Вам также может понравиться

- Assignment - 2Документ2 страницыAssignment - 2sohail merchantОценок пока нет

- Introduction To SociologyДокумент28 страницIntroduction To Sociologysohail merchant100% (1)

- Assignment 1Документ6 страницAssignment 1sohail merchantОценок пока нет

- Professor's Grade Book: Chart TitleДокумент3 страницыProfessor's Grade Book: Chart Titlesohail merchantОценок пока нет

- How To Create An Interview Winning CДокумент5 страницHow To Create An Interview Winning Csohail merchantОценок пока нет

- Computer TipsДокумент7 страницComputer Tipssohail merchantОценок пока нет

- News PDF-Notification 20152k15 AДокумент3 страницыNews PDF-Notification 20152k15 Asohail merchantОценок пока нет

- QuestionsДокумент28 страницQuestionssohail merchant100% (1)

- Pivot Easy WorkДокумент10 страницPivot Easy Worksohail merchantОценок пока нет

- Piece Rate System and Time Rate SystemДокумент6 страницPiece Rate System and Time Rate Systemsohail merchantОценок пока нет

- I e Presentation SeminarДокумент46 страницI e Presentation Seminarsohail merchantОценок пока нет

- HRM BookДокумент278 страницHRM Booksohail merchantОценок пока нет

- Ch20 InvestmentAppraisalДокумент32 страницыCh20 InvestmentAppraisalsohail merchantОценок пока нет

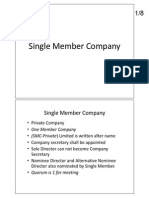

- Print SMCДокумент8 страницPrint SMCsohail merchantОценок пока нет

- Branch Banking CompleteДокумент195 страницBranch Banking Completesohail merchantОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Karachi Lahore Motorway Project: 911days From The Commencement DateДокумент3 страницыKarachi Lahore Motorway Project: 911days From The Commencement Dateمحمدعمران شريفОценок пока нет

- 8 December 2016 MoneylifeДокумент68 страниц8 December 2016 Moneylifethava477cegОценок пока нет

- UIN: 104N111V02 Page 1 of 3Документ3 страницыUIN: 104N111V02 Page 1 of 3vivek0955158Оценок пока нет

- Bid Document - t2017-015Документ131 страницаBid Document - t2017-015kingsolomon00Оценок пока нет

- Fidic Blue BookДокумент8 страницFidic Blue BookDona Alisyah SiregarОценок пока нет

- Starlight International Pvt. LTD 37, Jalan Besar SingaporeДокумент4 страницыStarlight International Pvt. LTD 37, Jalan Besar SingaporeMUHAMMAD ALDI NUGRAHAОценок пока нет

- Sub - Lease AgreementДокумент5 страницSub - Lease Agreementkamarin80Оценок пока нет

- Project On Punjab National BankДокумент86 страницProject On Punjab National BankPrakash Singh100% (1)

- An Analysis of Factors Affecting The Performance of Insurance Companies in ZimbabweДокумент21 страницаAn Analysis of Factors Affecting The Performance of Insurance Companies in ZimbabweTroden MukwasiОценок пока нет

- Becoming Your Own BankerДокумент14 страницBecoming Your Own Bankereagleye794% (17)

- Paper-6 080219Документ440 страницPaper-6 080219priya pОценок пока нет

- Digest For Bonifacio Bros V MoraДокумент2 страницыDigest For Bonifacio Bros V Moracookbooks&lawbooksОценок пока нет

- Contract Management PDFДокумент115 страницContract Management PDFS SITAPATIОценок пока нет

- Nicl Exam GK Capsule: 25 March, 2015Документ69 страницNicl Exam GK Capsule: 25 March, 2015Jatin YadavОценок пока нет

- MDRTДокумент44 страницыMDRTnava12Оценок пока нет

- Report 20160609171246Документ3 страницыReport 20160609171246Raakesh DoshiОценок пока нет

- San Pedro Local Development Investment Program 2017-2022Документ664 страницыSan Pedro Local Development Investment Program 2017-2022Igi EspeletaОценок пока нет

- Human Resource Management Exam 2Документ4 страницыHuman Resource Management Exam 2RobОценок пока нет

- 18 Recovery Housing Toolkit 5-3-2018Документ42 страницы18 Recovery Housing Toolkit 5-3-2018Russell SloanОценок пока нет

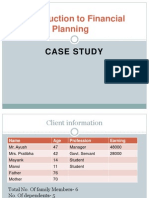

- Introduction To Financial Planning: Case StudyДокумент15 страницIntroduction To Financial Planning: Case StudyNilesh ChavanОценок пока нет

- Risk Management Worksheets Risk Assessment WorksheetДокумент4 страницыRisk Management Worksheets Risk Assessment Worksheetkapil ajmaniОценок пока нет

- Using The RIMS ERM Starter Kit 2013Документ12 страницUsing The RIMS ERM Starter Kit 2013ST KnightОценок пока нет

- KVICДокумент25 страницKVICAnjali MallisseryОценок пока нет

- Alok Annual Report-FY A2017-18Документ180 страницAlok Annual Report-FY A2017-18Aniket RoyОценок пока нет

- Npcil - 2.2 GCC - Supply1Документ67 страницNpcil - 2.2 GCC - Supply1srama_narayanan100% (1)

- 859 - By71h6kcls - Fire - Wordings For Add On Covers ClausesДокумент9 страниц859 - By71h6kcls - Fire - Wordings For Add On Covers ClausesShivОценок пока нет

- Carriage of Goods by Sea ActДокумент3 страницыCarriage of Goods by Sea ActOliverMastileroОценок пока нет

- A Project Report On AN Impact OF Celebrity Endorsement in InsuranceДокумент29 страницA Project Report On AN Impact OF Celebrity Endorsement in Insurancemegha mishraОценок пока нет

- I 843Документ6 страницI 843ayi imaduddinОценок пока нет

- Project Work On: Object ClauseДокумент19 страницProject Work On: Object ClauseShashi RanjanОценок пока нет