Вам также может понравиться

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Besanko HarvardДокумент228 страницBesanko Harvardkjmnlkmh100% (1)

- Inventory AuditДокумент26 страницInventory AuditTiffany SmithОценок пока нет

- Corporate Financial AnalysisДокумент21 страницаCorporate Financial AnalysisMOHD.ARISH100% (1)

- Problem Set Mod 1Документ4 страницыProblem Set Mod 1Lindsay MadeloОценок пока нет

- Financial Statement Analysis of Bank - A Case Study CompletedДокумент62 страницыFinancial Statement Analysis of Bank - A Case Study CompletedJaiswal R SanjayОценок пока нет

- SBI Annual Report Highlights Growth and TransformationДокумент241 страницаSBI Annual Report Highlights Growth and TransformationArjaxОценок пока нет

- PDCA ModelДокумент1 страницаPDCA ModelTiffany SmithОценок пока нет

- FSCДокумент12 страницFSCTiffany SmithОценок пока нет

- SM Case - Strategic AlliancesДокумент2 страницыSM Case - Strategic AlliancesTiffany SmithОценок пока нет

- Organizing and Controlling Profit CentersДокумент3 страницыOrganizing and Controlling Profit CentersTiffany SmithОценок пока нет

- Riza Haditia Saputri 1121002041Документ3 страницыRiza Haditia Saputri 1121002041Tiffany SmithОценок пока нет

- Minggu 7 Case 7-1 SPMДокумент2 страницыMinggu 7 Case 7-1 SPMTiffany SmithОценок пока нет

- Reta Sharfina Tahar 1111002006 Case 10-1 Variance Analysis ProblemsДокумент2 страницыReta Sharfina Tahar 1111002006 Case 10-1 Variance Analysis ProblemsTiffany SmithОценок пока нет

- Summary of Starbucks' Management: Change and Innovation at StarbucksДокумент3 страницыSummary of Starbucks' Management: Change and Innovation at StarbucksTiffany SmithОценок пока нет

- Case 6 - 2 and Seminar 3 ExcersisesДокумент3 страницыCase 6 - 2 and Seminar 3 ExcersisesStany D'melloОценок пока нет

- Case StudyДокумент42 страницыCase StudyBrian MayolОценок пока нет

- Syllabus: Course DescriptionДокумент7 страницSyllabus: Course DescriptionTiffany SmithОценок пока нет

- Teori AkuntansiДокумент6 страницTeori AkuntansiTiffany SmithОценок пока нет

- AEB14 SM CH17 v2Документ31 страницаAEB14 SM CH17 v2RonLiu350% (1)

- Expenditure Multipliers: The Keynesian Model : Key ConceptsДокумент15 страницExpenditure Multipliers: The Keynesian Model : Key ConceptsTiffany SmithОценок пока нет

- Chapter 12 SolutionДокумент1 страницаChapter 12 SolutionTiffany SmithОценок пока нет

- Organizational Culture and Motivation Impact on Employee Performance at PT Telekomunikasi IndonesiaДокумент33 страницыOrganizational Culture and Motivation Impact on Employee Performance at PT Telekomunikasi IndonesiaTiffany SmithОценок пока нет

- Print 3 RangkapДокумент4 страницыPrint 3 RangkapTiffany SmithОценок пока нет

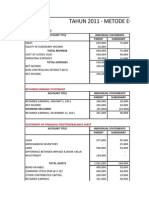

- Tahun 2011 - Metode Equity: Income StementДокумент8 страницTahun 2011 - Metode Equity: Income StementTiffany SmithОценок пока нет

- Business Plan KuiperДокумент51 страницаBusiness Plan KuiperNiña Anrish Joy TadiaОценок пока нет

- CNXX JV 2012 Verkort 5CДокумент77 страницCNXX JV 2012 Verkort 5CgalihОценок пока нет

- Cash budget planning and forecasting</h1Документ3 страницыCash budget planning and forecasting</h1Meghna Phutane100% (3)

- FCF Valuation ModelДокумент8 страницFCF Valuation ModelDemi Tugano BernardinoОценок пока нет

- Assess The Fixed Asset Valuation Method and Allocation of Deprecation ExpenseДокумент30 страницAssess The Fixed Asset Valuation Method and Allocation of Deprecation ExpenseAnonymous Pf4vLs98Pg100% (3)

- "How Well Am I Doing?" Financial Statement AnalysisДокумент61 страница"How Well Am I Doing?" Financial Statement AnalysisSederiku KabaruzaОценок пока нет

- Chap 21 - Leasing (PSAK 73) - E12-12Документ27 страницChap 21 - Leasing (PSAK 73) - E12-12Happy MichaelОценок пока нет

- Module 1 - PGBP Handout PDF - 240124 - 204954Документ42 страницыModule 1 - PGBP Handout PDF - 240124 - 204954jabeanonionОценок пока нет

- ACCT 1A&B: Fundamentals of Accounting BCSV Fundamentals of Accounting Part I The Accounting EquationДокумент11 страницACCT 1A&B: Fundamentals of Accounting BCSV Fundamentals of Accounting Part I The Accounting EquationAyana Mae BaetiongОценок пока нет

- Britannia Industries Financial AnalysisДокумент4 страницыBritannia Industries Financial AnalysisSneha BhartiОценок пока нет

- Quiz Discontinued OperationsДокумент2 страницыQuiz Discontinued OperationsMENDOZA, GLENDA S.Оценок пока нет

- Liability FinalДокумент26 страницLiability FinalJomarie UyОценок пока нет

- ICMA Fall 2013 Exam Business Taxation QuestionsДокумент4 страницыICMA Fall 2013 Exam Business Taxation Questionsmuhzahid786Оценок пока нет

- Arwana Citramulia TBK - 30 - 06 - 2021 - ReleasedДокумент85 страницArwana Citramulia TBK - 30 - 06 - 2021 - ReleasedM Fany AFОценок пока нет

- Ch2Premium LiabilityДокумент20 страницCh2Premium LiabilityCrysta Lee100% (1)

- A. Ra 7918Документ4 страницыA. Ra 7918Karen UmangayОценок пока нет

- Thesis Budget SampleДокумент4 страницыThesis Budget Sampleqpftgehig100% (2)

- Completing THE Accounting Cycle: BKAL 1013 Chapter 4 1Документ51 страницаCompleting THE Accounting Cycle: BKAL 1013 Chapter 4 1Muhammad Franz FirdauzОценок пока нет

- Exam and Question Tutorial Operational Case Study 2019 CIMA Professional QualificationДокумент61 страницаExam and Question Tutorial Operational Case Study 2019 CIMA Professional QualificationMyDustbin2010100% (1)

- BLMGNF Thousand Currents Asset Transfer AgreementДокумент58 страницBLMGNF Thousand Currents Asset Transfer AgreementWashington ExaminerОценок пока нет

- Management Acctg. Qualitative Characteristics of Financial StatementsДокумент71 страницаManagement Acctg. Qualitative Characteristics of Financial StatementsasiegrainenicoleОценок пока нет

- PARTNERSHIPДокумент84 страницыPARTNERSHIPJohn Rey LabasanОценок пока нет

- MA Project 2 - McDonaldsДокумент11 страницMA Project 2 - McDonaldsRafaelKwongОценок пока нет

- Financial Statement Analysis 11th Edition Subramanyam Solutions Manual DownloadДокумент60 страницFinancial Statement Analysis 11th Edition Subramanyam Solutions Manual DownloadDavid Williams100% (21)

- Internship ReportДокумент47 страницInternship ReportDeepaОценок пока нет

- CH 23Документ92 страницыCH 23Erin Heizyk100% (1)