Вам также может понравиться

- Student of The Game: On High ROE StocksДокумент7 страницStudent of The Game: On High ROE StocksCanadianValueОценок пока нет

- A2A Vorm Vision Feb-10Документ10 страницA2A Vorm Vision Feb-10ccomstock3459Оценок пока нет

- Rofo 2018 ArДокумент18 страницRofo 2018 ArNate TobikОценок пока нет

- AVOA Avoca L.L.C. Annual Report 2019Документ16 страницAVOA Avoca L.L.C. Annual Report 2019kdwcapitalОценок пока нет

- DKAM ROE Reporter January 2016 PDFДокумент9 страницDKAM ROE Reporter January 2016 PDFJohn Hadriano Mellon FundОценок пока нет

- Assurance Service - Case 2 - WS 2016/2017Документ12 страницAssurance Service - Case 2 - WS 2016/2017RayCharlesCloud100% (1)

- Pershing Square 3Q-2016 Investor LetterДокумент16 страницPershing Square 3Q-2016 Investor LettersuperinvestorbulletiОценок пока нет

- QUCT 2016 FinancialsДокумент24 страницыQUCT 2016 FinancialskdwcapitalОценок пока нет

- Tollymore Letters To Partners Dec 2021Документ193 страницыTollymore Letters To Partners Dec 2021TBoone0Оценок пока нет

- The 2016 HEC-DowJones PE Performance Ranking ReportДокумент6 страницThe 2016 HEC-DowJones PE Performance Ranking ReportTDGoddardОценок пока нет

- Starboard Value LP Letter To NWL Shareholders 03.05.2018Документ10 страницStarboard Value LP Letter To NWL Shareholders 03.05.2018marketfolly.com100% (1)

- HighBridge GaveaДокумент20 страницHighBridge GaveaAnibal Wadih100% (1)

- The 2011 HEC-DowJones PE Performance Ranking ReportДокумент6 страницThe 2011 HEC-DowJones PE Performance Ranking ReportDan PrimackОценок пока нет

- Tutorial 9 Q & AДокумент2 страницыTutorial 9 Q & Achunlun87Оценок пока нет

- Greenhaven Road Capital Q1 2017Документ12 страницGreenhaven Road Capital Q1 2017superinvestorbulletiОценок пока нет

- Lemelson Capital Featured in HFMWeekДокумент32 страницыLemelson Capital Featured in HFMWeekamvona100% (1)

- Engaged Capital's Letter To Abercrombie & FitchДокумент9 страницEngaged Capital's Letter To Abercrombie & FitchKim BhasinОценок пока нет

- PremWatsaFairfaxNewsletter7 12-20-11Документ6 страницPremWatsaFairfaxNewsletter7 12-20-11able1Оценок пока нет

- EMBA Applied Value Investing (Ajdler) SP2016Документ3 страницыEMBA Applied Value Investing (Ajdler) SP2016darwin12Оценок пока нет

- Global Investment Returns Yearbook 2014Документ68 страницGlobal Investment Returns Yearbook 2014Rosetta RennerОценок пока нет

- Heuristic Biases in Investment Decision-Making and Perceived Market EfficiencyДокумент26 страницHeuristic Biases in Investment Decision-Making and Perceived Market EfficiencyDaniel Pandapotan MarpaungОценок пока нет

- Third Point LLC's Letter To NestleДокумент4 страницыThird Point LLC's Letter To NestleDrew HansenОценок пока нет

- Corsair Q2 14Документ3 страницыCorsair Q2 14marketfolly.comОценок пока нет

- Quarterly Commentary 2017 Q3Документ3 страницыQuarterly Commentary 2017 Q3Anonymous Ht0MIJОценок пока нет

- ACCT421 Detailed Course Outline, Term 2 2019-20 (Prof Andrew Lee) PDFДокумент7 страницACCT421 Detailed Course Outline, Term 2 2019-20 (Prof Andrew Lee) PDFnixn135Оценок пока нет

- Letters of The Manager Since 1998Документ111 страницLetters of The Manager Since 1998Lukas SavickasОценок пока нет

- Ben Graham and The Growth Investor: Presented To Bryant College April 10, 2008Документ115 страницBen Graham and The Growth Investor: Presented To Bryant College April 10, 2008bernhardfОценок пока нет

- The Purpose of This CourseДокумент6 страницThe Purpose of This CourseSasha GrayОценок пока нет

- Bank Financing As An Incentive For Earnings Management in Business Start-UpsДокумент41 страницаBank Financing As An Incentive For Earnings Management in Business Start-UpsShakeel AhmadОценок пока нет

- Cio Spotlight ReportДокумент9 страницCio Spotlight Reporthkm_gmat4849Оценок пока нет

- Syrah Resources FinalДокумент32 страницыSyrah Resources FinalViceroy40% (5)

- Orvana Minerals Report Stonecap SecuritiesДокумент22 страницыOrvana Minerals Report Stonecap SecuritiesOld School ValueОценок пока нет

- FinalCadburyLetter121807 PDFДокумент14 страницFinalCadburyLetter121807 PDFbillroberts981Оценок пока нет

- A Study ON "Working Capital Management" AT Sterlite Technologies LTDДокумент55 страницA Study ON "Working Capital Management" AT Sterlite Technologies LTDZankhana PatelОценок пока нет

- Atticus Global Letter To InvestorsДокумент2 страницыAtticus Global Letter To InvestorsDealBookОценок пока нет

- Graham & Doddsville Spring 2011 NewsletterДокумент27 страницGraham & Doddsville Spring 2011 NewsletterOld School ValueОценок пока нет

- BuybacksДокумент22 страницыBuybackssamson1190Оценок пока нет

- Ackman Letter May 2016Документ14 страницAckman Letter May 2016ZerohedgeОценок пока нет

- Gary Brode of Silver Arrow Investment Management: Long NCRДокумент0 страницGary Brode of Silver Arrow Investment Management: Long NCRcurrygoatОценок пока нет

- Jeff Saut Raymond James 12 28Документ5 страницJeff Saut Raymond James 12 28marketfolly.comОценок пока нет

- Letter To Bruce BerkowitzДокумент1 страницаLetter To Bruce BerkowitzmattpaulsОценок пока нет

- Empirical Studies in FinanceДокумент8 страницEmpirical Studies in FinanceAhmedMalikОценок пока нет

- From SpinPop To SpinBrush Entrepreneurial Lessons From John OsherДокумент8 страницFrom SpinPop To SpinBrush Entrepreneurial Lessons From John OsherAmrit SharmaОценок пока нет

- Pershing Square Q2 10 Investor LetterДокумент8 страницPershing Square Q2 10 Investor Lettereric695Оценок пока нет

- Conservatism in AccountingДокумент16 страницConservatism in AccountingThabo MolubiОценок пока нет

- WTW 3Q12 Earnings TranscriptДокумент14 страницWTW 3Q12 Earnings Transcriptrtao719Оценок пока нет

- Eileen Segall of Tildenrow Partners: Long On ReachLocalДокумент0 страницEileen Segall of Tildenrow Partners: Long On ReachLocalcurrygoatОценок пока нет

- Bruce Berkowitz's Fairholme Fund 2015 Semi-Annual Portfolio Manager's LettersДокумент5 страницBruce Berkowitz's Fairholme Fund 2015 Semi-Annual Portfolio Manager's LettersCharlie Tian100% (1)

- Coho Capital Letter 2016Документ13 страницCoho Capital Letter 2016raissakisОценок пока нет

- Lazard Secondary Market Report 2022Документ23 страницыLazard Secondary Market Report 2022Marcel LimОценок пока нет

- Lessons from Private Equity Any Company Can UseОт EverandLessons from Private Equity Any Company Can UseРейтинг: 4.5 из 5 звезд4.5/5 (12)

- The Well-Timed Strategy (Review and Analysis of Navarro's Book)От EverandThe Well-Timed Strategy (Review and Analysis of Navarro's Book)Оценок пока нет

- Summary: Less Is More: Review and Analysis of Jennings' BookОт EverandSummary: Less Is More: Review and Analysis of Jennings' BookОценок пока нет

- Strategic Leadership for Business Value Creation: Principles and Case StudiesОт EverandStrategic Leadership for Business Value Creation: Principles and Case StudiesОценок пока нет

- Stan Druckenmiller The Endgame SohnДокумент10 страницStan Druckenmiller The Endgame SohnCanadianValueОценок пока нет

- Greenlight UnlockedДокумент7 страницGreenlight UnlockedZerohedgeОценок пока нет

- Stan Druckenmiller Sohn TranscriptДокумент8 страницStan Druckenmiller Sohn Transcriptmarketfolly.com100% (1)

- KaseFundannualletter 2015Документ20 страницKaseFundannualletter 2015CanadianValueОценок пока нет

- Charlie Munger 2016 Daily Journal Annual Meeting Transcript 2 10 16 PDFДокумент18 страницCharlie Munger 2016 Daily Journal Annual Meeting Transcript 2 10 16 PDFaakashshah85Оценок пока нет

- Munger-Daily Journal Annual Mtg-Adam Blum Notes-2!10!16Документ12 страницMunger-Daily Journal Annual Mtg-Adam Blum Notes-2!10!16CanadianValueОценок пока нет

- The Stock Market As Monetary Policy Junkie Quantifying The Fed's Impact On The S P 500Документ6 страницThe Stock Market As Monetary Policy Junkie Quantifying The Fed's Impact On The S P 500dpbasicОценок пока нет

- Market Macro Myths Debts Deficits and DelusionsДокумент13 страницMarket Macro Myths Debts Deficits and DelusionsCanadianValueОценок пока нет

- OakTree Real EstateДокумент13 страницOakTree Real EstateCanadianValue100% (1)

- Hussman Funds Semi-Annual ReportДокумент84 страницыHussman Funds Semi-Annual ReportCanadianValueОценок пока нет

- Einhorn Consol PresentationДокумент107 страницEinhorn Consol PresentationCanadianValueОценок пока нет

- Einhorn Q4 2015Документ7 страницEinhorn Q4 2015CanadianValueОценок пока нет

- Absolute Return Oct 2015Документ9 страницAbsolute Return Oct 2015CanadianValue0% (1)

- Letter To Clients and ShareholdersДокумент3 страницыLetter To Clients and ShareholdersJulia Reynolds La RocheОценок пока нет

- Whitney Tilson Favorite Long and Short IdeasДокумент103 страницыWhitney Tilson Favorite Long and Short IdeasCanadianValueОценок пока нет

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Investor Call Re Valeant PharmaceuticalsДокумент39 страницInvestor Call Re Valeant PharmaceuticalsCanadianValueОценок пока нет

- Starboard Value LP AAP Presentation 09.30.15Документ23 страницыStarboard Value LP AAP Presentation 09.30.15marketfolly.com100% (1)

- DishtvlofДокумент343 страницыDishtvlofAmeya N. JoshiОценок пока нет

- Services/Functions of Merchant Banking (I) Corporate Counseling: Corporate Counseling Covers Counseling in The Form ofДокумент12 страницServices/Functions of Merchant Banking (I) Corporate Counseling: Corporate Counseling Covers Counseling in The Form ofTejalОценок пока нет

- Can Can Ethical Restraint Be Part of The Solution (Stephen Jordan)Документ3 страницыCan Can Ethical Restraint Be Part of The Solution (Stephen Jordan)lsw222Оценок пока нет

- Assignment # 4Документ4 страницыAssignment # 4Butt ArhamОценок пока нет

- Greystone Capital Pitchbook 7.14.2020Документ47 страницGreystone Capital Pitchbook 7.14.2020Sumit SagarОценок пока нет

- AXA Private Equity 2008 Annual ReportДокумент30 страницAXA Private Equity 2008 Annual ReportAsiaBuyoutsОценок пока нет

- Income Funds Annual Report PDFДокумент320 страницIncome Funds Annual Report PDFHarshal PatelОценок пока нет

- Warranty Expense and Bonds PayableДокумент3 страницыWarranty Expense and Bonds PayableAira Jaimee GonzalesОценок пока нет

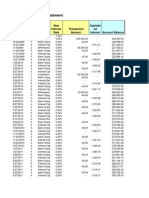

- Investment Account StatementДокумент6 страницInvestment Account StatementMorgan ThomasОценок пока нет

- Glass-Steagall ActДокумент43 страницыGlass-Steagall ActRishav Sinha100% (1)

- Literature Review CompletedДокумент13 страницLiterature Review CompletedRaji SinghОценок пока нет

- Project On Technical AnalysisДокумент32 страницыProject On Technical AnalysisShubham BhatiaОценок пока нет

- F321 - F319 - F329 Term Sheet 2016Документ2 страницыF321 - F319 - F329 Term Sheet 2016Chris CarmenОценок пока нет

- Indian Financial SystemДокумент57 страницIndian Financial SystemRanjeet RajputОценок пока нет

- Money MarketДокумент67 страницMoney MarketAvinash Veerendra TakОценок пока нет

- Fxrate 28 05 2023Документ2 страницыFxrate 28 05 2023ShohanОценок пока нет

- Investment Analysis and Stock Market OperationsДокумент45 страницInvestment Analysis and Stock Market Operationssurabhi24jain4439100% (1)

- Chapter 2 Analysis of Financial StatementДокумент18 страницChapter 2 Analysis of Financial StatementSuman ChaudharyОценок пока нет

- Uts Trading BlueprintДокумент4 страницыUts Trading BlueprintBudi MulyonoОценок пока нет

- New Project Awarded To DBL-DECO (JV) in The State of Maharashtra (Company Update)Документ2 страницыNew Project Awarded To DBL-DECO (JV) in The State of Maharashtra (Company Update)Shyam SunderОценок пока нет

- Silicon Valley Bank AssignmentДокумент2 страницыSilicon Valley Bank AssignmentMaazОценок пока нет

- All Values in The Economic System Are Measured in Terms of MoneyДокумент2 страницыAll Values in The Economic System Are Measured in Terms of MoneyYayank Emilia Darma100% (2)

- Customer Relationship Management inДокумент2 889 страницCustomer Relationship Management inDeepak ThakurОценок пока нет

- 10 HowToPredictForexBWДокумент6 страниц10 HowToPredictForexBWWihartono100% (2)

- Larry Williams Special Report 2017Документ15 страницLarry Williams Special Report 2017Alex Grey100% (1)

- DA4139 Level II CFA Mock Exam 1 AnswersДокумент84 страницыDA4139 Level II CFA Mock Exam 1 AnswersHelloWorldNowОценок пока нет

- B294-TMA-Fall 2023-2024-V1Документ4 страницыB294-TMA-Fall 2023-2024-V1adel.dahbour97Оценок пока нет

- Literature Review Foreign Exchange RiskДокумент6 страницLiterature Review Foreign Exchange Riskafmzxhvgfvprhm100% (1)

- CH 23 Hull Fundamentals 8 The DДокумент31 страницаCH 23 Hull Fundamentals 8 The DjlosamОценок пока нет

- Corporate Valuation, Value-Based Management, and Corporate GovernanceДокумент45 страницCorporate Valuation, Value-Based Management, and Corporate GovernanceAlem Abebe AryoОценок пока нет