Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Act of Spiritual Communion S A L: Aint Lphonsus IgouriДокумент4 страницыAct of Spiritual Communion S A L: Aint Lphonsus IgouriFrancis Rey GayaniloОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Emergency Planning and Crisis ManagementДокумент111 страницEmergency Planning and Crisis ManagementFrancis Rey Gayanilo100% (1)

- Kingdom of SpainДокумент5 страницKingdom of SpainFrancis Rey GayaniloОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Consumer Chapter 5Документ4 страницыConsumer Chapter 5Francis Rey GayaniloОценок пока нет

- Hot Pursuit ArrestДокумент6 страницHot Pursuit ArrestFrancis Rey GayaniloОценок пока нет

- List of Textbooks - CMA BSBA-MMДокумент9 страницList of Textbooks - CMA BSBA-MMFrancis Rey GayaniloОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- College of Management & Accountancy Ad - Feast 2014 For TV AdsДокумент1 страницаCollege of Management & Accountancy Ad - Feast 2014 For TV AdsFrancis Rey GayaniloОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- BeijingДокумент1 страницаBeijingFrancis Rey GayaniloОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Advertising Judging CriteriaДокумент2 страницыAdvertising Judging CriteriaFrancis Rey Gayanilo100% (3)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Do You Know?: Put The Months in Order by Writing A Number On Each PageДокумент2 страницыDo You Know?: Put The Months in Order by Writing A Number On Each PageFrancis Rey GayaniloОценок пока нет

- Cost SheetДокумент4 страницыCost SheetQuestionscastle FriendОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- FMID Mid Mock Spring 22Документ2 страницыFMID Mid Mock Spring 22Umer FarooqОценок пока нет

- Solution Chapter 23 MilanДокумент3 страницыSolution Chapter 23 MilanAngelica GaliciaОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Valuation NotesДокумент2 страницыValuation NotesveeranjaneyuluОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- BKash Performance Analysis & ValuationДокумент12 страницBKash Performance Analysis & ValuationZeehenul IshfaqОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- CFA二级 财务报表 习题 PDFДокумент272 страницыCFA二级 财务报表 习题 PDFNGOC NHIОценок пока нет

- Capital Budgeting, Cash Flows & Decision Making ProcessДокумент47 страницCapital Budgeting, Cash Flows & Decision Making ProcessAnifahchannie PacalnaОценок пока нет

- Ex2 Accounting For FOHДокумент5 страницEx2 Accounting For FOHMhelren DE LA PEnAОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Paper - 4: Taxation Section A: Income Tax Law Part - II: Receipts PaymentsДокумент29 страницPaper - 4: Taxation Section A: Income Tax Law Part - II: Receipts PaymentsVaishnavi ShindeОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Lesson 7 Working Capital ManagementДокумент30 страницLesson 7 Working Capital ManagementDavid Lumaban GatdulaОценок пока нет

- CRI - Solved Valuation Practical Sums - CS Vaibhav Chitlangia - Yes Academy, PuneДокумент37 страницCRI - Solved Valuation Practical Sums - CS Vaibhav Chitlangia - Yes Academy, Punegopika mundraОценок пока нет

- Quiz 2 Problem - SolutionДокумент9 страницQuiz 2 Problem - SolutionCharice Anne VillamarinОценок пока нет

- FI515 Homework1Документ5 страницFI515 Homework1andiemaeОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Simple Question Practice ReviewДокумент9 страницSimple Question Practice ReviewVirgilio VelascoОценок пока нет

- MicroCap Review Spring 2018Документ110 страницMicroCap Review Spring 2018Planet MicroCap Review MagazineОценок пока нет

- Accounting Equation - Part 2Документ48 страницAccounting Equation - Part 2Krrish BosamiaОценок пока нет

- Week 3 Tutorial SolutionsДокумент31 страницаWeek 3 Tutorial SolutionsalexandraОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Acc June 2018 PaperДокумент24 страницыAcc June 2018 PaperSarudzai MutsaОценок пока нет

- Chap. 9 12Документ58 страницChap. 9 122vpsrsmg7jОценок пока нет

- Compensation ManagementДокумент64 страницыCompensation ManagementNagireddy KalluriОценок пока нет

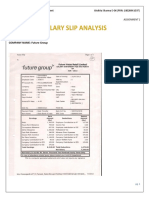

- Sector: Retail COMPANY NAME: Future GroupДокумент3 страницыSector: Retail COMPANY NAME: Future GroupAkshita SharmaОценок пока нет

- Concierge Service Business PlanДокумент35 страницConcierge Service Business PlanTamer KhattabОценок пока нет

- Trading ATR GuppyДокумент11 страницTrading ATR Guppylaxmicc100% (3)

- WING Investor Presentation IR Website 2018 WingstopДокумент37 страницWING Investor Presentation IR Website 2018 WingstopAla BasterОценок пока нет

- Finance 301 Exam 1 Flashcards - QuizletДокумент11 страницFinance 301 Exam 1 Flashcards - QuizletPhil SingletonОценок пока нет

- Final Accounts With AdjustmentsДокумент4 страницыFinal Accounts With AdjustmentsDivyaman RamawatОценок пока нет

- Itad Bir Ruling No. 044-21Документ9 страницItad Bir Ruling No. 044-21Crizedhen VardeleonОценок пока нет

- Eco211 Chapter 7Документ42 страницыEco211 Chapter 7Awang AizatОценок пока нет

- Human Capital Metrics and Analytics Assessing The Evidence - tcm18 22291 PDFДокумент64 страницыHuman Capital Metrics and Analytics Assessing The Evidence - tcm18 22291 PDFSyra RehmanОценок пока нет