Вам также может понравиться

- Budapest Research Forum Releases Q1 Report On Local Office MarketДокумент2 страницыBudapest Research Forum Releases Q1 Report On Local Office MarketallhungaryОценок пока нет

- PRF Q1 2010 Press Release enДокумент2 страницыPRF Q1 2010 Press Release encijblogОценок пока нет

- Euro SC Devt Report March 2010Документ3 страницыEuro SC Devt Report March 2010cijblogОценок пока нет

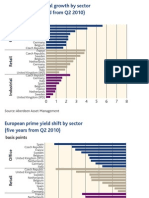

- Aberdeen Global Property Outlook 2010 ExtractДокумент1 страницаAberdeen Global Property Outlook 2010 ExtractcijblogОценок пока нет

- Euro SC Devt Report March 2010Документ3 страницыEuro SC Devt Report March 2010cijblogОценок пока нет

- 120%on Point - Polish Office Market Forecast: Back To TheДокумент1 страница120%on Point - Polish Office Market Forecast: Back To ThecijblogОценок пока нет

- PolAnd - IndusTRIAl REpoRT - Autumn 2009Документ1 страницаPolAnd - IndusTRIAl REpoRT - Autumn 2009cijblogОценок пока нет

- ProLogis' Committment To SustainabilityДокумент3 страницыProLogis' Committment To SustainabilitycijblogОценок пока нет

- eCIJ September 2009Документ64 страницыeCIJ September 2009cijblogОценок пока нет

- Opg PR H1 2009Документ10 страницOpg PR H1 2009cijblogОценок пока нет

- Industrial MR ENG 2009midДокумент2 страницыIndustrial MR ENG 2009midcijblogОценок пока нет

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Bratis Resi Pipeline 12 MonthДокумент2 страницыBratis Resi Pipeline 12 MonthcijblogОценок пока нет

- Warimpex Sells Csalogany Office BuildingДокумент2 страницыWarimpex Sells Csalogany Office BuildingcijblogОценок пока нет

- DTZ WarsawSummer2 4Документ3 страницыDTZ WarsawSummer2 4cijblogОценок пока нет

- WarsawRetail JLLДокумент1 страницаWarsawRetail JLLcijblogОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- LISTENING Countries in The WorldДокумент6 страницLISTENING Countries in The WorldVân KhánhОценок пока нет

- RTI ManualДокумент79 страницRTI Manualtnpsc2busarОценок пока нет

- La Campañia Maritima vs. Francisco Muñoz, 12 December 1907, GR No. L-3704Документ8 страницLa Campañia Maritima vs. Francisco Muñoz, 12 December 1907, GR No. L-3704Marianne Hope VillasОценок пока нет

- Sir Jeff FX GuideДокумент143 страницыSir Jeff FX GuideMadafaka MarobozuОценок пока нет

- It Landscape: InsideДокумент89 страницIt Landscape: InsideBogdan StanciuОценок пока нет

- Module 3Документ79 страницModule 3kakimog738Оценок пока нет

- Typeform Invoice BTLWMgTYQCPq91RjvДокумент1 страницаTypeform Invoice BTLWMgTYQCPq91RjvAakash vermaОценок пока нет

- An Integrative Framework of IWBДокумент21 страницаAn Integrative Framework of IWBpongthepОценок пока нет

- Coti GIW Rep 26x28LSA PDFДокумент3 страницыCoti GIW Rep 26x28LSA PDFjohan diazОценок пока нет

- Sue PisciottaДокумент3 страницыSue PisciottaSubhadip Das SarmaОценок пока нет

- Fundamentals of Business Law PDFДокумент358 страницFundamentals of Business Law PDFmikiyo90% (10)

- Evike Order 3939175Документ3 страницыEvike Order 3939175Carlos CrisostomoОценок пока нет

- Loreto School FeesДокумент4 страницыLoreto School FeesLaltu KarmakarОценок пока нет

- TM 2Документ28 страницTM 2ArsaОценок пока нет

- Pacl ScamДокумент24 страницыPacl ScamAindrila ChatterjeeОценок пока нет

- Notes On Intellectual Property (Ip) Law: Mylene I. Amerol - MacumbalДокумент41 страницаNotes On Intellectual Property (Ip) Law: Mylene I. Amerol - MacumbalAlain BarbaОценок пока нет

- A16z Comment Letter Final 1.4.21Документ21 страницаA16z Comment Letter Final 1.4.21ForkLogОценок пока нет

- Pro Forma Balance Sheet and Income StatementДокумент2 страницыPro Forma Balance Sheet and Income StatementMelinda AndrianiОценок пока нет

- Essentials of College and University AccountingДокумент121 страницаEssentials of College and University AccountingLith CloОценок пока нет

- Understanding The Leadership Spectrum - Developing The SkillsДокумент46 страницUnderstanding The Leadership Spectrum - Developing The SkillsSam PoliasОценок пока нет

- Bs in Business Administration Marketing Management: St. Nicolas College of Business and TechnologyДокумент6 страницBs in Business Administration Marketing Management: St. Nicolas College of Business and TechnologyMaria Charise TongolОценок пока нет

- Hdpe Pipe Electro Fusion Fittings Price ListДокумент18 страницHdpe Pipe Electro Fusion Fittings Price ListSantiago MoraОценок пока нет

- Chapter 7 Project Termination and Project Management Practices in BDДокумент19 страницChapter 7 Project Termination and Project Management Practices in BDbba19047Оценок пока нет

- Pt. Patco Elektronik Teknologi Standard Operating Procedure PurchasingДокумент8 страницPt. Patco Elektronik Teknologi Standard Operating Procedure Purchasingmochammad iqbal100% (1)

- Kaizen: A Lean Manufacturing Tool For Continuous ImprovementДокумент24 страницыKaizen: A Lean Manufacturing Tool For Continuous ImprovementSamrudhi PetkarОценок пока нет

- Std. X Ch. 3 Money and Credit WS (21 - 22)Документ3 страницыStd. X Ch. 3 Money and Credit WS (21 - 22)YASHVI MODIОценок пока нет

- Life InsuranceДокумент16 страницLife InsuranceKanika LalОценок пока нет

- Listening Test Unit 6Документ2 страницыListening Test Unit 6Xuân Bách0% (1)

- Internationalization of Tata Motors: Strategic Analysis Using Flowing Stream Strategy ProcessДокумент18 страницInternationalization of Tata Motors: Strategic Analysis Using Flowing Stream Strategy ProcessHedayatullah PashteenОценок пока нет

- CitikeyДокумент54 страницыCitikeyJacob PochinОценок пока нет