIncome Taxation Quiz 1Yi Zara100% (1)

- CA Inter Taxation Question BankДокумент425 страницCA Inter Taxation Question BankvisshelpОценок пока нет

- Lecture 1 - Introduction To Statutory ValuationДокумент11 страницLecture 1 - Introduction To Statutory ValuationQayyumОценок пока нет

- GSTR3B 03alnpk4728k1zv 042021Документ2 страницыGSTR3B 03alnpk4728k1zv 042021Harish VermaОценок пока нет

- شهادة التسجيل الضريبىДокумент1 страницаشهادة التسجيل الضريبىAL MASSA CONTRACTINGОценок пока нет

- Public SectorДокумент2 страницыPublic SectorDarlyn CarelОценок пока нет

- Republican Jewish Coalition Form 990 For 2012Документ65 страницRepublican Jewish Coalition Form 990 For 2012mjbeckelОценок пока нет

- p5101 - 2019-10-00 1Документ53 страницыp5101 - 2019-10-00 1api-495108136Оценок пока нет

- RA 11534 CREATE As Signed Into Law Briefing For FINEXДокумент18 страницRA 11534 CREATE As Signed Into Law Briefing For FINEXKevin BonaobraОценок пока нет

- Segment Results PDFДокумент1 страницаSegment Results PDFhkm_gmat4849Оценок пока нет

- Gutierrez v. CIR - SubaДокумент1 страницаGutierrez v. CIR - SubaPaul Joshua SubaОценок пока нет

- Lecture Notes Allowable DeductionsДокумент51 страницаLecture Notes Allowable DeductionsRaymond MedinaОценок пока нет

- Ins3010 Final ThuếiДокумент3 страницыIns3010 Final ThuếiLinh DoОценок пока нет

- TY2019 - Fair Fight Action - Form 990-PДокумент37 страницTY2019 - Fair Fight Action - Form 990-PWashington ExaminerОценок пока нет

- Clarification Regarding Service Tax On Delayed Payment Charges CollectedДокумент2 страницыClarification Regarding Service Tax On Delayed Payment Charges Collectedpr_abhatОценок пока нет

- PDF Projected Income Statement and Balance SheetДокумент4 страницыPDF Projected Income Statement and Balance Sheetnavie VОценок пока нет

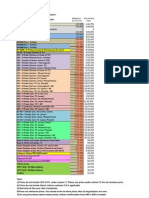

- Mindray Pricelist - Dec 11-Sales TeamДокумент1 страницаMindray Pricelist - Dec 11-Sales TeamNayan PatelОценок пока нет