Вам также может понравиться

- The Complete Idiot'SGuide To NumerologyДокумент399 страницThe Complete Idiot'SGuide To NumerologySagui Cohen97% (30)

- Chapter 3 MethodologyДокумент8 страницChapter 3 MethodologyIan Lee93% (168)

- How To Be Happy All The Time - NLP AnchorsДокумент9 страницHow To Be Happy All The Time - NLP Anchorsmramakrishna919Оценок пока нет

- Developing A Mechanical Trading SystemДокумент4 страницыDeveloping A Mechanical Trading SystemKathiravan R100% (1)

- Thesis and Dissertation Paper SamplesДокумент9 страницThesis and Dissertation Paper SamplesMohammed Abdul HaiОценок пока нет

- Chapter 3 FINALДокумент7 страницChapter 3 FINALKeziaОценок пока нет

- Foam ControlДокумент28 страницFoam ControlJoselu Ordoñez Ramos100% (1)

- IDAS Demonstration Setup Guide F3100D-F5120D PDFДокумент146 страницIDAS Demonstration Setup Guide F3100D-F5120D PDFTopcom Toki-Voki100% (2)

- Factors Influencing Online Shopping in IndiaДокумент27 страницFactors Influencing Online Shopping in Indiarishitkhakhar50% (2)

- 501ppt Strategy For Merger and AcquisitionДокумент31 страница501ppt Strategy For Merger and AcquisitionJitender ThakurОценок пока нет

- NYSE History and OverviewДокумент7 страницNYSE History and OverviewJitender Thakur50% (2)

- Challenges of Social Shaming on Self-EsteemДокумент6 страницChallenges of Social Shaming on Self-EsteemA PieceОценок пока нет

- Introduction To Pharmaceutical Dosage FormДокумент27 страницIntroduction To Pharmaceutical Dosage FormEshaal KhanОценок пока нет

- A Comparative GrammarДокумент503 страницыA Comparative GrammarXweuis Hekuos KweОценок пока нет

- Participatory Action Research for Evidence-driven Community DevelopmentОт EverandParticipatory Action Research for Evidence-driven Community DevelopmentОценок пока нет

- Gafti AP Apeo SopДокумент8 страницGafti AP Apeo SopManoj ChaudhariОценок пока нет

- Research MethodologyДокумент6 страницResearch Methodologyshrikrushna javanjal100% (1)

- Research Design SERVQUAL Model ICICI BankДокумент6 страницResearch Design SERVQUAL Model ICICI BankPULKIT KAURA 2127621100% (1)

- Chapter IIIДокумент4 страницыChapter IIIDilip MargamОценок пока нет

- Research MethodologyДокумент4 страницыResearch MethodologyArsl331Оценок пока нет

- Finding Answers To The Research Questions (Quantitaive)Документ6 страницFinding Answers To The Research Questions (Quantitaive)Ella MooreОценок пока нет

- Script Sa Background of The StudyДокумент11 страницScript Sa Background of The StudyEdward AroncianoОценок пока нет

- Chapter 3, 4 5 CombinedДокумент46 страницChapter 3, 4 5 Combinedimran5705074Оценок пока нет

- Chapter ThreeДокумент6 страницChapter Threemakda mulugetaОценок пока нет

- Shalbin MiddleДокумент62 страницыShalbin MiddleShalbin ShajiОценок пока нет

- Trends of Retail Marketing in BangladeshДокумент7 страницTrends of Retail Marketing in BangladeshMehedul Islam SabujОценок пока нет

- ProjectДокумент33 страницыProjectnizamnichu369Оценок пока нет

- Title of ProjectДокумент6 страницTitle of ProjectstemrawОценок пока нет

- Mba Thesis Pptabenet MelkamuДокумент16 страницMba Thesis Pptabenet MelkamuAbenetОценок пока нет

- A Study of Brand Preference of Mobile PhonesДокумент4 страницыA Study of Brand Preference of Mobile PhonesKeerti VasaОценок пока нет

- Man Sci CompreДокумент9 страницMan Sci CompreJessa Mae CacОценок пока нет

- Chapter - V: Research Methodology For The Present StudyДокумент15 страницChapter - V: Research Methodology For The Present StudymoinltrОценок пока нет

- 0948-BH-BAF-19 Muhammad Ali Haider Financial Econometrics ProjectДокумент14 страниц0948-BH-BAF-19 Muhammad Ali Haider Financial Econometrics ProjectMR AОценок пока нет

- Method For Ranking Online ReviewsДокумент50 страницMethod For Ranking Online Reviewskavya J.CОценок пока нет

- Customer Services in ICICI&SBI-SynopsisДокумент4 страницыCustomer Services in ICICI&SBI-SynopsisNageshwar SinghОценок пока нет

- Quantitative ExamДокумент33 страницыQuantitative ExamRafael BerteОценок пока нет

- Meher NegerДокумент10 страницMeher NegerAl Mamun AhmedОценок пока нет

- CASAДокумент76 страницCASARajesh Thangavel100% (1)

- RMДокумент38 страницRMDDZОценок пока нет

- Customer Satisfaction Towards Financial Products and Services of HDFC BankДокумент9 страницCustomer Satisfaction Towards Financial Products and Services of HDFC BankUtsav JaiswalОценок пока нет

- Suggestions & ConclusionДокумент29 страницSuggestions & ConclusionMeenu RaniОценок пока нет

- Fahad Ashraf SynopsisДокумент8 страницFahad Ashraf SynopsisNageshwar SinghОценок пока нет

- SynopsisДокумент2 страницыSynopsisDileep Kumar100% (1)

- Chapter-4 (Research Methodology)Документ48 страницChapter-4 (Research Methodology)ankit161019893980Оценок пока нет

- Part Chapter Thrree FourДокумент26 страницPart Chapter Thrree FourDaris KitchОценок пока нет

- Quantitative ResearchДокумент15 страницQuantitative ResearchTop MusicОценок пока нет

- Group1 SectionC MM Report PDFДокумент10 страницGroup1 SectionC MM Report PDFKunal KumarОценок пока нет

- Morales 2019Документ6 страницMorales 2019signif newsОценок пока нет

- 2 Consumer Behavior Towards Online Shopping PDFДокумент27 страниц2 Consumer Behavior Towards Online Shopping PDFysantoshОценок пока нет

- Research Methodology - Sem 4Документ4 страницыResearch Methodology - Sem 4payablesОценок пока нет

- Chapter Iii: Research Methodology: Population of StudyДокумент5 страницChapter Iii: Research Methodology: Population of Studysajid bhattiОценок пока нет

- Market Study MilmaДокумент8 страницMarket Study MilmaAnush PrasannanОценок пока нет

- An Introduction To Quantitative Research 1Документ2 страницыAn Introduction To Quantitative Research 1AnamОценок пока нет

- MPA-II Assignment Reflections On The Methodology (Ies) Adopted in Case Study 1Документ4 страницыMPA-II Assignment Reflections On The Methodology (Ies) Adopted in Case Study 1Vungrhonthung PattonОценок пока нет

- 09 - Chapter 3 PDFДокумент9 страниц09 - Chapter 3 PDFRomelyn BeranОценок пока нет

- Explain E-Commerce .: 1. Scope of The StudyДокумент2 страницыExplain E-Commerce .: 1. Scope of The Studyshiv pandeyОценок пока нет

- Chapter 3Документ0 страницChapter 3Jermain HolmesОценок пока нет

- Servicequalityof Canara BankДокумент49 страницServicequalityof Canara BankRichard Lawrence50% (4)

- Operationalization - I Session II Research DesignДокумент38 страницOperationalization - I Session II Research DesignSatyaranjan SahuОценок пока нет

- Research Methodology for Bank PerformanceДокумент34 страницыResearch Methodology for Bank PerformanceSatya KumarОценок пока нет

- shree 2Документ6 страницshree 2shriabi1109Оценок пока нет

- Chapter 3Документ8 страницChapter 3danilo jr siquigОценок пока нет

- 09 - Chapter 3Документ29 страниц09 - Chapter 3Gopal ReddyОценок пока нет

- Customer Services in ICICI&SBIДокумент14 страницCustomer Services in ICICI&SBINageshwar SinghОценок пока нет

- Comparative AnalysisДокумент9 страницComparative Analysissamantha.tura4Оценок пока нет

- Banking Services IntroductionДокумент52 страницыBanking Services IntroductionJaffar T K KarulaiОценок пока нет

- BRM ProjectДокумент23 страницыBRM Projectrbhatter007Оценок пока нет

- Satisfection On Varun MotorsДокумент58 страницSatisfection On Varun MotorsLokesh Reddy100% (2)

- Chapter#3Документ6 страницChapter#3AMMAR SHAMSHADОценок пока нет

- Monaj ProjectДокумент43 страницыMonaj ProjectNaresh KumarОценок пока нет

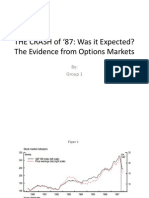

- THE CRASH of 87: Was It Expected? The Evidence From Options MarketsДокумент7 страницTHE CRASH of 87: Was It Expected? The Evidence From Options MarketsJitender ThakurОценок пока нет

- 02 Break Even AnalysisДокумент10 страниц02 Break Even AnalysisJitender ThakurОценок пока нет

- IRDA Journal September Issue 2013Документ108 страницIRDA Journal September Issue 2013Jitender ThakurОценок пока нет

- VCДокумент13 страницVCJitender ThakurОценок пока нет

- SatyamДокумент57 страницSatyamFaisal Malek100% (1)

- Satyam TechmahindraДокумент16 страницSatyam TechmahindraJitender ThakurОценок пока нет

- Q.4 Factors Affecting Capital Market in IndiaДокумент3 страницыQ.4 Factors Affecting Capital Market in IndiaMAHENDRA SHIVAJI DHENAK78% (9)

- Ravina Tech1Документ9 страницRavina Tech1Jitender ThakurОценок пока нет

- SatyamДокумент16 страницSatyamJitender ThakurОценок пока нет

- Indigo Continues Profit Run as Rivals Lose BillionsДокумент8 страницIndigo Continues Profit Run as Rivals Lose BillionsJitender ThakurОценок пока нет

- Muthoot Finance LimitedДокумент13 страницMuthoot Finance LimitedJitender ThakurОценок пока нет

- Final Project 1Документ91 страницаFinal Project 1Jitender ThakurОценок пока нет

- Workshop On Mergers & Acquisitions: Mohit SarafДокумент46 страницWorkshop On Mergers & Acquisitions: Mohit SarafvarunneedsОценок пока нет

- Merger of RIL & RPLДокумент8 страницMerger of RIL & RPLJitender ThakurОценок пока нет

- Activity Rules - Calling A Sub-ActivityДокумент7 страницActivity Rules - Calling A Sub-Activityvineela05Оценок пока нет

- Bhaskar Agarwal CVДокумент1 страницаBhaskar Agarwal CVbhaskaraglОценок пока нет

- Embedded Systems - Fs 2018: Figure 1: Simplified Task States Diagram in FreertosДокумент8 страницEmbedded Systems - Fs 2018: Figure 1: Simplified Task States Diagram in FreertosPhạm Đức HuyОценок пока нет

- HPS100 2016F SyllabusДокумент6 страницHPS100 2016F SyllabusxinОценок пока нет

- Tehreem Mohsin (FA18-BBAH-0003) Eraj Rehan (FA18-BBAH-0004) Mehwish Naeem (FA18-BBAH-0007) Ameer Hamza (FA18-BBAH-0010)Документ4 страницыTehreem Mohsin (FA18-BBAH-0003) Eraj Rehan (FA18-BBAH-0004) Mehwish Naeem (FA18-BBAH-0007) Ameer Hamza (FA18-BBAH-0010)Eraj RehanОценок пока нет

- 14 Applications of Number TheoryДокумент42 страницы14 Applications of Number TheoryKetan DeokarОценок пока нет

- Design & Implementation of Linux Based Network Forensic System Using HoneynetДокумент5 страницDesign & Implementation of Linux Based Network Forensic System Using HoneynetIjarcet JournalОценок пока нет

- Increasing Seismic Safety by CombiningДокумент386 страницIncreasing Seismic Safety by CombiningIvan Hadi SantosoОценок пока нет

- FTT - en 45545 EU Railway Industry 2015 - CompressedДокумент24 страницыFTT - en 45545 EU Railway Industry 2015 - Compresseddody andiОценок пока нет

- Mikhail Murashov: 2110 Applebrook Drive Commerce Township, MI 48382 (386) 569-8665 Personal Website: Mmurashov@adrian - EduДокумент2 страницыMikhail Murashov: 2110 Applebrook Drive Commerce Township, MI 48382 (386) 569-8665 Personal Website: Mmurashov@adrian - Eduapi-242945986Оценок пока нет

- High School 9-12 Reading Curriculum GuideДокумент23 страницыHigh School 9-12 Reading Curriculum GuidemrsfoxОценок пока нет

- Annals of Medicine and Surgery: Bliss J. ChangДокумент2 страницыAnnals of Medicine and Surgery: Bliss J. ChangroromutiaraОценок пока нет

- 6TH Maths Year Plan and Lesson Plan by PrathapДокумент8 страниц6TH Maths Year Plan and Lesson Plan by PrathapPoorvi PatelОценок пока нет

- Status of Technical Education in India - Emerging Issues and ChallengesДокумент11 страницStatus of Technical Education in India - Emerging Issues and ChallengesSreeram MandaОценок пока нет

- An Introduction To Acoustics PDFДокумент296 страницAn Introduction To Acoustics PDFmatteo_1234Оценок пока нет

- 11.servlet WrappersДокумент14 страниц11.servlet WrapperskasimОценок пока нет

- E2788-11 Standard Specification For Use of Expanded Shale, Clay and Slate (ESCS) As A Mineral Component in The Growing Media and The Drainage Layer For Vegetative (Green) Roof SystemsДокумент3 страницыE2788-11 Standard Specification For Use of Expanded Shale, Clay and Slate (ESCS) As A Mineral Component in The Growing Media and The Drainage Layer For Vegetative (Green) Roof SystemsSatya kaliprasad vangaraОценок пока нет

- 11-1203 Syed Hussain HaiderДокумент16 страниц11-1203 Syed Hussain HaiderSalman Nisar BhattiОценок пока нет

- Rafflesian Times Issue 2Документ152 страницыRafflesian Times Issue 2diktat86Оценок пока нет

- Writing Ink Identification: Standard Guide ForДокумент5 страницWriting Ink Identification: Standard Guide ForEric GozzerОценок пока нет

- An Alarming National Trend - False Rape AllegationsДокумент7 страницAn Alarming National Trend - False Rape Allegationsdesbest100% (1)

- TelecomHall - Mapinfo For Telecom - Part 1Документ6 страницTelecomHall - Mapinfo For Telecom - Part 1Drio RioОценок пока нет