Вам также может понравиться

- Godown Agreement For Somani CeramicsДокумент16 страницGodown Agreement For Somani CeramicsNitesh KotianОценок пока нет

- IndexДокумент10 страницIndexNitesh KotianОценок пока нет

- House Construction Cost CalculatorДокумент1 страницаHouse Construction Cost CalculatorNitesh KotianОценок пока нет

- Study The Following Pie PritiДокумент2 страницыStudy The Following Pie PritiNitesh KotianОценок пока нет

- Citizen CharterДокумент21 страницаCitizen CharterNitesh KotianОценок пока нет

- AmmanДокумент11 страницAmmanNitesh KotianОценок пока нет

- FC AssignmentДокумент22 страницыFC AssignmentNitesh KotianОценок пока нет

- Name: Momin Hajira Bano Abubakar: PRN No.: 2015017002713562Документ19 страницName: Momin Hajira Bano Abubakar: PRN No.: 2015017002713562Nitesh KotianОценок пока нет

- Anemia IntroductionДокумент15 страницAnemia IntroductionNitesh Kotian100% (1)

- Student Certificate PowerPoint Course CompletionДокумент10 страницStudent Certificate PowerPoint Course CompletionNitesh KotianОценок пока нет

- 3a00135 PDFДокумент207 страниц3a00135 PDFNitesh KotianОценок пока нет

- CertificateДокумент11 страницCertificateNitesh KotianОценок пока нет

- Consumer Protection Act, ProjectДокумент17 страницConsumer Protection Act, ProjectPREETAM252576% (171)

- To Study Role of Earthworm in Increasing SoilДокумент16 страницTo Study Role of Earthworm in Increasing SoilNitesh KotianОценок пока нет

- Study of Antibacterial Activity of Different Parts of Taro PlantДокумент8 страницStudy of Antibacterial Activity of Different Parts of Taro PlantNitesh KotianОценок пока нет

- Name: Momin Hajira Bano Abubakar: PRN No.: 2015017002713562Документ19 страницName: Momin Hajira Bano Abubakar: PRN No.: 2015017002713562Nitesh KotianОценок пока нет

- Study of Antibacterial Activity of Different Parts of Taro PlantДокумент8 страницStudy of Antibacterial Activity of Different Parts of Taro PlantNitesh KotianОценок пока нет

- Mosquito Density Are Significantly Correlated With Tree DensitiesДокумент6 страницMosquito Density Are Significantly Correlated With Tree DensitiesNitesh KotianОценок пока нет

- American RevolutionДокумент6 страницAmerican RevolutionNitesh KotianОценок пока нет

- Anand Parkhe Sem4Документ2 страницыAnand Parkhe Sem4Nitesh KotianОценок пока нет

- Full Schedule of VIVO IPL 2019Документ5 страницFull Schedule of VIVO IPL 2019Nitesh KotianОценок пока нет

- Certificate Save EarthДокумент10 страницCertificate Save EarthNitesh KotianОценок пока нет

- Causes and Types of Unemployment ExplainedДокумент1 страницаCauses and Types of Unemployment ExplainedNitesh KotianОценок пока нет

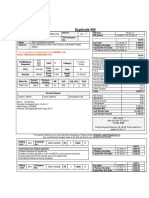

- Duplicate Electricity Bill Details and Payment InstructionsДокумент1 страницаDuplicate Electricity Bill Details and Payment InstructionsNitesh KotianОценок пока нет

- Economic InequalityДокумент3 страницыEconomic InequalityNitesh KotianОценок пока нет

- United Nations Development ProgrammeДокумент3 страницыUnited Nations Development ProgrammeNitesh KotianОценок пока нет

- Global SituationДокумент3 страницыGlobal SituationNitesh KotianОценок пока нет

- 8 Flowers One paraДокумент3 страницы8 Flowers One paraNitesh KotianОценок пока нет

- 1993 Latur EarthquakeДокумент2 страницы1993 Latur EarthquakeNitesh KotianОценок пока нет

- DrugДокумент8 страницDrugNitesh KotianОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- JFET and MOSFET quiz questionsДокумент4 страницыJFET and MOSFET quiz questionsfGОценок пока нет

- Data Analysis and Interpretation TABLE 3.1 Age of The RespondentДокумент58 страницData Analysis and Interpretation TABLE 3.1 Age of The RespondenteshuОценок пока нет

- Analytical Chemistry Hand-Out 1Документ11 страницAnalytical Chemistry Hand-Out 1Mark Jesson Datario100% (1)

- Difference Between Basel 1 2 and 3 - Basel 1 Vs 2 Vs 3Документ8 страницDifference Between Basel 1 2 and 3 - Basel 1 Vs 2 Vs 3Sonaal GuptaОценок пока нет

- MC ElroyДокумент2 страницыMC ElroyTanmay DastidarОценок пока нет

- Cost Functions Defined in EconomicsДокумент26 страницCost Functions Defined in EconomicsSoumya Ranjan SwainОценок пока нет

- The Copperbelt University BS 361: Entrepreneurship Skills: Lecture 2C: Business Startups K. Mulenga June, 2020Документ40 страницThe Copperbelt University BS 361: Entrepreneurship Skills: Lecture 2C: Business Startups K. Mulenga June, 2020Nkole MukukaОценок пока нет

- White Rust Removal and PreventionДокумент17 страницWhite Rust Removal and PreventionSunny OoiОценок пока нет

- Dubai Sme DefinitionДокумент28 страницDubai Sme DefinitionLallan SharmaОценок пока нет

- Burger and Fries Ingredients Burgers: Fries: KetchupДокумент5 страницBurger and Fries Ingredients Burgers: Fries: KetchupNobody2222Оценок пока нет

- Lion Air ETicket (IIZKUK) - NataliaДокумент2 страницыLion Air ETicket (IIZKUK) - NataliaNatalia LeeОценок пока нет

- Macro CH 11Документ48 страницMacro CH 11maria37066100% (3)

- Spreadsheet Concepts Using Microsoft Excel: ObjectivesДокумент26 страницSpreadsheet Concepts Using Microsoft Excel: ObjectivesYunita Yozpin AyanknyaRizalОценок пока нет

- Swanand Co-Op. Housing Society LTDДокумент2 страницыSwanand Co-Op. Housing Society LTDskumarsrОценок пока нет

- ACC 403 Final ExamДокумент5 страницACC 403 Final ExamSanada YukimuraОценок пока нет

- Supply Chain Re-Engineering Saves Elizabeth Arden $180MДокумент6 страницSupply Chain Re-Engineering Saves Elizabeth Arden $180MjaveriaОценок пока нет

- Shipping Bill of LadingДокумент1 страницаShipping Bill of LadingdonsterthemonsterОценок пока нет

- Port Pricing Final PresentationДокумент13 страницPort Pricing Final PresentationRomnic CagasОценок пока нет

- Product DiffrentiationДокумент26 страницProduct Diffrentiationoptimistic07100% (1)

- Mr. WegapitiyaДокумент10 страницMr. WegapitiyaNisrin Ali67% (3)

- Dissolution RegulationsДокумент15 страницDissolution Regulationsbhavk20Оценок пока нет

- SLFI610-Project Appraisal & FinanceДокумент2 страницыSLFI610-Project Appraisal & FinanceVivek GujralОценок пока нет

- Louis Dixon Pediatric Dentistry Trial Balance ReportДокумент4 страницыLouis Dixon Pediatric Dentistry Trial Balance ReportNabeelAhmedОценок пока нет

- China Soap Synthetic Detergent Market ReportДокумент10 страницChina Soap Synthetic Detergent Market ReportAllChinaReports.comОценок пока нет

- 1 IB Nature & ScopeДокумент19 страниц1 IB Nature & ScopePanav MohindraОценок пока нет

- CapbudhintДокумент3 страницыCapbudhintImran IdrisОценок пока нет

- Quiz - Act 07A: I. Theories: ProblemsДокумент2 страницыQuiz - Act 07A: I. Theories: ProblemsShawn Organo0% (1)

- 2011 1040NR-EZ Form - SampleДокумент2 страницы2011 1040NR-EZ Form - Samplefrankvanhaste100% (1)

- Chapter 5Документ37 страницChapter 5Ahmed ElbazОценок пока нет

- Founders Pie Calculator FinalДокумент3 страницыFounders Pie Calculator FinalAbbas AliОценок пока нет