Вам также может понравиться

- StatementДокумент2 страницыStatementLuis HarrisonОценок пока нет

- 2018 Coleman Tax Return PDFДокумент46 страниц2018 Coleman Tax Return PDFJonathan Brinton100% (1)

- Copy B-To Be Filed With Employee's FEDERAL Tax ReturnДокумент1 страницаCopy B-To Be Filed With Employee's FEDERAL Tax ReturnJoshua WagonerОценок пока нет

- EIN and Biz RegistrationДокумент2 страницыEIN and Biz RegistrationmaufunctОценок пока нет

- General Payroll, Employment and DeductionsДокумент6 страницGeneral Payroll, Employment and DeductionsJosh LeBlancОценок пока нет

- Forbes 2018 Tax GuideДокумент16 страницForbes 2018 Tax GuideJerry WhittonОценок пока нет

- 16 Don'T-Miss Tax DeductionsДокумент4 страницы16 Don'T-Miss Tax DeductionsGon FloОценок пока нет

- 1040es Estimated Tax 2014 For IndividualsДокумент12 страниц1040es Estimated Tax 2014 For IndividualsClaudia MaldonadoОценок пока нет

- PayStatement D0655147Документ1 страницаPayStatement D0655147Anonymous O61KvPgОценок пока нет

- 2012 Ontario Tax FormДокумент2 страницы2012 Ontario Tax FormHassan MhОценок пока нет

- On-Site Guide (BS 7671 - 2018) (Electrical Regulations)Документ4 страницыOn-Site Guide (BS 7671 - 2018) (Electrical Regulations)Farshid AhmadiОценок пока нет

- 2022 46-1240832 XXX-XX-8976 1410.00: CORRECTED (If Checked)Документ2 страницы2022 46-1240832 XXX-XX-8976 1410.00: CORRECTED (If Checked)Minerva BetancourtОценок пока нет

- Request For Transcript of Tax ReturnДокумент2 страницыRequest For Transcript of Tax ReturnJulie Payne-King100% (2)

- F 1040 EsДокумент12 страницF 1040 EsEndu EnduroОценок пока нет

- Credit For The Elderly or The Disabled: Publication 524Документ16 страницCredit For The Elderly or The Disabled: Publication 524api-115350234Оценок пока нет

- Benefit Verification LetterДокумент4 страницыBenefit Verification LetterDonna BridgesОценок пока нет

- RP 2013 30Документ4 страницыRP 2013 30forbesadmin100% (2)

- View AttachmentДокумент6 страницView AttachmentAlvin NgОценок пока нет

- RA 9504 Amending NIRC Section 34 (L)Документ2 страницыRA 9504 Amending NIRC Section 34 (L)RB BalanayОценок пока нет

- Superannuation and Retirement Planning AdviceДокумент16 страницSuperannuation and Retirement Planning Adviceapi-337581948Оценок пока нет

- Redundancy Payments Are TaxedДокумент2 страницыRedundancy Payments Are TaxedVivian KongОценок пока нет

- Form 1040-ES: Purpose of This PackageДокумент12 страницForm 1040-ES: Purpose of This PackageCaliCain MendezОценок пока нет

- td1 13eДокумент2 страницыtd1 13eMel McSweeneyОценок пока нет

- Household Employer's Tax Guide: Future DevelopmentsДокумент16 страницHousehold Employer's Tax Guide: Future DevelopmentsTezadeLicentaОценок пока нет

- Income Based Repayment Plan Request and or RenewalДокумент5 страницIncome Based Repayment Plan Request and or RenewalaquarianflowerОценок пока нет

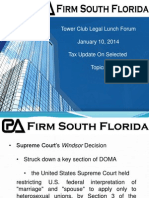

- Tax & Budget: After Doma: Tax Filing Faqs For Same-Sex Married CouplesДокумент3 страницыTax & Budget: After Doma: Tax Filing Faqs For Same-Sex Married CouplesExactCPAОценок пока нет

- Professional Judgment FaqДокумент2 страницыProfessional Judgment FaqAndrew WillingtonОценок пока нет

- An Assignment of Tax Planning On "Tax System in United States of America"Документ23 страницыAn Assignment of Tax Planning On "Tax System in United States of America"Akash NathwaniОценок пока нет

- Iowa W4Документ2 страницыIowa W4ts0m3Оценок пока нет

- Reference Id: Entitledto-10957291 Your Income: Entitlement Yearly Weekly Notes and GuidanceДокумент12 страницReference Id: Entitledto-10957291 Your Income: Entitlement Yearly Weekly Notes and GuidanceJohnny AlfaОценок пока нет

- Saver'S Tax Credit For Contributions by Individuals To Employer Retirement Plans and IrasДокумент5 страницSaver'S Tax Credit For Contributions by Individuals To Employer Retirement Plans and IrasIRSОценок пока нет

- It's December 31. Do You Know Where Your Money Is?: Collaborative Financial Solutions, LLCДокумент4 страницыIt's December 31. Do You Know Where Your Money Is?: Collaborative Financial Solutions, LLCJanet BarrОценок пока нет

- Factsheet: Family Tax BenefitДокумент5 страницFactsheet: Family Tax BenefitdhibuОценок пока нет

- Year-Round Tax Saving Tips: Vow To Be More EfficientДокумент4 страницыYear-Round Tax Saving Tips: Vow To Be More EfficientSrinivas ThoutaОценок пока нет

- Calculate SalaryДокумент15 страницCalculate SalaryShahjahan MohammedОценок пока нет

- 1453104607550Документ10 страниц1453104607550JGОценок пока нет

- Income Taxes: Key ConceptsДокумент10 страницIncome Taxes: Key ConceptsErika BОценок пока нет

- On The Precipice: The "Fiscal Cliff": Collaborative Financial Solutions, LLCДокумент4 страницыOn The Precipice: The "Fiscal Cliff": Collaborative Financial Solutions, LLCJanet BarrОценок пока нет

- Irvs GovnДокумент4 страницыIrvs Govnanaga1982Оценок пока нет

- A Guide To Terms and Conditions: Advanced Learning LoanДокумент16 страницA Guide To Terms and Conditions: Advanced Learning LoanAnca BodianОценок пока нет

- Income TaxationДокумент12 страницIncome TaxationMonica Jarabelo RamintasОценок пока нет

- Howdoi Adjust My Tax Withholding?: Publication 919Документ20 страницHowdoi Adjust My Tax Withholding?: Publication 919randyfranklinОценок пока нет

- What Is Taxable Income?: Key TakeawaysДокумент4 страницыWhat Is Taxable Income?: Key TakeawaysBella AyabОценок пока нет

- SP Fairer Charging LeafletДокумент2 страницыSP Fairer Charging LeafletFauzan Luthfi A MОценок пока нет

- Preparing For EOFY June 2011Документ2 страницыPreparing For EOFY June 2011nsfpОценок пока нет

- Income-Driven Repayment Plan Request How To Complete YourДокумент13 страницIncome-Driven Repayment Plan Request How To Complete YourAnonymous 6jR6DuОценок пока нет

- Surviving the New Tax Landscape: Smart Savings, Investment and Estate Planning StrategiesОт EverandSurviving the New Tax Landscape: Smart Savings, Investment and Estate Planning StrategiesОценок пока нет

- 2020.4 Coronavirus Stimulus Package F.A.Q. - Checks, Unemployment, Layoffs and More - The New York TimesДокумент12 страниц2020.4 Coronavirus Stimulus Package F.A.Q. - Checks, Unemployment, Layoffs and More - The New York TimesgioanelaОценок пока нет

- Gr9 12lesson9 PDFДокумент10 страницGr9 12lesson9 PDFbekbek12Оценок пока нет

- Claiming DependentsДокумент9 страницClaiming DependentschloeiskingОценок пока нет

- LEGT2751 Lecture 1Документ14 страницLEGT2751 Lecture 1reflecti0nОценок пока нет

- Minnesota Property Tax Refund: Forms and InstructionsДокумент28 страницMinnesota Property Tax Refund: Forms and InstructionsJeffery MeyerОценок пока нет

- Tax Impact of Job LossДокумент7 страницTax Impact of Job LossbullyrayОценок пока нет

- Personal Finance Another Perspective: Tax PlanningДокумент50 страницPersonal Finance Another Perspective: Tax PlanningcrazysidzОценок пока нет

- Your Guide To Auto-EnrolmentДокумент5 страницYour Guide To Auto-EnrolmentnikОценок пока нет

- td1 Fill 04 16eДокумент2 страницыtd1 Fill 04 16eAlec RichardsonОценок пока нет

- Taxable Income and Tax Payable For Individuals: Lesson 2 Tax Credits ContinuedДокумент37 страницTaxable Income and Tax Payable For Individuals: Lesson 2 Tax Credits ContinuedXi ChenОценок пока нет

- WWW - Humanservices.gov - Au SPW Customer Forms Resources Modjy-1211enДокумент17 страницWWW - Humanservices.gov - Au SPW Customer Forms Resources Modjy-1211enLeslie BrownОценок пока нет

- ACC 330 Final Project Formal Letter To Client TemplateДокумент4 страницыACC 330 Final Project Formal Letter To Client TemplateBREANNA JOHNSONОценок пока нет

- Income Driven Repayment FormДокумент13 страницIncome Driven Repayment Formtumi50Оценок пока нет

- Form 1040-ES (NR) : U.S. Estimated Tax For Nonresident Alien IndividualsДокумент9 страницForm 1040-ES (NR) : U.S. Estimated Tax For Nonresident Alien IndividualsBrokerAОценок пока нет

- En 05 11011 PDFДокумент28 страницEn 05 11011 PDFdawnОценок пока нет

- DHS-PUB-1010 - 243538 - 7 Important Things About Programs & ServicesДокумент38 страницDHS-PUB-1010 - 243538 - 7 Important Things About Programs & ServicesAryas VajraОценок пока нет

- Tower Club Legal Lunch Forum January 10, 2014 Tax Update On Selected TopicsДокумент32 страницыTower Club Legal Lunch Forum January 10, 2014 Tax Update On Selected TopicsPeter Rudolph, CPAОценок пока нет

- Help With Your Rent and Council Tax: ProofsДокумент28 страницHelp With Your Rent and Council Tax: Proofsjason_preciousОценок пока нет

- Eligibility NoticeДокумент17 страницEligibility NoticeDJPhrostОценок пока нет

- Ca De-4Документ4 страницыCa De-4Kevin Marcos FelicianoОценок пока нет

- MCFP Outreach-Mar 09 2012Документ11 страницMCFP Outreach-Mar 09 2012Milius CommandОценок пока нет

- Draft Nolan For Governor LetterДокумент4 страницыDraft Nolan For Governor LetterFluenceMediaОценок пока нет

- A. Program and Budget Activity DetailДокумент4 страницыA. Program and Budget Activity DetailRachel E. Stassen-BergerОценок пока нет

- FergusonДокумент19 страницFergusonJessica McBrideОценок пока нет

- Letter To The Governor's General CounselДокумент37 страницLetter To The Governor's General CounselMinnesota Public RadioОценок пока нет

- Speaker Daudt Letter To Governor DaytonДокумент2 страницыSpeaker Daudt Letter To Governor DaytonFluenceMediaОценок пока нет

- Opa141792 101916Документ11 страницOpa141792 101916Rachel E. Stassen-BergerОценок пока нет

- Christopher William ChamberlinДокумент2 страницыChristopher William ChamberlinRachel E. Stassen-BergerОценок пока нет

- Supplemental Payments To EmployeesДокумент19 страницSupplemental Payments To EmployeesRachel E. Stassen-BergerОценок пока нет

- Secretary of State PDFДокумент28 страницSecretary of State PDFRachel E. Stassen-Berger100% (1)

- Order Other 1Документ4 страницыOrder Other 1Rachel E. Stassen-BergerОценок пока нет

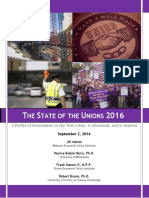

- State of The Unions Minnesota 2016 FINALДокумент26 страницState of The Unions Minnesota 2016 FINALRachel E. Stassen-BergerОценок пока нет

- MN Economy FINAL PDFДокумент40 страницMN Economy FINAL PDFRachel E. Stassen-BergerОценок пока нет

- State of Minnesota in Court of Appeals A15-1579Документ13 страницState of Minnesota in Court of Appeals A15-1579Rachel E. Stassen-BergerОценок пока нет

- 05 27 2016 Joe Hoppe Volunteer CommДокумент9 страниц05 27 2016 Joe Hoppe Volunteer CommRachel E. Stassen-BergerОценок пока нет

- 16.04.19 Statement Champion and Hayden RE Target FieldДокумент2 страницы16.04.19 Statement Champion and Hayden RE Target FieldRachel E. Stassen-BergerОценок пока нет

- 2016.4.1 Champion Col JamarClarkДокумент3 страницы2016.4.1 Champion Col JamarClarkRachel E. Stassen-BergerОценок пока нет

- Disclose Act BillДокумент2 страницыDisclose Act BillRachel E. Stassen-BergerОценок пока нет

- County Audits: Special ReviewДокумент34 страницыCounty Audits: Special ReviewRachel E. Stassen-BergerОценок пока нет

- SchoenДокумент1 страницаSchoenRachel E. Stassen-BergerОценок пока нет

- 2015 11 09 GMD Letter To Daudt Hann On Commissioners Managers Compensation PlanДокумент2 страницы2015 11 09 GMD Letter To Daudt Hann On Commissioners Managers Compensation PlanRachel E. Stassen-BergerОценок пока нет

- Corporation Application For Tentative Refund: Sign HereДокумент1 страницаCorporation Application For Tentative Refund: Sign HereIRSОценок пока нет

- Resident BookletДокумент32 страницыResident BookletGopal GopinathОценок пока нет

- US Internal Revenue Service: I1040 - 1992Документ84 страницыUS Internal Revenue Service: I1040 - 1992IRSОценок пока нет

- CH 1 - Class NotesДокумент12 страницCH 1 - Class NotesAndrew EngelhardtОценок пока нет

- Sgs India Private Limited: Sgs House 4B, A.S. Marg, Vikhroli (W) Mumbai - 400083 Payslip For The Month - Jul 2017Документ1 страницаSgs India Private Limited: Sgs House 4B, A.S. Marg, Vikhroli (W) Mumbai - 400083 Payslip For The Month - Jul 2017Santosh Kumar KurellaОценок пока нет

- Gross Taxable Income Tax DueДокумент19 страницGross Taxable Income Tax DueEdcelyn SamaniegoОценок пока нет

- Net Operating Losses (Nols) For Individuals, Estates, and TrustsДокумент12 страницNet Operating Losses (Nols) For Individuals, Estates, and TrustsAdi PutraОценок пока нет

- Earned Income Tax CreditДокумент1 страницаEarned Income Tax CreditkevinpadamsОценок пока нет

- Advanced Scenario 7 - Austin Drake (2018)Документ8 страницAdvanced Scenario 7 - Austin Drake (2018)Center for Economic Progress100% (2)

- Part III-Investment Interest Expense Deduction: Form 4952 (2009)Документ1 страницаPart III-Investment Interest Expense Deduction: Form 4952 (2009)Afzal ImamОценок пока нет

- Alien Residency Examples - IRSДокумент1 страницаAlien Residency Examples - IRSHaribabu PalneediОценок пока нет

- Guide To Taxation of Employee Disability Benefits: Standard Insurance CompanyДокумент26 страницGuide To Taxation of Employee Disability Benefits: Standard Insurance CompanyJacen BondsОценок пока нет

- 919e 2020-01-05 1578224820631Документ10 страниц919e 2020-01-05 1578224820631BrianHwang100% (1)

- LeAnn Bobleter Sargent Bankruptcy Income Records Maple Grove City Council MemberДокумент12 страницLeAnn Bobleter Sargent Bankruptcy Income Records Maple Grove City Council MemberghostgripОценок пока нет

- 1098-T Copy B: Tuition StatementДокумент2 страницы1098-T Copy B: Tuition StatementJonathan EllisОценок пока нет

- Solutions To Self-Study Problems: Chapter 1 The Individual Income Tax ReturnДокумент84 страницыSolutions To Self-Study Problems: Chapter 1 The Individual Income Tax ReturnTiffy LouiseОценок пока нет

- ACC 317 Homework CH 23Документ2 страницыACC 317 Homework CH 23leelee0302Оценок пока нет

- Instructions For Form 940: Future DevelopmentsДокумент16 страницInstructions For Form 940: Future DevelopmentsHotfootballmomОценок пока нет

- TANF Extension Reduces FundingДокумент2 страницыTANF Extension Reduces FundingPatricia DillonОценок пока нет

- Income Tax Refund ChartДокумент2 страницыIncome Tax Refund ChartKelly Phillips ErbОценок пока нет