Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Deed of Absolute Sale (House and Lot)Документ4 страницыDeed of Absolute Sale (House and Lot)Maureen Pátajo75% (8)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Builders Certification of Plans Specs Site HUD-92541Документ3 страницыBuilders Certification of Plans Specs Site HUD-92541The Pinnacle TeamОценок пока нет

- Builders Certification of Plans Specs Site HUD-92541Документ3 страницыBuilders Certification of Plans Specs Site HUD-92541The Pinnacle TeamОценок пока нет

- Contract of Lease - SampleДокумент3 страницыContract of Lease - SampleIryshell VillegasОценок пока нет

- Contract of Sale of Real PropertyДокумент2 страницыContract of Sale of Real PropertyNombs NomОценок пока нет

- Time Frame To Obtain Mortgage FinancingДокумент1 страницаTime Frame To Obtain Mortgage FinancingThe Pinnacle TeamОценок пока нет

- September-October 2010 NewsletterДокумент6 страницSeptember-October 2010 NewsletterThe Pinnacle TeamОценок пока нет

- How Should I Price My Home...Документ20 страницHow Should I Price My Home...The Pinnacle TeamОценок пока нет

- Are You A Positive or A NegativeДокумент2 страницыAre You A Positive or A NegativeThe Pinnacle TeamОценок пока нет

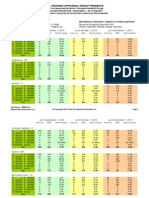

- A. L. Wagner Appraisal Group PresentsДокумент43 страницыA. L. Wagner Appraisal Group PresentsThe Pinnacle TeamОценок пока нет

- The Rentjuice Rent Index: Chicago Rents On The DeclineДокумент16 страницThe Rentjuice Rent Index: Chicago Rents On The DeclineThe Pinnacle TeamОценок пока нет

- Pinnacle Team July-August 2010 NewsletterДокумент7 страницPinnacle Team July-August 2010 NewsletterThe Pinnacle TeamОценок пока нет

- Pinnacle Team May-June 2010 NewsletterДокумент6 страницPinnacle Team May-June 2010 NewsletterThe Pinnacle TeamОценок пока нет

- Spot Approval QuestionnaireДокумент1 страницаSpot Approval QuestionnaireThe Pinnacle TeamОценок пока нет

- FHA Condo Process Attachment E Developer-Builder Certification To Condo RequirementsДокумент1 страницаFHA Condo Process Attachment E Developer-Builder Certification To Condo RequirementsThe Pinnacle TeamОценок пока нет

- Pinnacle Team March/April 2010 NewsletterДокумент6 страницPinnacle Team March/April 2010 NewsletterThe Pinnacle TeamОценок пока нет

- New FHA Condominium Matrix Version 2Документ12 страницNew FHA Condominium Matrix Version 2The Pinnacle TeamОценок пока нет

- Property Tax Reduction Article 2.22.10Документ2 страницыProperty Tax Reduction Article 2.22.10The Pinnacle TeamОценок пока нет

- FHA Approved-Limited Condo Questionnaire 12-09Документ1 страницаFHA Approved-Limited Condo Questionnaire 12-09The Pinnacle TeamОценок пока нет

- Pinnacle Team July NewsletterДокумент5 страницPinnacle Team July NewsletterThe Pinnacle Team100% (2)

- FHA FULL Condo Questionnaire 12-09Документ2 страницыFHA FULL Condo Questionnaire 12-09The Pinnacle TeamОценок пока нет

- FHA Spot ApprovalДокумент1 страницаFHA Spot ApprovalThe Pinnacle TeamОценок пока нет

- September 2009 NewsletterДокумент6 страницSeptember 2009 NewsletterThe Pinnacle TeamОценок пока нет

- 2235 W Lawrence #2Документ661 страница2235 W Lawrence #2The Pinnacle TeamОценок пока нет

- Home Buyer SeminarДокумент1 страницаHome Buyer SeminarThe Pinnacle TeamОценок пока нет

- 2009 Chicago Summer FestivalsДокумент1 страница2009 Chicago Summer FestivalsThe Pinnacle TeamОценок пока нет

- Pinnacle Team August NewsletterДокумент5 страницPinnacle Team August NewsletterThe Pinnacle TeamОценок пока нет

- 5.29.09 HUD AnnouncmentДокумент3 страницы5.29.09 HUD AnnouncmentThe Pinnacle TeamОценок пока нет

- Pinnacle Team April 2009 NewsletterДокумент6 страницPinnacle Team April 2009 NewsletterThe Pinnacle TeamОценок пока нет

- IRS FHB Tax Credit Update 3.18.09Документ2 страницыIRS FHB Tax Credit Update 3.18.09The Pinnacle TeamОценок пока нет

- Chicago Market Share YTD 4-17-09Документ2 страницыChicago Market Share YTD 4-17-09stevemcewen2992100% (1)

- Pinnacle Team May NewsletterДокумент5 страницPinnacle Team May NewsletterThe Pinnacle TeamОценок пока нет

- FHAMaxLimits 2.26.09Документ1 страницаFHAMaxLimits 2.26.09The Pinnacle TeamОценок пока нет

- Doha WWC Report - JLL May09Документ16 страницDoha WWC Report - JLL May09henrychavezhОценок пока нет

- A Quick History of Real Estate InvestingДокумент7 страницA Quick History of Real Estate Investingpetertumaini44Оценок пока нет

- One Year Residential Rental Agreement 3-25-12Документ5 страницOne Year Residential Rental Agreement 3-25-12yaro58Оценок пока нет

- Compromise AgreementДокумент2 страницыCompromise AgreementEnna FleurОценок пока нет

- Constitutional Law AssignmentДокумент19 страницConstitutional Law Assignmentfaisal NaushadОценок пока нет

- Succession 90 127Документ119 страницSuccession 90 127Sylver JanОценок пока нет

- Power Commercial and Industrial Corp. v. CAДокумент3 страницыPower Commercial and Industrial Corp. v. CAAMОценок пока нет

- Sale Deed of Agricultural LandДокумент1 страницаSale Deed of Agricultural Landگلوبل کنسلٹنٹسОценок пока нет

- Open House SheetsДокумент1 страницаOpen House Sheetsrealestate6199Оценок пока нет

- Estudi Regulació LloguerДокумент27 страницEstudi Regulació LloguerPúblico DiarioОценок пока нет

- Housing ToolkitДокумент28 страницHousing ToolkitJerry JohnsonОценок пока нет

- Aircraft ValuationДокумент4 страницыAircraft Valuationdjagger1Оценок пока нет

- UCC IRS Private BankingДокумент52 страницыUCC IRS Private BankingPETE97% (37)

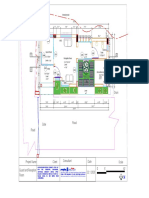

- Sheltech: SHELTECH TOWER: 60, Sheikh Russel Square, West PanthapathДокумент1 страницаSheltech: SHELTECH TOWER: 60, Sheikh Russel Square, West PanthapathMasum BillahОценок пока нет

- Analysis of The Montgomery County ZTA Zoning Amendment On Small CellsДокумент6 страницAnalysis of The Montgomery County ZTA Zoning Amendment On Small CellsSafe Tech For SchoolsОценок пока нет

- Benami TransactionДокумент103 страницыBenami TransactionMd AlamОценок пока нет

- 14 Things We Buying Home in Puerto RicoДокумент7 страниц14 Things We Buying Home in Puerto RicoTommyCasillas-GerenaОценок пока нет

- Property Law - Complete Final - 18.12.18Документ115 страницProperty Law - Complete Final - 18.12.18Niraj PandeyОценок пока нет

- Ramprastha Primera Sector 37D GurgaonДокумент2 страницыRamprastha Primera Sector 37D Gurgaonminku01Оценок пока нет

- Land Law SummaryДокумент160 страницLand Law SummaryDambisya Lyama John100% (2)

- Stockholders of Guanzon v. Register of Deeds of ManilaДокумент2 страницыStockholders of Guanzon v. Register of Deeds of ManilaDarla GreyОценок пока нет

- Power of Attorney To Transfer Ownership To Real EstateДокумент1 страницаPower of Attorney To Transfer Ownership To Real EstateIzabella KvistОценок пока нет

- Orduna V Fuentebella PDFДокумент16 страницOrduna V Fuentebella PDFmickeysdortega_41120Оценок пока нет

- Caniza Case and Republic V CAДокумент3 страницыCaniza Case and Republic V CAEmiaj Francinne MendozaОценок пока нет

- Stoney Crown Lease - Rental AgreementДокумент12 страницStoney Crown Lease - Rental AgreementRobert CallandОценок пока нет

- Cardoso v. Bank of AmericaДокумент32 страницыCardoso v. Bank of Americawoodruff1Оценок пока нет