Вам также может понравиться

- 08 Chapter 2Документ72 страницы08 Chapter 2Arshdeep KaurОценок пока нет

- Customer Relationship Management: A powerful tool for attracting and retaining customersОт EverandCustomer Relationship Management: A powerful tool for attracting and retaining customersРейтинг: 3.5 из 5 звезд3.5/5 (3)

- Customer Relationship ManagementДокумент16 страницCustomer Relationship ManagementAjay SahuОценок пока нет

- Project On CRM in Banking SectorДокумент65 страницProject On CRM in Banking SectorMukesh Manwani100% (1)

- Chapter-3 Customer Relationship Management in BanksДокумент21 страницаChapter-3 Customer Relationship Management in BanksAryan SharmaОценок пока нет

- Customer Relationship Marketing: To inspire good customer service behaviour, we must be able to measure customer experiences meaningfully.От EverandCustomer Relationship Marketing: To inspire good customer service behaviour, we must be able to measure customer experiences meaningfully.Оценок пока нет

- Participation of Employees in Customer Relationship Marketing: A Case of Indian Banking SectorДокумент25 страницParticipation of Employees in Customer Relationship Marketing: A Case of Indian Banking SectorNarayana ReddyОценок пока нет

- Index: SR No TopicsДокумент30 страницIndex: SR No Topicsdeepakmaru92Оценок пока нет

- Ere PortДокумент7 страницEre PortPayal SharmaОценок пока нет

- Customer Relationship ManagementДокумент15 страницCustomer Relationship ManagementTanoj PandeyОценок пока нет

- INDUSTRY: Banking Project Title: CRM in Axis BankДокумент7 страницINDUSTRY: Banking Project Title: CRM in Axis BankArup BoseОценок пока нет

- Desing of The StudyДокумент9 страницDesing of The StudyCh TarunОценок пока нет

- CRM:Banking Industry.: Submitted To: Submitted By: Prof. Nivedita Roy Nishant Mendiratta 09BS0001463Документ23 страницыCRM:Banking Industry.: Submitted To: Submitted By: Prof. Nivedita Roy Nishant Mendiratta 09BS0001463nishant_mendiratta_1Оценок пока нет

- CRM in BankingДокумент2 страницыCRM in BankingKaushik SameerОценок пока нет

- Executive Summary: The Report Explains The Concept of CRM in Private Bank With The Case Study On ICICI BankДокумент56 страницExecutive Summary: The Report Explains The Concept of CRM in Private Bank With The Case Study On ICICI BankKevin DarrylОценок пока нет

- CRM in Bank With Reference To SbiДокумент45 страницCRM in Bank With Reference To Sbishaikhdilshaad12373% (30)

- "Customer Relationship Management": IntroductionДокумент43 страницы"Customer Relationship Management": IntroductionsudhirОценок пока нет

- Customer Relationship Management in Bhel Company HaridwarДокумент43 страницыCustomer Relationship Management in Bhel Company HaridwarsudhirОценок пока нет

- RM AssignДокумент5 страницRM AssignSanjeev ThakurОценок пока нет

- CRM in Banking Sector.Документ38 страницCRM in Banking Sector.desaikrishna24Оценок пока нет

- CRM Automobile IndustryДокумент8 страницCRM Automobile IndustryKashish MehtaОценок пока нет

- (CRM) in Axis BankДокумент42 страницы(CRM) in Axis Bankkrupamayekar55% (11)

- Nfluence A 360-Degree View of Every Customer: A) Sales Force AutomationДокумент4 страницыNfluence A 360-Degree View of Every Customer: A) Sales Force AutomationAvantika SaxenaОценок пока нет

- CRM in Axis Bank - Stage 2 Mid-Review of The ProjectДокумент7 страницCRM in Axis Bank - Stage 2 Mid-Review of The ProjectShalini MahawarОценок пока нет

- Report On Use of Customer Relationship Management in BangladeshДокумент13 страницReport On Use of Customer Relationship Management in BangladeshSadi AminОценок пока нет

- Industry: Bankingproject Title: CRM in Axis Bank Group Members: Mangesh Jadhav Rajnish Dubey Sadiq Quadricsonia Sharmavarun GuptaДокумент12 страницIndustry: Bankingproject Title: CRM in Axis Bank Group Members: Mangesh Jadhav Rajnish Dubey Sadiq Quadricsonia Sharmavarun GuptaBhakti GuravОценок пока нет

- CRM Project: Submitted To: Submitted byДокумент12 страницCRM Project: Submitted To: Submitted byAshishОценок пока нет

- CRM FinalДокумент21 страницаCRM FinalHerleen KalraОценок пока нет

- Customer Relationship Management in Hotel IndustryДокумент66 страницCustomer Relationship Management in Hotel IndustryJas77794% (33)

- Customer Relationship Management (CRM) in Overall Banking Sector of BangladeshДокумент11 страницCustomer Relationship Management (CRM) in Overall Banking Sector of BangladeshAsifHasanОценок пока нет

- Customer Relationship ManagementДокумент66 страницCustomer Relationship Managementrocky gamerОценок пока нет

- Major Project ReportДокумент48 страницMajor Project Reportinderpreet kaurОценок пока нет

- Customer Relationship Management Project ReportДокумент19 страницCustomer Relationship Management Project ReportLokesh Krishnan100% (1)

- Chapter - I: 2010 Customer Relationship ManagementДокумент68 страницChapter - I: 2010 Customer Relationship ManagementShamil VazirОценок пока нет

- (Markenting) CRM SBICAP SECURITIESДокумент73 страницы(Markenting) CRM SBICAP SECURITIESsantoshnagane72Оценок пока нет

- Customer Relationship ManagementДокумент45 страницCustomer Relationship ManagementParag MoreОценок пока нет

- Customer Relationship Management in Hotel IndustryДокумент66 страницCustomer Relationship Management in Hotel IndustryFreddie Kpako JahОценок пока нет

- Customer Relationship Management - STДокумент10 страницCustomer Relationship Management - STDivyansh SinghОценок пока нет

- Business Research Methods Assignment: BY G.Deepthi 2T1-16 TPSДокумент6 страницBusiness Research Methods Assignment: BY G.Deepthi 2T1-16 TPSvinodmeghanaОценок пока нет

- 8 Yatish Joshi 1936 Research Communication VSRDIJBMR June 2013Документ4 страницы8 Yatish Joshi 1936 Research Communication VSRDIJBMR June 2013Rajni TyagiОценок пока нет

- Project 2k19Документ38 страницProject 2k19Abhijit SinghОценок пока нет

- CRM Project, SheratonДокумент16 страницCRM Project, SheratonSonu BansalОценок пока нет

- What Is Customer Relationship Management?Документ41 страницаWhat Is Customer Relationship Management?moregauravОценок пока нет

- Customer Relationship ManagementДокумент11 страницCustomer Relationship Managementdev_dbcОценок пока нет

- Customer Relationship ManagementДокумент58 страницCustomer Relationship ManagementMrinal BankaОценок пока нет

- Customer Relationship Management: Shikha Sehgal Rajesh Punia Tej Inder Singh Yogesh DbeyДокумент44 страницыCustomer Relationship Management: Shikha Sehgal Rajesh Punia Tej Inder Singh Yogesh DbeyyddubeyОценок пока нет

- Promotion Strategies of Customer Relations ManagementДокумент16 страницPromotion Strategies of Customer Relations ManagementRajeev ChinnappaОценок пока нет

- Final Capstone CRM - ReportДокумент39 страницFinal Capstone CRM - ReportakashОценок пока нет

- CRM The Most Valuable Component of Banking: Dr. Sujata Rao, Jinali PatelДокумент7 страницCRM The Most Valuable Component of Banking: Dr. Sujata Rao, Jinali PatelAshish KumarОценок пока нет

- MBA (BI) III Sem CRM in Banks Unit-3Документ28 страницMBA (BI) III Sem CRM in Banks Unit-3maheshgutam8756Оценок пока нет

- CRM in The Automobile Industry: Submitted By: Jatin Patel (75) Dhaval Goriya (29) Neha Shinde (103) Gumansinh RajputДокумент7 страницCRM in The Automobile Industry: Submitted By: Jatin Patel (75) Dhaval Goriya (29) Neha Shinde (103) Gumansinh RajputGumansinh RajputОценок пока нет

- Customer Relationship ManagementДокумент4 страницыCustomer Relationship Managementg peddaiahОценок пока нет

- A Study On Customer Relationship Management Practices in Banking SectorДокумент11 страницA Study On Customer Relationship Management Practices in Banking SectorStuti SrivastavaОценок пока нет

- Customer Relationship ManagementДокумент41 страницаCustomer Relationship Managementgoodwynj100% (1)

- Production Management Kari Session PlanДокумент5 страницProduction Management Kari Session PlanTanoj PandeyОценок пока нет

- CrudeДокумент2 страницыCrudeTanoj PandeyОценок пока нет

- Nelson Mandela LeadershipДокумент1 страницаNelson Mandela LeadershipTanoj PandeyОценок пока нет

- Analytical & Logical ReasoningДокумент8 страницAnalytical & Logical Reasoningkanishqthakur100% (2)

- Challenges Faced by Airlines SectorДокумент2 страницыChallenges Faced by Airlines SectorTanoj PandeyОценок пока нет

- Former Tata Group Chairman Ratan Tata Said The GroupДокумент4 страницыFormer Tata Group Chairman Ratan Tata Said The GroupTanoj PandeyОценок пока нет

- Trading Forex What Investors Need To KnowДокумент24 страницыTrading Forex What Investors Need To KnowTanoj PandeyОценок пока нет

- Hot ItДокумент26 страницHot ItTanoj PandeyОценок пока нет

- Gurgaon: Indiatimes The Economic TimesДокумент6 страницGurgaon: Indiatimes The Economic TimesTanoj PandeyОценок пока нет

- Marketing Strategy of Icici Bank': Tanoj PandeyДокумент5 страницMarketing Strategy of Icici Bank': Tanoj PandeyTanoj PandeyОценок пока нет

- Customer Relationship ManagementДокумент15 страницCustomer Relationship ManagementTanoj PandeyОценок пока нет

- Capital MarketsДокумент7 страницCapital MarketsTanoj PandeyОценок пока нет

- Introduction To Banking Sector: Marketing Strategies of ICICI BankДокумент32 страницыIntroduction To Banking Sector: Marketing Strategies of ICICI BankTanoj PandeyОценок пока нет

- Coffee Industry in IndiaДокумент3 страницыCoffee Industry in IndiaTanoj PandeyОценок пока нет

- Centurion Bank of PunjabДокумент2 страницыCenturion Bank of PunjabTanoj PandeyОценок пока нет

- G 20Документ2 страницыG 20Tanoj PandeyОценок пока нет

- Punjab and Sind Bank Services of Risk ManagementДокумент12 страницPunjab and Sind Bank Services of Risk Managementiyaps427100% (1)

- ExportДокумент28 страницExportNagarjun AithaОценок пока нет

- Average Daily Traffic On NH - 42 (2011)Документ25 страницAverage Daily Traffic On NH - 42 (2011)Anek AgrawalОценок пока нет

- Answer Legal FormsДокумент10 страницAnswer Legal FormsLean-Klair Jan GamateroОценок пока нет

- Romualdez Vs Civil Service CommissionДокумент1 страницаRomualdez Vs Civil Service CommissionFrancis Gillean OrpillaОценок пока нет

- Trust ReceiptsДокумент23 страницыTrust ReceiptskarenkierОценок пока нет

- FT Business EducationДокумент76 страницFT Business EducationDenis VarlamovОценок пока нет

- JP Morgan Chase Sues To Get Mortgage Loan Files Back From Ben Ezra... Ben Ezra Claims Chase Did Not Pay Its BillДокумент59 страницJP Morgan Chase Sues To Get Mortgage Loan Files Back From Ben Ezra... Ben Ezra Claims Chase Did Not Pay Its Bill83jjmackОценок пока нет

- Hkicl - Disclosure For HKD ChatsДокумент40 страницHkicl - Disclosure For HKD ChatsLawrence TamОценок пока нет

- Fema Add CHДокумент54 страницыFema Add CHMukesh DholakiaОценок пока нет

- Balance SheetДокумент2 страницыBalance SheetAbdul Samad ButtОценок пока нет

- Prepaid Instruments in India Feb 27Документ11 страницPrepaid Instruments in India Feb 27nish21inОценок пока нет

- Matrix Assessment of Pan-European Banks Capital Positions Relating To Basel III: Jan. '11Документ98 страницMatrix Assessment of Pan-European Banks Capital Positions Relating To Basel III: Jan. '11creditplumberОценок пока нет

- Guest Accounting, VTL, Weekly Bill BHM 2Документ4 страницыGuest Accounting, VTL, Weekly Bill BHM 2vickie_sunnie50% (2)

- T03 - Working Capital FinanceДокумент40 страницT03 - Working Capital FinanceJesha JotojotОценок пока нет

- MRAT - Annual Report - 2018 PDFДокумент147 страницMRAT - Annual Report - 2018 PDFdamas anggaОценок пока нет

- RBI Grade B Exam Preparation StrategyДокумент17 страницRBI Grade B Exam Preparation StrategysahilОценок пока нет

- Client AgreementДокумент10 страницClient AgreementAnonymous 4B1M0nwvvОценок пока нет

- Problem 7 - Group 1Документ8 страницProblem 7 - Group 1Francine Torres100% (4)

- Analyze The Roles of International Payment in An Open EconomyДокумент22 страницыAnalyze The Roles of International Payment in An Open EconomyNgô Giang Anh ThưОценок пока нет

- The World Bank: IBRD & IDA: Working For A World Free of PovertyДокумент28 страницThe World Bank: IBRD & IDA: Working For A World Free of PovertyManish TiwariОценок пока нет

- F06084145 PDFДокумент5 страницF06084145 PDFSharath rОценок пока нет

- Visa ReceiptДокумент1 страницаVisa ReceiptAnonymous Dkc838Оценок пока нет

- Guthrie-Jensen - Corporate ProfileДокумент8 страницGuthrie-Jensen - Corporate ProfileRalph GuzmanОценок пока нет

- NIC Account BenefitsДокумент4 страницыNIC Account BenefitsAnkit UpretyОценок пока нет

- IAE Student Prospective Guide San DiegoДокумент15 страницIAE Student Prospective Guide San DiegoNatalia Díaz GarcíaОценок пока нет

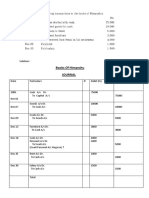

- Books of Himanshu JournalДокумент4 страницыBooks of Himanshu Journalrakesh19865Оценок пока нет

- Assignment No 1 CBLДокумент3 страницыAssignment No 1 CBLsingh rajnishОценок пока нет

- AGENCY, Doctrine of Apparent Authority GR 227990Документ2 страницыAGENCY, Doctrine of Apparent Authority GR 227990Gerard LeeОценок пока нет

- 02 Varun Nagar - Case HandoutДокумент2 страницы02 Varun Nagar - Case Handoutravi007kant100% (1)

- You Can't Joke About That: Why Everything Is Funny, Nothing Is Sacred, and We're All in This TogetherОт EverandYou Can't Joke About That: Why Everything Is Funny, Nothing Is Sacred, and We're All in This TogetherОценок пока нет

- Fascinate: How to Make Your Brand Impossible to ResistОт EverandFascinate: How to Make Your Brand Impossible to ResistРейтинг: 5 из 5 звезд5/5 (1)

- $100M Offers: How to Make Offers So Good People Feel Stupid Saying NoОт Everand$100M Offers: How to Make Offers So Good People Feel Stupid Saying NoРейтинг: 5 из 5 звезд5/5 (25)

- Obviously Awesome: How to Nail Product Positioning so Customers Get It, Buy It, Love ItОт EverandObviously Awesome: How to Nail Product Positioning so Customers Get It, Buy It, Love ItРейтинг: 4.5 из 5 звезд4.5/5 (152)

- Summary: $100M Leads: How to Get Strangers to Want to Buy Your Stuff by Alex Hormozi: Key Takeaways, Summary & Analysis IncludedОт EverandSummary: $100M Leads: How to Get Strangers to Want to Buy Your Stuff by Alex Hormozi: Key Takeaways, Summary & Analysis IncludedРейтинг: 3 из 5 звезд3/5 (6)

- $100M Leads: How to Get Strangers to Want to Buy Your StuffОт Everand$100M Leads: How to Get Strangers to Want to Buy Your StuffРейтинг: 5 из 5 звезд5/5 (19)

- Yes!: 50 Scientifically Proven Ways to Be PersuasiveОт EverandYes!: 50 Scientifically Proven Ways to Be PersuasiveРейтинг: 4 из 5 звезд4/5 (154)

- The House at Pooh Corner - Winnie-the-Pooh Book #4 - UnabridgedОт EverandThe House at Pooh Corner - Winnie-the-Pooh Book #4 - UnabridgedРейтинг: 4.5 из 5 звезд4.5/5 (5)

- Storytelling: A Guide on How to Tell a Story with Storytelling Techniques and Storytelling SecretsОт EverandStorytelling: A Guide on How to Tell a Story with Storytelling Techniques and Storytelling SecretsРейтинг: 4.5 из 5 звезд4.5/5 (72)

- Summary: Dotcom Secrets: The Underground Playbook for Growing Your Company Online with Sales Funnels by Russell Brunson: Key Takeaways, Summary & Analysis IncludedОт EverandSummary: Dotcom Secrets: The Underground Playbook for Growing Your Company Online with Sales Funnels by Russell Brunson: Key Takeaways, Summary & Analysis IncludedРейтинг: 5 из 5 звезд5/5 (2)

- Understanding Digital Marketing: Marketing Strategies for Engaging the Digital GenerationОт EverandUnderstanding Digital Marketing: Marketing Strategies for Engaging the Digital GenerationРейтинг: 4 из 5 звезд4/5 (22)

- Brand Identity Breakthrough: How to Craft Your Company's Unique Story to Make Your Products IrresistibleОт EverandBrand Identity Breakthrough: How to Craft Your Company's Unique Story to Make Your Products IrresistibleРейтинг: 4.5 из 5 звезд4.5/5 (48)

- How to Read People: The Complete Psychology Guide to Analyzing People, Reading Body Language, and Persuading, Manipulating and Understanding How to Influence Human BehaviorОт EverandHow to Read People: The Complete Psychology Guide to Analyzing People, Reading Body Language, and Persuading, Manipulating and Understanding How to Influence Human BehaviorРейтинг: 4.5 из 5 звезд4.5/5 (33)

- Jab, Jab, Jab, Right Hook: How to Tell Your Story in a Noisy Social WorldОт EverandJab, Jab, Jab, Right Hook: How to Tell Your Story in a Noisy Social WorldРейтинг: 4.5 из 5 звезд4.5/5 (18)

- Pre-Suasion: Channeling Attention for ChangeОт EverandPre-Suasion: Channeling Attention for ChangeРейтинг: 4.5 из 5 звезд4.5/5 (278)

- Dealers of Lightning: Xerox PARC and the Dawn of the Computer AgeОт EverandDealers of Lightning: Xerox PARC and the Dawn of the Computer AgeРейтинг: 4 из 5 звезд4/5 (88)

- Summary: Traction: Get a Grip on Your Business: by Gino Wickman: Key Takeaways, Summary, and AnalysisОт EverandSummary: Traction: Get a Grip on Your Business: by Gino Wickman: Key Takeaways, Summary, and AnalysisРейтинг: 5 из 5 звезд5/5 (10)

- Ca$hvertising: How to Use More than 100 Secrets of Ad-Agency Psychology to Make Big Money Selling Anything to AnyoneОт EverandCa$hvertising: How to Use More than 100 Secrets of Ad-Agency Psychology to Make Big Money Selling Anything to AnyoneРейтинг: 5 из 5 звезд5/5 (114)

- Visibility Marketing: The No-Holds-Barred Truth About What It Takes to Grab Attention, Build Your Brand, and Win New BusinessОт EverandVisibility Marketing: The No-Holds-Barred Truth About What It Takes to Grab Attention, Build Your Brand, and Win New BusinessРейтинг: 4.5 из 5 звезд4.5/5 (7)

- The Importance of Being Earnest: Classic Tales EditionОт EverandThe Importance of Being Earnest: Classic Tales EditionРейтинг: 4.5 из 5 звезд4.5/5 (44)

- Scientific Advertising: "Master of Effective Advertising"От EverandScientific Advertising: "Master of Effective Advertising"Рейтинг: 4.5 из 5 звезд4.5/5 (164)

- Summary: Influence: The Psychology of Persuasion by Robert B. Cialdini Ph.D.: Key Takeaways, Summary & AnalysisОт EverandSummary: Influence: The Psychology of Persuasion by Robert B. Cialdini Ph.D.: Key Takeaways, Summary & AnalysisРейтинг: 5 из 5 звезд5/5 (4)

- Summary: Range: Why Generalists Triumph in a Specialized World by David Epstein: Key Takeaways, Summary & Analysis IncludedОт EverandSummary: Range: Why Generalists Triumph in a Specialized World by David Epstein: Key Takeaways, Summary & Analysis IncludedРейтинг: 4.5 из 5 звезд4.5/5 (6)