Вам также может понравиться

- Bond AccountingДокумент10 страницBond AccountingDaniela HogasОценок пока нет

- TOPIC 1 Accounting For Financial LiabilitiesДокумент45 страницTOPIC 1 Accounting For Financial LiabilitiesZe KhaiОценок пока нет

- Tut Lec 5 - Chap 80Документ6 страницTut Lec 5 - Chap 80Bella SeahОценок пока нет

- ACC 210P - Chapter 9 Lab Exercise SolutionsДокумент3 страницыACC 210P - Chapter 9 Lab Exercise SolutionscyclonextremeОценок пока нет

- EC10Документ18 страницEC10Muhammad AwaisОценок пока нет

- Bonds Payable: Bond PricesДокумент12 страницBonds Payable: Bond PricesRana SajidОценок пока нет

- Bank Management 8th Edition Koch Solutions ManualДокумент10 страницBank Management 8th Edition Koch Solutions Manualphoebeky78zbbz100% (26)

- Bank Management 8Th Edition Koch Solutions Manual Full Chapter PDFДокумент31 страницаBank Management 8Th Edition Koch Solutions Manual Full Chapter PDFBenjaminWeissazqe100% (11)

- CH 14Документ8 страницCH 14antonydonОценок пока нет

- Dwnload Full Business Ethics Ethical Decision Making and Cases 12th Edition Ferrell Solutions Manual PDFДокумент36 страницDwnload Full Business Ethics Ethical Decision Making and Cases 12th Edition Ferrell Solutions Manual PDFtrichitegraverye1bzv8100% (16)

- Reporting and Interpreting Bonds: Answers To QuestionsДокумент43 страницыReporting and Interpreting Bonds: Answers To QuestionsceojiОценок пока нет

- Activity Sheet In: Business FinanceДокумент8 страницActivity Sheet In: Business FinanceCatherine Larce100% (1)

- E136l7 Bond PricingДокумент21 страницаE136l7 Bond PricingRahul PatelОценок пока нет

- Chapter 13 HW SolutionsДокумент23 страницыChapter 13 HW SolutionsSijo VMОценок пока нет

- CH 14Документ8 страницCH 14Lemon VeinОценок пока нет

- FAR NotesДокумент3 страницыFAR NotesSoma Chatterjee DasОценок пока нет

- Time Value of MoneyДокумент18 страницTime Value of MoneyJunaid SubhaniОценок пока нет

- Fixed Income Portfolio MGMT - Butterfly SpreadsДокумент111 страницFixed Income Portfolio MGMT - Butterfly Spreadssawilson1Оценок пока нет

- Short and Long-Term: On Balance Sheet DebtДокумент8 страницShort and Long-Term: On Balance Sheet DebtNitin KumarОценок пока нет

- Refinancing Risk: Solutions For End-of-Chapter Questions and Problems: Chapter SevenДокумент6 страницRefinancing Risk: Solutions For End-of-Chapter Questions and Problems: Chapter SevenJeffОценок пока нет

- F9 - Mock A - AnswersДокумент15 страницF9 - Mock A - AnswerspavishneОценок пока нет

- Fixed Income Chapter4Документ51 страницаFixed Income Chapter4Sourabh pathakОценок пока нет

- Financial ManagementДокумент48 страницFinancial Managementalokthakur100% (1)

- AFM RevisionДокумент8 страницAFM RevisionSomabhizinisi MazibukoОценок пока нет

- NPVДокумент5 страницNPVMian UmarОценок пока нет

- Far410 Chapter 4 Non Current Liabilities 12 Nov 2013Документ25 страницFar410 Chapter 4 Non Current Liabilities 12 Nov 2013mr.nazir.shahidanОценок пока нет

- Chapter 12 Bond Portfolio MGMTДокумент41 страницаChapter 12 Bond Portfolio MGMTsharktale2828Оценок пока нет

- IM6. Fixed IncomeДокумент42 страницыIM6. Fixed IncomeZoon KiatОценок пока нет

- Sapm Compre Partb QPДокумент15 страницSapm Compre Partb QPXavier CharlesОценок пока нет

- Bodie Essentials Ch. 10 SolutionsДокумент18 страницBodie Essentials Ch. 10 SolutionsJPM190067% (6)

- Chapter 16: Fixed Income Portfolio ManagementДокумент20 страницChapter 16: Fixed Income Portfolio ManagementSilviu TrebuianОценок пока нет

- Fa4e SM Ch09Документ36 страницFa4e SM Ch09michaelkwok1100% (1)

- Bond Portfolio MGTДокумент22 страницыBond Portfolio MGTChandrabhan NathawatОценок пока нет

- Lecture (7) - (24-12-2023)Документ21 страницаLecture (7) - (24-12-2023)Abdulrahman YounesОценок пока нет

- Project Financial AppraisalДокумент81 страницаProject Financial Appraisallidya100% (1)

- FNCE 4820 Fall 2013 Midterm 1 With AnswersДокумент5 страницFNCE 4820 Fall 2013 Midterm 1 With AnswersDingo BabyОценок пока нет

- 7 7Документ11 страниц7 7Nad AdenanОценок пока нет

- 301 Chapter 14 Edition 15Документ31 страница301 Chapter 14 Edition 15Go TurpinОценок пока нет

- Solution Manual For Financial Institutions Markets and Money Kidwell Blackwell Whidbee Sias 11th EditionДокумент8 страницSolution Manual For Financial Institutions Markets and Money Kidwell Blackwell Whidbee Sias 11th EditionAmandaMartinxdwj100% (40)

- Noncurrent LiabilitiesДокумент29 страницNoncurrent LiabilitiesLuna MeowОценок пока нет

- M13.1 Chubb Corp ValuationДокумент16 страницM13.1 Chubb Corp ValuationrullyadhityaОценок пока нет

- Investments Global Edition 10th Edition Bodie Solutions ManualДокумент6 страницInvestments Global Edition 10th Edition Bodie Solutions Manuala609526046Оценок пока нет

- Chapter6 Matematika BusinessДокумент17 страницChapter6 Matematika BusinessKarlina DewiОценок пока нет

- Lecture On Amortization and Amortization ScheduleДокумент3 страницыLecture On Amortization and Amortization ScheduleAeiaОценок пока нет

- Long-Term Liabilities: QuestionsДокумент69 страницLong-Term Liabilities: QuestionsCh Radeel MurtazaОценок пока нет

- Booth Cleary 2nd Edition Chapter 6 - Bond Valuation and Interest RatesДокумент93 страницыBooth Cleary 2nd Edition Chapter 6 - Bond Valuation and Interest RatesQurat.ul.ain MumtazОценок пока нет

- Financing Part I: Debt: Chapter 14 in Spiceland See Example Excel Files File Names: Bonds and LeasesДокумент17 страницFinancing Part I: Debt: Chapter 14 in Spiceland See Example Excel Files File Names: Bonds and LeasesNurul LailiyahОценок пока нет

- Time Value of Money FormulasДокумент8 страницTime Value of Money FormulasrovosoloОценок пока нет

- Libby Financial Accounting Chapter10Документ8 страницLibby Financial Accounting Chapter10Jie Bo TiОценок пока нет

- Ch05 Mini CaseДокумент8 страницCh05 Mini CaseTia1977Оценок пока нет

- Kontabiliteti I Obligacioneve (Anglisht)Документ11 страницKontabiliteti I Obligacioneve (Anglisht)Vilma HoxhaОценок пока нет

- The Analysis and Valuation of Bonds: Answers To QuestionsДокумент4 страницыThe Analysis and Valuation of Bonds: Answers To QuestionsIsmat Jerin ChetonaОценок пока нет

- Bonds Payable - Part 2Документ6 страницBonds Payable - Part 2Elizabeth diane NOVENOОценок пока нет

- Ch20 SolutionsДокумент19 страницCh20 SolutionsAlexir Thatayaone NdovieОценок пока нет

- TCCB REVISIONДокумент44 страницыTCCB REVISION21070119Оценок пока нет

- Problem Set IV (9 Marks) : YTM/2) (n2)Документ5 страницProblem Set IV (9 Marks) : YTM/2) (n2)steve bobОценок пока нет

- Income Tax Department Sec 56Документ5 страницIncome Tax Department Sec 56Sourabh GargОценок пока нет

- Recent Dev On TPДокумент29 страницRecent Dev On TPSourabh GargОценок пока нет

- EY Doing Business in IndiaДокумент340 страницEY Doing Business in IndiaSourabh Garg50% (2)

- Income Tax Department Rule 11UAДокумент3 страницыIncome Tax Department Rule 11UASourabh GargОценок пока нет

- Dutch Compaies in IndiaДокумент28 страницDutch Compaies in IndiaSourabh GargОценок пока нет

- SPA GRP Profile 2014-15Документ33 страницыSPA GRP Profile 2014-15Sourabh GargОценок пока нет

- Companies Act GovernanceДокумент16 страницCompanies Act GovernanceSourabh GargОценок пока нет

- Companies Act 2013 Key Highlights and Analysis in MalaysiaДокумент52 страницыCompanies Act 2013 Key Highlights and Analysis in MalaysiatruthosisОценок пока нет

- PLC - Employee Share Plans in India - Regulatory OverviewДокумент21 страницаPLC - Employee Share Plans in India - Regulatory OverviewSourabh GargОценок пока нет

- Exit Options Under SEBI, RBI and Companies Act - MoneylifeДокумент6 страницExit Options Under SEBI, RBI and Companies Act - MoneylifeSourabh GargОценок пока нет

- Directory of Cement Companies in IndiaДокумент2 страницыDirectory of Cement Companies in IndiaSourabh Garg100% (1)

- 1pepulse EduДокумент40 страниц1pepulse EduSourabh GargОценок пока нет

- 15663valuation Standard V7-IcaiДокумент62 страницы15663valuation Standard V7-IcaiSourabh GargОценок пока нет

- Chapter IV Drfat Rules Under Companies Act 2013Документ53 страницыChapter IV Drfat Rules Under Companies Act 2013Sourabh GargОценок пока нет

- CA13Документ294 страницыCA13Knowitall77Оценок пока нет

- Real MortgageДокумент107 страницReal MortgageMarion Lawrence LaraОценок пока нет

- Jumia Travel, Hotel & Flight Booking - Rates & Pay Later HotelsДокумент2 страницыJumia Travel, Hotel & Flight Booking - Rates & Pay Later Hotelssayys1390Оценок пока нет

- HRP of RakbankДокумент36 страницHRP of RakbankRama KediaОценок пока нет

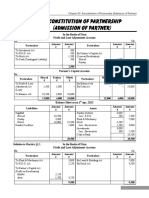

- 03 Reconstitution of Partnership Admission of Partner PDFДокумент24 страницы03 Reconstitution of Partnership Admission of Partner PDFBrawler Stars100% (3)

- Tally Inventory Question 6 (Rice Mill)Документ2 страницыTally Inventory Question 6 (Rice Mill)Suraj BiswakarmaОценок пока нет

- Intermediate Test 3Документ4 страницыIntermediate Test 3Hao Phan100% (2)

- Interview Schedule - FARMER Paddy Markerting in Thanjavur DistrictДокумент7 страницInterview Schedule - FARMER Paddy Markerting in Thanjavur DistrictRanjith Kumar MrkОценок пока нет

- Industrial SicknessДокумент19 страницIndustrial SicknessAnkit SoniОценок пока нет

- Financial Management Module I: Introduction: Finance and Related DisciplinesДокумент4 страницыFinancial Management Module I: Introduction: Finance and Related DisciplinesKhushbu SaxenaОценок пока нет

- Corporate BankingДокумент56 страницCorporate Bankingsujata_patil11214405Оценок пока нет

- High Credit RatingДокумент2 страницыHigh Credit RatingRajesh KumarОценок пока нет

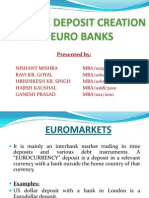

- Multiple Deposit Creation by Euro BanksДокумент20 страницMultiple Deposit Creation by Euro BankshrishikeshkrojhaОценок пока нет

- 1.1 Introduction To TopicДокумент55 страниц1.1 Introduction To Topickunal bankheleОценок пока нет

- Slides1 14 PDFДокумент240 страницSlides1 14 PDFVinay KumarОценок пока нет

- 2016.12 - Reader's DigestДокумент148 страниц2016.12 - Reader's Digestybarraza100% (1)

- Tutorial6 AnswersДокумент3 страницыTutorial6 AnswersTosin OjoОценок пока нет

- Study of Customer Satisfaction For The Loan Product Avaqilable at IIFLДокумент70 страницStudy of Customer Satisfaction For The Loan Product Avaqilable at IIFLDanya JainОценок пока нет

- Flight of FundsДокумент25 страницFlight of Fundsjue0% (1)

- Security Bank and Trust Company vs. GanДокумент2 страницыSecurity Bank and Trust Company vs. GanElaine HonradeОценок пока нет

- Ignou Bright Future For YouДокумент22 страницыIgnou Bright Future For YouAnshooman RayОценок пока нет

- Bunga Telur & Bally ShoesДокумент9 страницBunga Telur & Bally ShoesNur AzaliaОценок пока нет

- Memorial On Behalf of Respondent - Final Draft - 1.2.2017Документ32 страницыMemorial On Behalf of Respondent - Final Draft - 1.2.2017tanishq acharya100% (1)

- The Subprime Mortgage CrisisДокумент38 страницThe Subprime Mortgage Crisiseric3215Оценок пока нет

- Guide To The Secondary Market, 2015Документ92 страницыGuide To The Secondary Market, 2015ed_nycОценок пока нет

- LAND BANK OF THE PHILIPPINES vs. EDUARDO M. CACAYURANДокумент2 страницыLAND BANK OF THE PHILIPPINES vs. EDUARDO M. CACAYURANEmil Bautista100% (1)

- Importance of Loan Documents and Legal ImplicationДокумент64 страницыImportance of Loan Documents and Legal ImplicationVishnu TandiОценок пока нет

- Comparatie IFRS HGB PDFДокумент5 страницComparatie IFRS HGB PDFslisОценок пока нет

- Web of Debt - Thinking Outside The Box: How A Bankrupt Germany Solved Its Infrastructure ProblemsДокумент4 страницыWeb of Debt - Thinking Outside The Box: How A Bankrupt Germany Solved Its Infrastructure Problemssuperdude663Оценок пока нет

- Complaint BlankДокумент3 страницыComplaint BlankRoger Montero Jr.Оценок пока нет

- Mobility, LOS, CRM, LMS, Lead-gen-Underwriting, Field AutomationДокумент8 страницMobility, LOS, CRM, LMS, Lead-gen-Underwriting, Field AutomationAniket ThakurОценок пока нет