Вам также может понравиться

- Long Before Digital Effects Appeared, Animatronics Were Making CinematicДокумент16 страницLong Before Digital Effects Appeared, Animatronics Were Making CinematicOwolabi PetersОценок пока нет

- ProposalДокумент7 страницProposalOwolabi PetersОценок пока нет

- Effect of Motivation On Employee Performance in Public Middle Level TechnicalДокумент11 страницEffect of Motivation On Employee Performance in Public Middle Level TechnicalOwolabi PetersОценок пока нет

- Project ProposalДокумент9 страницProject ProposalOwolabi PetersОценок пока нет

- Awosanya Victoria Afolake: Address - 26, Rev Oluwatimiro Avenue, Elepe, Ikorodu, Lagos 08031991825,08118424762Документ2 страницыAwosanya Victoria Afolake: Address - 26, Rev Oluwatimiro Avenue, Elepe, Ikorodu, Lagos 08031991825,08118424762Owolabi PetersОценок пока нет

- Igbowukwu ArtДокумент6 страницIgbowukwu ArtOwolabi PetersОценок пока нет

- New CV Owolabi Peters CCNA, MCITPДокумент3 страницыNew CV Owolabi Peters CCNA, MCITPOwolabi PetersОценок пока нет

- Chapter Two Review of LiteratureДокумент28 страницChapter Two Review of LiteratureOwolabi PetersОценок пока нет

- Name: Ukoha Chidiuto Elizabeth Matric: 1409072032 DEPT.: Mass Communication HND Ii Course: Intro To Science Writing Applied ScienceДокумент6 страницName: Ukoha Chidiuto Elizabeth Matric: 1409072032 DEPT.: Mass Communication HND Ii Course: Intro To Science Writing Applied ScienceOwolabi PetersОценок пока нет

- Project Proposal ON Maintaining Food Hygiene Standards To Combat Food Poisoning in The Hotel Industry in Hotel BY Azeez Sekinat Motunrayo 1505012040Документ7 страницProject Proposal ON Maintaining Food Hygiene Standards To Combat Food Poisoning in The Hotel Industry in Hotel BY Azeez Sekinat Motunrayo 1505012040Owolabi Peters50% (2)

- Chapter Three 3.0 Materials and Methods 3.1 Experimental UnitsДокумент2 страницыChapter Three 3.0 Materials and Methods 3.1 Experimental UnitsOwolabi PetersОценок пока нет

- Dare's Project Proposal NewДокумент5 страницDare's Project Proposal NewOwolabi PetersОценок пока нет

- Human Behavior and Interpersonal CommДокумент11 страницHuman Behavior and Interpersonal CommOwolabi PetersОценок пока нет

- Project Proposal On The Impact of Use of Models On Patronage of A Product (Case Study of Mary Kay) by Olatoyegun Maria Folashade 1409072122Документ5 страницProject Proposal On The Impact of Use of Models On Patronage of A Product (Case Study of Mary Kay) by Olatoyegun Maria Folashade 1409072122Owolabi PetersОценок пока нет

- The Role of Nigerian Stock Exchange in Industrial DevelopmentДокумент61 страницаThe Role of Nigerian Stock Exchange in Industrial DevelopmentOwolabi PetersОценок пока нет

- Chapter One 1.1 Background To The StudyДокумент7 страницChapter One 1.1 Background To The StudyOwolabi PetersОценок пока нет

- The Origin of ReligionДокумент1 страницаThe Origin of ReligionOwolabi PetersОценок пока нет

- Cable 31Документ6 страницCable 31Owolabi PetersОценок пока нет

- Chapter Two LatestДокумент13 страницChapter Two LatestOwolabi PetersОценок пока нет

- Name: Akin-Lawrence Fisayo Esther Matric: 134072015 Course: International Communication and World PressДокумент6 страницName: Akin-Lawrence Fisayo Esther Matric: 134072015 Course: International Communication and World PressOwolabi PetersОценок пока нет

- Name: Akintayo Kehinde Monsurat Matric: 134072081 Course: International Communication and World PressДокумент4 страницыName: Akintayo Kehinde Monsurat Matric: 134072081 Course: International Communication and World PressOwolabi PetersОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Two Brain MetricsДокумент27 страницTwo Brain MetricsJay MikeОценок пока нет

- Government of Kerala: Rs. Rs. RsДокумент25 страницGovernment of Kerala: Rs. Rs. RsmuhammedОценок пока нет

- 9 Bank of The Phil. Islands vs. Intermediate Appellate Court PDFДокумент7 страниц9 Bank of The Phil. Islands vs. Intermediate Appellate Court PDFKristabelleCapaОценок пока нет

- UntitledДокумент8 страницUntitledRae SlaughterОценок пока нет

- Chapter 8: Cash and Bank Management Daily Procedures: ObjectivesДокумент26 страницChapter 8: Cash and Bank Management Daily Procedures: ObjectivesArturo GonzalezОценок пока нет

- Training Report On Anand RathiДокумент92 страницыTraining Report On Anand Rathirahulsogani123Оценок пока нет

- FINA1904 - ALL Weitzel - Spring 2019Документ11 страницFINA1904 - ALL Weitzel - Spring 2019JamesОценок пока нет

- Act1104midterm Exam Wit AnsДокумент9 страницAct1104midterm Exam Wit AnsDyen100% (1)

- EconomicsДокумент10 страницEconomicsCalvinОценок пока нет

- Income Tax Law & Practice Unit 4Документ8 страницIncome Tax Law & Practice Unit 4MuskanОценок пока нет

- AE 111 Final Summative Assessment 2Документ3 страницыAE 111 Final Summative Assessment 2Djunah ArellanoОценок пока нет

- GU215RG Post To Home Address: SurreyДокумент1 страницаGU215RG Post To Home Address: SurreyhelikacarvalhoОценок пока нет

- 04 2013-2014 Financial AgreementДокумент2 страницы04 2013-2014 Financial Agreementapi-234678525Оценок пока нет

- External Debt Development and Management: Presentations On IndiaДокумент22 страницыExternal Debt Development and Management: Presentations On IndiaYasser KhanОценок пока нет

- What Is EMD in Contract Work - Google SearchДокумент3 страницыWhat Is EMD in Contract Work - Google SearchRanjanОценок пока нет

- Merchant BankingДокумент49 страницMerchant BankingChandrika DasОценок пока нет

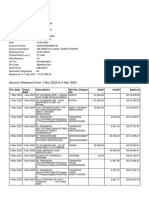

- Account Statement From 1 Mar 2023 To 4 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент2 страницыAccount Statement From 1 Mar 2023 To 4 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancesameer bawejaОценок пока нет

- This Is A System-Generated Statement. Hence, It Does Not Require Any SignatureДокумент6 страницThis Is A System-Generated Statement. Hence, It Does Not Require Any SignatureSachinОценок пока нет

- Valuation Part 2Документ82 страницыValuation Part 2Dương Thu TràОценок пока нет

- DIY Discharge Debt GuideДокумент4 страницыDIY Discharge Debt GuideAnthony VinsonОценок пока нет

- Finanacial Performance Analysis of HDFC BankДокумент54 страницыFinanacial Performance Analysis of HDFC BankSharuk KhanОценок пока нет

- BP Amoco (B)Документ32 страницыBP Amoco (B)Arnab RoyОценок пока нет

- AssignmentДокумент7 страницAssignmentMona VimlaОценок пока нет

- Basic Guidance To AccountingДокумент5 страницBasic Guidance To AccountingAishwarya ShelarОценок пока нет

- 4 AdjustmentДокумент19 страниц4 AdjustmentMina AmirОценок пока нет

- Investment Undertakings PDFДокумент64 страницыInvestment Undertakings PDFDianneОценок пока нет

- Unit 1Документ92 страницыUnit 1Amrit KaurОценок пока нет

- Commercial Law Review Cases Batch Recto LawДокумент12 страницCommercial Law Review Cases Batch Recto LawKarmaranthОценок пока нет

- Yes BankДокумент9 страницYes Bankरायटर लेखनवालाОценок пока нет

- The Nigerian Financial System at A Glance - Monetary Policy DepartmentДокумент356 страницThe Nigerian Financial System at A Glance - Monetary Policy DepartmentAgbons EbohonОценок пока нет