Вам также может понравиться

- Questions 1 PDFДокумент10 страницQuestions 1 PDFdkishore28100% (1)

- Tinas RestaurantДокумент14 страницTinas Restaurantapi-3881551440% (1)

- AHLA-OSAC Hotel Assessment Form2017Документ21 страницаAHLA-OSAC Hotel Assessment Form2017Hervian LanangОценок пока нет

- Management Accounting: CMA Ontario Accelerated ProgramДокумент131 страницаManagement Accounting: CMA Ontario Accelerated ProgramArlene Diane OrozcoОценок пока нет

- Banquet GlossaryДокумент3 страницыBanquet GlossaryIdi Ramadhani100% (1)

- Welcoming Your Indian Guests: A Practical Guide for Hospitality and Tourism (Second Edition)От EverandWelcoming Your Indian Guests: A Practical Guide for Hospitality and Tourism (Second Edition)Оценок пока нет

- ToA.1830 - Accounting Changes and Errors - OnlineДокумент3 страницыToA.1830 - Accounting Changes and Errors - OnlineJolina ManceraОценок пока нет

- Drill ReceivablesДокумент3 страницыDrill ReceivablesGlecel BustrilloОценок пока нет

- PIG2016 Thailand v5 PDFДокумент13 страницPIG2016 Thailand v5 PDFakanagesОценок пока нет

- Operations Manual Table of Contents: 1. Introduction To The ManualДокумент7 страницOperations Manual Table of Contents: 1. Introduction To The ManualKrisha VittoОценок пока нет

- Buffalo Wild Wings Business Plan: Poised To ThriveДокумент39 страницBuffalo Wild Wings Business Plan: Poised To ThriveRose PerezОценок пока нет

- Hotel Chart of AccountsДокумент2 страницыHotel Chart of AccountsVivek BhadviyaОценок пока нет

- Pre Open ChklistДокумент10 страницPre Open Chklistchetan_jangidОценок пока нет

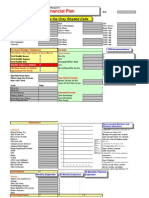

- Individual Financial Plan: Complete The Gray Shaded CellsДокумент6 страницIndividual Financial Plan: Complete The Gray Shaded Cellsraven505Оценок пока нет

- Cost and Management Accounting AccountingДокумент22 страницыCost and Management Accounting AccountingvyajivvОценок пока нет

- MarketingДокумент8 страницMarketingYasodha ChithuОценок пока нет

- Job Request: Unit Job Description QTYДокумент29 страницJob Request: Unit Job Description QTYRodnel MonceraОценок пока нет

- Berlitz Biz English 2 IGДокумент253 страницыBerlitz Biz English 2 IGMotanaОценок пока нет

- Domino's Pizza: Strategy and PolicyДокумент6 страницDomino's Pizza: Strategy and PolicyMathews JosephОценок пока нет

- Personal Monthly Budget: Division of Total Expenses ProjectedДокумент1 страницаPersonal Monthly Budget: Division of Total Expenses ProjectedMuhammad AtifОценок пока нет

- Restaurant StartupДокумент57 страницRestaurant Startuphaitham bedranОценок пока нет

- Personal Monthly BudgetДокумент4 страницыPersonal Monthly BudgetBrenda Queenbee MooreОценок пока нет

- Revenue ManagementДокумент11 страницRevenue ManagementRakesh DangolОценок пока нет

- Event Management and Catering: Entrep 106Документ29 страницEvent Management and Catering: Entrep 106John OpeñaОценок пока нет

- Mice ManagementДокумент38 страницMice ManagementDrexler BuenafeОценок пока нет

- Dominos ProjectДокумент9 страницDominos ProjectHarshitTripahtiОценок пока нет

- HRMДокумент24 страницыHRMHetvi GadaОценок пока нет

- Micros Opera Digital BookДокумент114 страницMicros Opera Digital BookKyla Joanna Sabareza Tomagan100% (1)

- Chart of Accounts and ReportingДокумент35 страницChart of Accounts and ReportingSafiullah KamawalОценок пока нет

- Advanced Revenue ManagementДокумент210 страницAdvanced Revenue ManagementMauricioAlejandroToroVegaОценок пока нет

- Convention ManagementДокумент16 страницConvention ManagementBhavna Sarkar100% (1)

- Food and Beverage Control Systems Can Help You Introduce The Same Financial Rigour To Your Dining Establishment or Catering Company That YouДокумент11 страницFood and Beverage Control Systems Can Help You Introduce The Same Financial Rigour To Your Dining Establishment or Catering Company That Younarinder singh saini100% (4)

- Advertising and Sales Promotion StrategyДокумент39 страницAdvertising and Sales Promotion Strategyshivakumar NОценок пока нет

- Marketing Plan Launching HotelДокумент9 страницMarketing Plan Launching HotelScarletОценок пока нет

- 1 Promotion MixДокумент39 страниц1 Promotion MixDrSachin SrivastavaОценок пока нет

- Chapter 3 Accounts Receivable May 2010Документ48 страницChapter 3 Accounts Receivable May 2010Berbagi UsahaОценок пока нет

- Sales Orientation ProcessДокумент3 страницыSales Orientation Processjitusingh2235Оценок пока нет

- Canadian Food Inspection AgencyДокумент37 страницCanadian Food Inspection AgencyDevon DennisОценок пока нет

- CostaCoffee CardДокумент8 страницCostaCoffee Cardpascal rosasОценок пока нет

- Front Office Associate Participants GuideДокумент100 страницFront Office Associate Participants GuideKim Adrian XuОценок пока нет

- Restaurant Marketing:: 5 Ways To Improve Your Restaurant's Cu Stomer LoyaltyДокумент2 страницыRestaurant Marketing:: 5 Ways To Improve Your Restaurant's Cu Stomer Loyaltyutkarsh singhОценок пока нет

- Code of Conduct Scandic Hotels Group Ab Publ 2017Документ3 страницыCode of Conduct Scandic Hotels Group Ab Publ 2017Instant ITServicengОценок пока нет

- Irfs and Us GaapДокумент7 страницIrfs and Us Gaapabissi67Оценок пока нет

- FHRAI - Reopening Manual For Hotels and Restaurants - 2020Документ44 страницыFHRAI - Reopening Manual For Hotels and Restaurants - 2020EclatОценок пока нет

- Opening A RestaurantДокумент29 страницOpening A RestaurantDavinder SinghОценок пока нет

- KRT ProposalДокумент13 страницKRT ProposalShafiq SsekittoОценок пока нет

- MacDonald Expanding GloballyДокумент7 страницMacDonald Expanding GloballykhannakasОценок пока нет

- Telephone Training: MED-EL Worldwide HeadquartersДокумент2 страницыTelephone Training: MED-EL Worldwide HeadquartersEdna Neri GuzmanОценок пока нет

- Reading-Finding HotelsДокумент2 страницыReading-Finding Hotelssarah mansorОценок пока нет

- Manpower Required in The HotelДокумент146 страницManpower Required in The Hotelparag0% (1)

- Questions Regarding QSR ChainДокумент1 страницаQuestions Regarding QSR ChainVishal SachdevОценок пока нет

- REDDIT Marketing Plan FY13Документ36 страницREDDIT Marketing Plan FY13breeze450Оценок пока нет

- Job Description: Job Title Conference and Banqueting Supervisor Department Scope of WorkДокумент4 страницыJob Description: Job Title Conference and Banqueting Supervisor Department Scope of WorktheauctionhunterОценок пока нет

- Next Generation Product Holding Units Mandate: Prince Castle Duke HS2 MercoДокумент2 страницыNext Generation Product Holding Units Mandate: Prince Castle Duke HS2 Mercopascal rosasОценок пока нет

- MPH Restaurant Bar Events Standards. Training Manual 2022Документ216 страницMPH Restaurant Bar Events Standards. Training Manual 2022Mervin CuyuganОценок пока нет

- Food and Beverage ManagerДокумент3 страницыFood and Beverage ManagerQuy TranxuanОценок пока нет

- Banquet Booking ProcedureДокумент3 страницыBanquet Booking ProcedureShadkhanОценок пока нет

- Uniform System of Accounts For Restaurants: Summary Version - Income Statement Full Service RestaurantДокумент6 страницUniform System of Accounts For Restaurants: Summary Version - Income Statement Full Service RestaurantAna Pedroso de LimaОценок пока нет

- Internship Supervisor Evaluation Form VISHAL KUMAR GUPTA, SEC (A)Документ3 страницыInternship Supervisor Evaluation Form VISHAL KUMAR GUPTA, SEC (A)VishalОценок пока нет

- The Robert Donato Approach to Enhancing Customer Service and Cultivating RelationshipsОт EverandThe Robert Donato Approach to Enhancing Customer Service and Cultivating RelationshipsОценок пока нет

- Actg Lecture8 CaseДокумент9 страницActg Lecture8 CaseOnline TutorОценок пока нет

- Sap Fi-11Документ73 страницыSap Fi-11Beema RaoОценок пока нет

- An Investigation of The Determinants of Bank Failure and Distress of Commercial and Merchant Banks in Zimbabwe (2011-2015)Документ3 страницыAn Investigation of The Determinants of Bank Failure and Distress of Commercial and Merchant Banks in Zimbabwe (2011-2015)Wayne MhlangaОценок пока нет

- Trainspotter 2014-09Документ38 страницTrainspotter 2014-09jcunha4740Оценок пока нет

- Rauf AshrafДокумент4 страницыRauf AshrafRauf AshrafОценок пока нет

- Memorandum of Agreement (MOA) : BetweenДокумент2 страницыMemorandum of Agreement (MOA) : BetweenGracee MedinaОценок пока нет

- COMPRO CB IndonesiaДокумент8 страницCOMPRO CB IndonesiaWilly AriefОценок пока нет

- 0124Документ88 страниц0124AqilaliraОценок пока нет

- Revision Notes On AlcoholsДокумент13 страницRevision Notes On AlcoholsMuredzwa MuzendaОценок пока нет

- Section (1) : 1. With Respect To Loading Timber Cargo in Question A) Explain Under What Circumstances, Vessel Is Able To Load To Lumber Load LinesДокумент6 страницSection (1) : 1. With Respect To Loading Timber Cargo in Question A) Explain Under What Circumstances, Vessel Is Able To Load To Lumber Load Linescanigetaccess100% (1)

- Branch Audit Guidelines 2018-19: Financial Management & Accounts DepartmentДокумент43 страницыBranch Audit Guidelines 2018-19: Financial Management & Accounts DepartmentBerkshire Hathway coldОценок пока нет

- Starbucks CaseДокумент3 страницыStarbucks CaseKiranОценок пока нет

- Cash ReceiptДокумент1 страницаCash ReceiptIrfanОценок пока нет

- 2015 (Monday) Room Ictss 10.00Pm 1) Ictzen Shirt 2) Technopreneur Startup Weekend 3) Robotic WorkshopДокумент5 страниц2015 (Monday) Room Ictss 10.00Pm 1) Ictzen Shirt 2) Technopreneur Startup Weekend 3) Robotic WorkshopMohd Sobri IsmailОценок пока нет

- Government Intervention in MarketsДокумент48 страницGovernment Intervention in MarketsSoha MalikОценок пока нет

- Development in Wagon FinalДокумент133 страницыDevelopment in Wagon Finalkr_abhijeet72356587100% (5)

- Profile The Leela Palaces Hotels and ResortsДокумент2 страницыProfile The Leela Palaces Hotels and Resortshafshu100% (1)

- Corality ModelOff Sample Answer Hard TimesДокумент81 страницаCorality ModelOff Sample Answer Hard TimesserpepeОценок пока нет

- Rheda City en Ballastless Track SystemДокумент12 страницRheda City en Ballastless Track SystemMaria Filip100% (1)

- Domar 1946Документ12 страницDomar 1946Stephany SandovalОценок пока нет

- LabourNet PresentationДокумент19 страницLabourNet PresentationcsendinfОценок пока нет

- Questionnaire Regarding The Problems Faced by The Passengers of Surat City Bus ServiceДокумент3 страницыQuestionnaire Regarding The Problems Faced by The Passengers of Surat City Bus ServiceTejas GardhariaОценок пока нет

- Toeic Practice TestДокумент56 страницToeic Practice TestHaris HaralambosОценок пока нет

- 2015 - INVESTMENT JOURNEY - Davuluri Omprakash PDFДокумент10 страниц2015 - INVESTMENT JOURNEY - Davuluri Omprakash PDFjohnthomastОценок пока нет

- National Accounts Blue Book 2016Документ101 страницаNational Accounts Blue Book 2016Shoaib AhmedОценок пока нет

- A K Srivastava - Essar PowerДокумент13 страницA K Srivastava - Essar PowerVishal SinghОценок пока нет

- Pizza Hut - Quantitative AnalysisДокумент6 страницPizza Hut - Quantitative AnalysisSrinivaas GanesanОценок пока нет

- Importance of IPRДокумент3 страницыImportance of IPRRathin BanerjeeОценок пока нет

- Bajaj Finance JP MorganДокумент38 страницBajaj Finance JP MorganNikhilKapoor29Оценок пока нет