Вам также может понравиться

- Future HedgingДокумент29 страницFuture HedgingChRehanAliОценок пока нет

- Topic 1 Intro To DerivativesДокумент66 страницTopic 1 Intro To DerivativesVikram JaiswalОценок пока нет

- Making Money with Option Strategies: Powerful Hedging Ideas for the Serious Investor to Reduce Portfolio RisksОт EverandMaking Money with Option Strategies: Powerful Hedging Ideas for the Serious Investor to Reduce Portfolio RisksОценок пока нет

- Two Marks Question: 1. What Is Hedging?Документ6 страницTwo Marks Question: 1. What Is Hedging?akshataОценок пока нет

- Finman 10 DerivativesДокумент5 страницFinman 10 DerivativesStephanie Dulay SierraОценок пока нет

- DerivativesДокумент12 страницDerivativesapi-555390406Оценок пока нет

- Test Bank Fin Man 3Документ2 страницыTest Bank Fin Man 3Phillip RamosОценок пока нет

- Qus Der Mid 1Документ4 страницыQus Der Mid 1Santosh KumarОценок пока нет

- Topic 1 Intro To DerivativesДокумент29 страницTopic 1 Intro To DerivativesRaheel SiddiquiОценок пока нет

- Pluck Eesj A16Документ10 страницPluck Eesj A16008Akshat BedekarОценок пока нет

- Financial Derivatives Lessons From The Subprime CrisisДокумент13 страницFinancial Derivatives Lessons From The Subprime CrisisTytyt TyyОценок пока нет

- HedgingДокумент2 страницыHedgingSonam GuptaОценок пока нет

- Chap 005Документ18 страницChap 005van tinh khucОценок пока нет

- Managing Foreign Exchange Risk: International Service CentreДокумент8 страницManaging Foreign Exchange Risk: International Service CentrenadeenaОценок пока нет

- Literature Review Currency HedgingДокумент8 страницLiterature Review Currency Hedgingfvf8gc78100% (1)

- Chapter 23 NotesДокумент16 страницChapter 23 Notesakeila3Оценок пока нет

- Ims3310 Group 10 Dealing With Transaction RiskДокумент8 страницIms3310 Group 10 Dealing With Transaction Riskapi-250771392Оценок пока нет

- A Primer On Hedge FundsДокумент10 страницA Primer On Hedge FundsOladipupo Mayowa PaulОценок пока нет

- 1 Compare & Contrast Objective Risk and Subjective Risk?: Insurance CompanyДокумент6 страниц1 Compare & Contrast Objective Risk and Subjective Risk?: Insurance Companytayachew mollaОценок пока нет

- 2019-Ag-1826 Zain Ul AbidinДокумент9 страниц2019-Ag-1826 Zain Ul AbidinMian ZainОценок пока нет

- Orca Share Media1517752297941Документ179 страницOrca Share Media1517752297941Jewel Mae MercadoОценок пока нет

- Arbitrage WorkДокумент11 страницArbitrage WorkAhmed YusufОценок пока нет

- Homework Answers 1Документ3 страницыHomework Answers 1Vel NefertariОценок пока нет

- Option Chain Part-6Документ5 страницOption Chain Part-6ramyatan SinghОценок пока нет

- The Management of Foreign Exchange RiskДокумент98 страницThe Management of Foreign Exchange RisknandiniОценок пока нет

- Derivatives Risk Mit.Документ56 страницDerivatives Risk Mit.Prashant PhanseОценок пока нет

- What Are Your Hedging Options?: Executive SummaryДокумент3 страницыWhat Are Your Hedging Options?: Executive SummarytrevinooscarОценок пока нет

- Derivatives and Risk Management: Answers To Beginning-Of-Chapter QuestionsДокумент13 страницDerivatives and Risk Management: Answers To Beginning-Of-Chapter QuestionsRiri FahraniОценок пока нет

- Foundations of International Strategy (Tilburg University) Foundations of International Strategy (Tilburg University)Документ8 страницFoundations of International Strategy (Tilburg University) Foundations of International Strategy (Tilburg University)Еmil KostovОценок пока нет

- Current-Transcriber-Test (2) - Otter - AiДокумент1 страницаCurrent-Transcriber-Test (2) - Otter - Aiquaqu HenryОценок пока нет

- Arbitrage Pricing TheoryДокумент21 страницаArbitrage Pricing TheoryMahesh BhorОценок пока нет

- The Credit Hedging Agency Model Vs Credit Default SwapsДокумент3 страницыThe Credit Hedging Agency Model Vs Credit Default SwapsJasvinder JosenОценок пока нет

- Chap001 RevisedДокумент43 страницыChap001 Revisedp6yq4n9ykjОценок пока нет

- Jim Leitner - Global Macro WizardДокумент6 страницJim Leitner - Global Macro Wizardmoolya_rajeshОценок пока нет

- Pricing Convertible BondДокумент31 страницаPricing Convertible BondMaxОценок пока нет

- Quantitative Modelling: The Quantitative Modelling Group Is Responsible For Researching, DevelopingДокумент18 страницQuantitative Modelling: The Quantitative Modelling Group Is Responsible For Researching, DevelopingDeepak AhujaОценок пока нет

- Dvanced Orporate Inance: Derivatives and Hedging RiskДокумент29 страницDvanced Orporate Inance: Derivatives and Hedging RiskMohamed A FarahОценок пока нет

- Should You Buy or Sell Tail Risk Hedges? A Filtered Bootstrap ApproachДокумент33 страницыShould You Buy or Sell Tail Risk Hedges? A Filtered Bootstrap ApproachRahul SheorainОценок пока нет

- Everything Is A DCF ModelДокумент13 страницEverything Is A DCF ModelSajjad HossainОценок пока нет

- What Are DerivativesДокумент9 страницWhat Are DerivativesKashyap NirmalОценок пока нет

- Currency Options: Trading & SpeculationДокумент11 страницCurrency Options: Trading & SpeculationNelly NanevaОценок пока нет

- Managing Interest Rate RiskДокумент4 страницыManaging Interest Rate RiskNyeko FrancisОценок пока нет

- Hedging PDFДокумент6 страницHedging PDFIraiven ShanmugamОценок пока нет

- Credit Default Swaps and The Credit Crisis: René M. StulzДокумент21 страницаCredit Default Swaps and The Credit Crisis: René M. StulzRenjie XuОценок пока нет

- Research Paper For Credit CrisisДокумент31 страницаResearch Paper For Credit CrisisShabana KhanОценок пока нет

- SEC Short SellingДокумент10 страницSEC Short SellingNatasha LaoОценок пока нет

- Seth Klarman On The Painful Decision To Hold CashДокумент2 страницыSeth Klarman On The Painful Decision To Hold CashIgor Chalhub100% (5)

- Dr. Jayaraman BalakrishnanДокумент19 страницDr. Jayaraman BalakrishnanAhmed MunawarОценок пока нет

- Pindyck Solutions Chapter 5Документ13 страницPindyck Solutions Chapter 5Ashok Patsamatla100% (1)

- How Companies Use Derivatives For Hedging & Risk ManagementДокумент17 страницHow Companies Use Derivatives For Hedging & Risk ManagementBinitha B NairОценок пока нет

- Financial Risk Management AssignmentДокумент8 страницFinancial Risk Management AssignmentM-Faheem AslamОценок пока нет

- Report On: Bangladesh Institute of Bank ManagementДокумент26 страницReport On: Bangladesh Institute of Bank ManagementriasatОценок пока нет

- Credit Default Swaps and GFC-C2D2Документ5 страницCredit Default Swaps and GFC-C2D2michnhiОценок пока нет

- Arbitrage ProjectДокумент96 страницArbitrage Projectyogesh_bhargavОценок пока нет

- Derivatives and RMДокумент35 страницDerivatives and RMMichael WardОценок пока нет

- Sense and Nonsense in Modern Corporate FinanceДокумент139 страницSense and Nonsense in Modern Corporate FinancerameshvarmagОценок пока нет

- How To Win 97% of Your Options Trades Ebook PDFДокумент24 страницыHow To Win 97% of Your Options Trades Ebook PDFAdam Perez100% (6)

- Outline of FinanceДокумент255 страницOutline of FinanceKal_CОценок пока нет

- Butterfly EconomicsДокумент5 страницButterfly EconomicsLameuneОценок пока нет

- Brief Therapy - A Problem Solving Model of ChangeДокумент4 страницыBrief Therapy - A Problem Solving Model of ChangeLameuneОценок пока нет

- Dispersion TradesДокумент41 страницаDispersion TradesLameune100% (1)

- Commodity Hybrids Trading: James Groves, Barclays CapitalДокумент21 страницаCommodity Hybrids Trading: James Groves, Barclays CapitalLameuneОценок пока нет

- Network of Options For International Coal & Freight BusinessesДокумент20 страницNetwork of Options For International Coal & Freight BusinessesLameuneОценок пока нет

- A Course On Asymptotic Methods, Choice of Model in Regression and CausalityДокумент1 страницаA Course On Asymptotic Methods, Choice of Model in Regression and CausalityLameuneОценок пока нет

- Eyde LandДокумент54 страницыEyde LandLameuneОценок пока нет

- Jacob BeharallДокумент19 страницJacob BeharallLameuneОценок пока нет

- Tristam ScottДокумент24 страницыTristam ScottLameuneОценок пока нет

- Pricing Storable Commodities and Associated Derivatives: Dorje C. BrodyДокумент32 страницыPricing Storable Commodities and Associated Derivatives: Dorje C. BrodyLameuneОценок пока нет

- Valuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingДокумент25 страницValuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingLameuneОценок пока нет

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalДокумент44 страницыReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneОценок пока нет

- Andrea RoncoroniДокумент27 страницAndrea RoncoroniLameuneОценок пока нет

- Marcel ProkopczukДокумент28 страницMarcel ProkopczukLameuneОценок пока нет

- Prmia 20111103 NyholmДокумент24 страницыPrmia 20111103 NyholmLameuneОценок пока нет

- Emmanuel GincbergДокумент37 страницEmmanuel GincbergLameuneОценок пока нет

- Tristam ScottДокумент24 страницыTristam ScottLameuneОценок пока нет

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalДокумент44 страницыReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneОценок пока нет

- Day3 Session 2APaulДокумент11 страницDay3 Session 2APaulLameuneОценок пока нет

- Day3 Session2B StoneДокумент11 страницDay3 Session2B StoneLameuneОценок пока нет

- Day1 Session3 ColeДокумент36 страницDay1 Session3 ColeLameuneОценок пока нет

- Day3 Session 1BSternberg PresentationforWebДокумент11 страницDay3 Session 1BSternberg PresentationforWebLameuneОценок пока нет

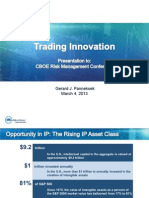

- Gerard J. Pannekoek March 4, 2013Документ12 страницGerard J. Pannekoek March 4, 2013LameuneОценок пока нет

- Prediction CompanyДокумент16 страницPrediction CompanylowtarhkОценок пока нет

- Anton R. Valukas, Examiners Report - in Re Lehman Brothers Inc., Et Al., (2010-03-10) - Volume 8 - Appendix 8 - 22Документ487 страницAnton R. Valukas, Examiners Report - in Re Lehman Brothers Inc., Et Al., (2010-03-10) - Volume 8 - Appendix 8 - 22Meliora CogitoОценок пока нет

- Work Experience Watiga & Co. (S) Pte LTD: IgnatiusДокумент3 страницыWork Experience Watiga & Co. (S) Pte LTD: IgnatiusankiosaОценок пока нет

- Mergers & Acquisitions: Merger Evaluation: RIL & Network 18Документ13 страницMergers & Acquisitions: Merger Evaluation: RIL & Network 18DilipSamantaОценок пока нет

- Guided Notes - Roaring 20s and Great DepressionДокумент3 страницыGuided Notes - Roaring 20s and Great DepressionBradley GriffinОценок пока нет

- Digital Assignment 2Документ7 страницDigital Assignment 2Prithish PreeОценок пока нет

- Technical Analysis: Presented by Anita Singhal 1Документ41 страницаTechnical Analysis: Presented by Anita Singhal 1anita singhalОценок пока нет

- Corporation CodeДокумент28 страницCorporation Codejanine nenariaОценок пока нет

- Nism Investment Adviser Level2 Study Notes PDFДокумент20 страницNism Investment Adviser Level2 Study Notes PDFAkash VaidyaОценок пока нет

- 8905 Corporate Liquidation Answers PDFДокумент14 страниц8905 Corporate Liquidation Answers PDFYADAO, EloisaОценок пока нет

- Important Mafa SuggestionДокумент60 страницImportant Mafa Suggestioncyrex33Оценок пока нет

- TDTLДокумент4 страницыTDTLGeorgeОценок пока нет

- IFMP Mutual Fund Distributors Certification (Study and Reference Guide) PDFДокумент165 страницIFMP Mutual Fund Distributors Certification (Study and Reference Guide) PDFPunjabi Larka100% (1)

- FovewivusДокумент2 страницыFovewivusSREENIVASA MURTHY RОценок пока нет

- Nora JV Sakari AnalysisДокумент3 страницыNora JV Sakari AnalysisIrwan PriambodoОценок пока нет

- FINA3324 MSE Potential QuestionsДокумент10 страницFINA3324 MSE Potential QuestionsrcrmОценок пока нет

- Anomalies - Behavioral FinanceДокумент19 страницAnomalies - Behavioral Financeabhishekbehal5012Оценок пока нет

- Gulf Business - December 2010Документ130 страницGulf Business - December 2010motivatepublishingОценок пока нет

- Aas 12 Responsibility of Joint AuditorsДокумент3 страницыAas 12 Responsibility of Joint AuditorsRishabh GuptaОценок пока нет

- Qualifying Exam Review Qs Final Answers2Документ32 страницыQualifying Exam Review Qs Final Answers2JD DLОценок пока нет

- Contoh Soal Pelaporan KorporatДокумент4 страницыContoh Soal Pelaporan Korporatirma cahyani kawi0% (1)

- Starbuck PPT by Pershing SquareДокумент44 страницыStarbuck PPT by Pershing SquareJainam VoraОценок пока нет

- Original Research Paper: Prof. Parameshwar H.S. Manish Soni Utkarsh Pandey Jayant Singh Bhadoria Pranjul BajpayeeДокумент4 страницыOriginal Research Paper: Prof. Parameshwar H.S. Manish Soni Utkarsh Pandey Jayant Singh Bhadoria Pranjul BajpayeeSourav PaulОценок пока нет

- Final Tax PDFДокумент3 страницыFinal Tax PDFGianJoshuaDayrit0% (1)

- Financial Management - Question Paper Review - 5 & 10 Marks (Problems)Документ2 страницыFinancial Management - Question Paper Review - 5 & 10 Marks (Problems)jeganrajrajОценок пока нет

- Webster Smart ShopperДокумент32 страницыWebster Smart ShopperPete SearsОценок пока нет

- AlphaДокумент18 страницAlphaOrganic NutsОценок пока нет

- DepriciationДокумент3 страницыDepriciationIram RiazОценок пока нет

- CH 12Документ3 страницыCH 12vivien0% (1)

- Cost of Capital Module 7 (Class 27)Документ16 страницCost of Capital Module 7 (Class 27)Vineet AgarwalОценок пока нет