Вам также может понравиться

- Engineering and Commercial Functions in BusinessОт EverandEngineering and Commercial Functions in BusinessРейтинг: 5 из 5 звезд5/5 (1)

- H1 FY09 Investor PresentationДокумент34 страницыH1 FY09 Investor PresentationansariakhterОценок пока нет

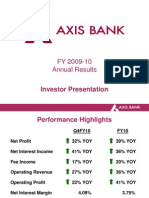

- FY 2009-10 Annual Results: Investor PresentationДокумент34 страницыFY 2009-10 Annual Results: Investor PresentationDujesh KardamОценок пока нет

- BSRM PresentationДокумент4 страницыBSRM PresentationMostafa Noman DeepОценок пока нет

- Depreciation Drilling Rigs Esv2008Документ108 страницDepreciation Drilling Rigs Esv2008corsini999Оценок пока нет

- Nyse Post 2018 PDFДокумент116 страницNyse Post 2018 PDFLM_SОценок пока нет

- 新城发展2022年中期业绩PPT 0830v1Документ39 страниц新城发展2022年中期业绩PPT 0830v1Muska ChiuОценок пока нет

- Can't Say It Enough: Value. Value. ValueДокумент112 страницCan't Say It Enough: Value. Value. Valuebillroberts981Оценок пока нет

- Financial Ratio AnalysisДокумент17 страницFinancial Ratio Analysissarmad_bakhtОценок пока нет

- Working Capital ManagementДокумент19 страницWorking Capital ManagementSandeep KumarОценок пока нет

- Annual ReportДокумент156 страницAnnual ReportTan Chee LeongОценок пока нет

- Hyundai Construction Equipment (IR 4Q20)Документ17 страницHyundai Construction Equipment (IR 4Q20)girish_patkiОценок пока нет

- Bbby 4Q2014Документ3 страницыBbby 4Q2014RahulBakshiОценок пока нет

- Purchases / Average Payables Revenue / Average Total AssetsДокумент7 страницPurchases / Average Payables Revenue / Average Total AssetstannuОценок пока нет

- Solution Manual For Business Analysis and Valuation Ifrs EditionДокумент10 страницSolution Manual For Business Analysis and Valuation Ifrs EditionRobertMitchellmgea100% (40)

- Case 1 MarriottДокумент14 страницCase 1 Marriotthimanshu sagar100% (1)

- Ten Year ReviewДокумент10 страницTen Year Reviewmaruthi631Оценок пока нет

- S9 - XLS069-XLS-ENG MarriottДокумент12 страницS9 - XLS069-XLS-ENG MarriottCarlosОценок пока нет

- FIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadДокумент3 страницыFIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadgОценок пока нет

- Cost of Capital - NikeДокумент6 страницCost of Capital - NikeAnuj SaxenaОценок пока нет

- Cost of Capital - NikeДокумент6 страницCost of Capital - NikeAditi KhaitanОценок пока нет

- Combined Valuing Yahoo in 2013Документ12 страницCombined Valuing Yahoo in 2013Þorgeir DavíðssonОценок пока нет

- 9722 Fujita Kanko Inc CompanyFinancialSummary 20180314222612Документ5 страниц9722 Fujita Kanko Inc CompanyFinancialSummary 20180314222612DamTokyoОценок пока нет

- 2021.1Q Earnings Release: Apirl 26, 2021Документ13 страниц2021.1Q Earnings Release: Apirl 26, 2021Eric ChiangОценок пока нет

- Investor FajarPaper AR 2015 2Документ180 страницInvestor FajarPaper AR 2015 2Shehilda SeptianaОценок пока нет

- Saito Solar ExcelДокумент5 страницSaito Solar ExcelArjun NairОценок пока нет

- Building: Annual 2 0 2 1 / 2 2Документ128 страницBuilding: Annual 2 0 2 1 / 2 2TharushikaОценок пока нет

- Nba Advanced - Happy Hour Co - DCF Model v2Документ10 страницNba Advanced - Happy Hour Co - DCF Model v221BAM045 Sandhiya SОценок пока нет

- Annual Report KAEFДокумент384 страницыAnnual Report KAEFNatasya EdyantoОценок пока нет

- FIN4040 Rosetta Stone Valuation SheetДокумент6 страницFIN4040 Rosetta Stone Valuation SheetMaira Ahmad0% (1)

- BHEL Valuation of CompanyДокумент23 страницыBHEL Valuation of CompanyVishalОценок пока нет

- Management of Monetary Resource of GSK: Course: Faculty: Group NameДокумент27 страницManagement of Monetary Resource of GSK: Course: Faculty: Group Nameborn2growОценок пока нет

- Under ArmourДокумент6 страницUnder Armourzcdbnrdkm4Оценок пока нет

- Chapter 6Документ35 страницChapter 6Tanjila ShipaОценок пока нет

- Viden Io Case Solutions and Notes Airthread Connection Case Solution Calculations 1Документ9 страницViden Io Case Solutions and Notes Airthread Connection Case Solution Calculations 1goyalmuskan412Оценок пока нет

- Glaxosmithkline Consumer Healthcare: Group MembersДокумент19 страницGlaxosmithkline Consumer Healthcare: Group MembersBilal AfzalОценок пока нет

- Ar 2014Документ162 страницыAr 2014kokueiОценок пока нет

- Case 01a Growing Pains SolutionДокумент7 страницCase 01a Growing Pains SolutionUSD 654Оценок пока нет

- Review: Ten Year (Standalone)Документ10 страницReview: Ten Year (Standalone)maruthi631Оценок пока нет

- CL EducateДокумент7 страницCL EducateRicha SinghОценок пока нет

- 17020841116Документ13 страниц17020841116Khushboo RajОценок пока нет

- Discounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No FormulasДокумент2 страницыDiscounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No Formulasrito2005Оценок пока нет

- Business Analysis and Valuation Using Financial Statements Text and Cases Palepu 5th Edition Solutions ManualДокумент19 страницBusiness Analysis and Valuation Using Financial Statements Text and Cases Palepu 5th Edition Solutions ManualStephanieParkerexbf100% (43)

- Pirelli in Figures 2023 9MДокумент11 страницPirelli in Figures 2023 9Mvictorfarima1385Оценок пока нет

- Financial PlanДокумент8 страницFinancial PlanwajeehaОценок пока нет

- 2011 Annual ReportsДокумент96 страниц2011 Annual ReportsCyepi CyemezoОценок пока нет

- Annual Report Telkomsel 2003Документ44 страницыAnnual Report Telkomsel 2003jakabareОценок пока нет

- Data Finansial Gap IncДокумент4 страницыData Finansial Gap IncTohirОценок пока нет

- Shalby Limited BSE 540797 FinancialsДокумент51 страницаShalby Limited BSE 540797 Financialsakumar4uОценок пока нет

- NYSF Walmart Templatev2Документ49 страницNYSF Walmart Templatev2Avinash Ganesan100% (1)

- Shalby Limited BSE 540797 FinancialsДокумент39 страницShalby Limited BSE 540797 Financialsakumar4uОценок пока нет

- Income Statement Template: Strictly ConfidentialДокумент9 страницIncome Statement Template: Strictly ConfidentialAnthony BenavidesОценок пока нет

- SPS Sample ReportsДокумент61 страницаSPS Sample Reportsphong.parkerdistributorОценок пока нет

- Marriott (2) ..Документ13 страницMarriott (2) ..veninsssssОценок пока нет

- Tata Motors Dupont and Altman Z-Score AnalysisДокумент4 страницыTata Motors Dupont and Altman Z-Score AnalysisLAKHAN TRIVEDIОценок пока нет

- 08 AnsДокумент13 страниц08 AnsAnonymous 8ooQmMoNs1Оценок пока нет

- Prospective Analysis 2Документ7 страницProspective Analysis 2MAYANK JAINОценок пока нет

- Bidding For Hertz Leveraged Buyout, Spreadsheet SupplementДокумент12 страницBidding For Hertz Leveraged Buyout, Spreadsheet SupplementAmit AdmuneОценок пока нет

- Atlas HondaДокумент15 страницAtlas HondaQasim AkramОценок пока нет

- ENT300 Module11Документ56 страницENT300 Module11Muhammad AkbarОценок пока нет

- Business Plan For Creative AgencyДокумент27 страницBusiness Plan For Creative AgencySajeed Alam75% (8)

- Financial Reporting in The Mining IndustryДокумент192 страницыFinancial Reporting in The Mining IndustryerlanggaherpОценок пока нет

- Hoyle Advanced Accounting Powerpoint Slides Chapter 3Документ37 страницHoyle Advanced Accounting Powerpoint Slides Chapter 3Sean75% (4)

- Solution To The Case Study - The Norrkoping PlantДокумент3 страницыSolution To The Case Study - The Norrkoping PlantMudasser50% (2)

- Getz Pharma Corporate ProfileДокумент2 страницыGetz Pharma Corporate ProfileghazalidawoodОценок пока нет

- Commodity PDFДокумент85 страницCommodity PDFSuyash Kumar100% (2)

- NBFC & CooperativesДокумент3 страницыNBFC & Cooperativesvarun_pillai92Оценок пока нет

- Oxford University Press - Online Resource Centre - Chapter 05Документ3 страницыOxford University Press - Online Resource Centre - Chapter 05pink1231Оценок пока нет

- Benjamin Graham and The Birth of Value InvestingДокумент85 страницBenjamin Graham and The Birth of Value InvestingTara GorurОценок пока нет

- FinalFA2015 MBA v3 With Detailed SolutionДокумент20 страницFinalFA2015 MBA v3 With Detailed Solutionarisht jainxОценок пока нет

- Exide Industries LTDДокумент8 страницExide Industries LTDVikram FernandezОценок пока нет

- Capital Account Convertibility: Issues and ConcernsДокумент19 страницCapital Account Convertibility: Issues and Concernsme22anshuОценок пока нет

- Financial AdministrationДокумент15 страницFinancial Administrationshivkanth28Оценок пока нет

- House Hearing, 111TH Congress - Capital Markets Regulatory Reform: Strengthening Investor Protection, Enhancing Oversight of Private Pools of Capital, and Creating A National Insurance OfficeДокумент325 страницHouse Hearing, 111TH Congress - Capital Markets Regulatory Reform: Strengthening Investor Protection, Enhancing Oversight of Private Pools of Capital, and Creating A National Insurance OfficeScribd Government DocsОценок пока нет

- Financial Statement Analysis: K R Subramanyam John J WildДокумент40 страницFinancial Statement Analysis: K R Subramanyam John J WildMARIA ANGELINA WIBAWA (00000020978)Оценок пока нет

- Conceptual Framework WITH ANSWERSДокумент25 страницConceptual Framework WITH ANSWERSDymphna Ann CalumpianoОценок пока нет

- MS Azure CaseДокумент8 страницMS Azure CaseSidharth RainaОценок пока нет

- ACCT 411-Applied Financial Analysis-Arslan Shahid Butt PDFДокумент7 страницACCT 411-Applied Financial Analysis-Arslan Shahid Butt PDFAbdul Basit JavedОценок пока нет

- Example 2 Find Revenue With One PriceДокумент28 страницExample 2 Find Revenue With One PriceramanОценок пока нет

- Cost of Capital, Optimal Capital Structure, and Leverages 1.0 The Fundamental ConceptДокумент5 страницCost of Capital, Optimal Capital Structure, and Leverages 1.0 The Fundamental ConceptMacy AndradeОценок пока нет

- MC Moelis InitiatingДокумент27 страницMC Moelis InitiatingRCОценок пока нет

- DAAS2 DocxdgsdgsdДокумент4 страницыDAAS2 DocxdgsdgsdemrangiftОценок пока нет

- Fair Value Accounting For FinancialДокумент4 страницыFair Value Accounting For FinancialAashie SkystОценок пока нет

- Certified Credit Union Financial Counselor Training Program: The Vermont StoryДокумент9 страницCertified Credit Union Financial Counselor Training Program: The Vermont StoryREAL SolutionsОценок пока нет

- Billabong Case StudyДокумент13 страницBillabong Case StudyVan Tran0% (1)

- A KariozenДокумент4 страницыA Kariozenjoseyamil77Оценок пока нет

- Coffee Shop Business PlanДокумент14 страницCoffee Shop Business Planmeenuchoudharyoffice100% (1)

- Ugvcl HT Power Connection NormsДокумент15 страницUgvcl HT Power Connection Normsjhakg_169712275Оценок пока нет

- Accounting Theory Chapter 11 - GodfreyДокумент40 страницAccounting Theory Chapter 11 - GodfreyRozanna Amalia100% (1)