Вам также может понравиться

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Bandy How To Build Trading SysДокумент113 страницBandy How To Build Trading SysJack ParrОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Internship Report Adamjee Insurance CoДокумент95 страницInternship Report Adamjee Insurance CoUneeza AliОценок пока нет

- Marketing ManagementДокумент146 страницMarketing ManagementMannu Bhardwaj100% (2)

- Ebook Percuma Tfs Price Action TradingДокумент7 страницEbook Percuma Tfs Price Action TradingMUHAMMAD AL AMIN AZMANОценок пока нет

- DO - 163 - S2015 - DupaДокумент12 страницDO - 163 - S2015 - DupaRay Ramilo100% (1)

- Audit Program Fixed AssetsДокумент6 страницAudit Program Fixed Assetsnico_pia454Оценок пока нет

- Secrets of Successful Forex Gold Trading - Advanced ForexДокумент3 страницыSecrets of Successful Forex Gold Trading - Advanced ForexMudasir MuhdiОценок пока нет

- PDD Accounting For Bad Debts and Writeoffs (BDAR2160)Документ37 страницPDD Accounting For Bad Debts and Writeoffs (BDAR2160)SRDОценок пока нет

- Huerta Alba Resort V CAДокумент2 страницыHuerta Alba Resort V CAsinisteredgirl100% (1)

- 10 - Consolidations - Changes in Ownership InterestsДокумент42 страницы10 - Consolidations - Changes in Ownership InterestsLukas PrawiraОценок пока нет

- The Nature of The Social Work TaskДокумент11 страницThe Nature of The Social Work Taskronaldzamora100% (1)

- Lenses: Model Description Recommended Retail PriceДокумент12 страницLenses: Model Description Recommended Retail PriceronaldzamoraОценок пока нет

- BasicElements of Financial Management SystemДокумент5 страницBasicElements of Financial Management SystemronaldzamoraОценок пока нет

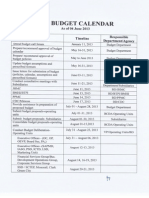

- 2014 - Budget CalendarДокумент3 страницы2014 - Budget CalendarronaldzamoraОценок пока нет

- NBC548 PDFДокумент9 страницNBC548 PDFegabadОценок пока нет

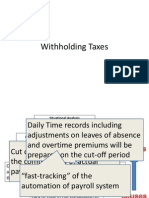

- Withholding TaxesДокумент3 страницыWithholding TaxesronaldzamoraОценок пока нет

- Presidential Decree No. 807, Civil Service Decree of The PhilippinesДокумент36 страницPresidential Decree No. 807, Civil Service Decree of The PhilippinesronaldzamoraОценок пока нет

- Test 01 Chapters 2 & 3 September 25Документ8 страницTest 01 Chapters 2 & 3 September 25barbara tamminenОценок пока нет

- BPPL Holdings PLCДокумент15 страницBPPL Holdings PLCkasun witharanaОценок пока нет

- Module 4 PDFДокумент19 страницModule 4 PDFRAJASAHEB DUTTAОценок пока нет

- FRBM ActДокумент3 страницыFRBM ActDHWANI DEDHIAОценок пока нет

- Basics of Engineering Economy, 1e: CHAPTER 12 Solutions ManualДокумент15 страницBasics of Engineering Economy, 1e: CHAPTER 12 Solutions Manualttufan1Оценок пока нет

- SJCBA Prospectus 2010-12-04nov09Документ17 страницSJCBA Prospectus 2010-12-04nov09tyrone21Оценок пока нет

- Polaroid Corporation Case Solution Final PDFДокумент8 страницPolaroid Corporation Case Solution Final PDFShirazeОценок пока нет

- Format For Stock Statement in Case of Manufacturing/ProcessingДокумент36 страницFormat For Stock Statement in Case of Manufacturing/ProcessingAjoydeepОценок пока нет

- Chapter 1. Introduction To Cost and ManagementДокумент49 страницChapter 1. Introduction To Cost and ManagementHARYATI SETYORINI100% (1)

- Letter-SB-Request For Special Session-11 October 2023Документ5 страницLetter-SB-Request For Special Session-11 October 2023cj.pulga.palОценок пока нет

- CSD PlanДокумент12 страницCSD PlanNargis FatimaОценок пока нет

- Economic Analysis and Decision Making: SayedmohammadrezamirforughyДокумент2 страницыEconomic Analysis and Decision Making: SayedmohammadrezamirforughyMaiwand KhanОценок пока нет

- Final-Fall-2009 Mock SolutionДокумент16 страницFinal-Fall-2009 Mock SolutionmehdiОценок пока нет

- Account Statement: Date Value Date Description Cheque Deposit Withdrawal BalanceДокумент2 страницыAccount Statement: Date Value Date Description Cheque Deposit Withdrawal BalancesadhanaОценок пока нет

- EquityДокумент126 страницEquityChristopherОценок пока нет

- Trader's Journal Cover - Brandon Wendell August 2010Документ6 страницTrader's Journal Cover - Brandon Wendell August 2010mleefxОценок пока нет

- Insurance Types Importance Objective Alternative Takaful Feature of Takaful, Re Insurance, Takaful WorldwideДокумент11 страницInsurance Types Importance Objective Alternative Takaful Feature of Takaful, Re Insurance, Takaful WorldwideMD. ANWAR UL HAQUEОценок пока нет

- Euro Currency Market (Unit 1)Документ27 страницEuro Currency Market (Unit 1)Manoj Bansiwal100% (1)

- WineCare Storage LLC: DECLARATION OF DEREK L. LIMBOCKERДокумент25 страницWineCare Storage LLC: DECLARATION OF DEREK L. LIMBOCKERBrad DempseyОценок пока нет

- Job Vacancy - PT Hale InternationalДокумент3 страницыJob Vacancy - PT Hale InternationalFebrihybridОценок пока нет

- Corporate Income Tax ActДокумент59 страницCorporate Income Tax ActMateusz DłużniewskiОценок пока нет