Вам также может понравиться

- Control: The Management Control Environment: Changes From The Eleventh EditionДокумент22 страницыControl: The Management Control Environment: Changes From The Eleventh EditionRobin Shephard Hogue100% (1)

- Chap 006Документ15 страницChap 006Neetu RajaramanОценок пока нет

- AHM Chapter 3 Exercises CKvxWXG1tmДокумент2 страницыAHM Chapter 3 Exercises CKvxWXG1tmASHUTOSH BISWALОценок пока нет

- Project ManagementДокумент10 страницProject ManagementcleousОценок пока нет

- Case Background: - Mrs. Santha - Owner Small Assembly Shop - Production Line AДокумент12 страницCase Background: - Mrs. Santha - Owner Small Assembly Shop - Production Line AAbhishek KumarОценок пока нет

- Case Study Beta Management Company: Raman Dhiman Indian Institute of Management (Iim), ShillongДокумент8 страницCase Study Beta Management Company: Raman Dhiman Indian Institute of Management (Iim), ShillongFabián Fuentes100% (1)

- Chapter 7 (Case) : Joan HoltzДокумент2 страницыChapter 7 (Case) : Joan Holtzjenice joy100% (1)

- Comparing Depreciation at Delta Air Lines and Singapore AirlinesДокумент110 страницComparing Depreciation at Delta Air Lines and Singapore AirlinesSiratullah ShahОценок пока нет

- McPhee Distillers Statements v03 CPДокумент13 страницMcPhee Distillers Statements v03 CPcmag10Оценок пока нет

- Prestige Telephone Company SlidesДокумент13 страницPrestige Telephone Company SlidesHarsh MaheshwariОценок пока нет

- Balakrishnan MGRL Solutions Ch14Документ36 страницBalakrishnan MGRL Solutions Ch14Aditya Krishna100% (1)

- Chap 003Документ19 страницChap 003jujuОценок пока нет

- BBC's Proposal to Manufacture Bicycles for Hi-ValuДокумент19 страницBBC's Proposal to Manufacture Bicycles for Hi-ValuMannu83Оценок пока нет

- PHT and KooistraДокумент4 страницыPHT and KooistraNilesh PrajapatiОценок пока нет

- GRAND RIVER UNIVERSITY ACTIVITY BASED COSTING CASE ANALYSISДокумент6 страницGRAND RIVER UNIVERSITY ACTIVITY BASED COSTING CASE ANALYSISfisa kiahsОценок пока нет

- Darlana FurnitureДокумент3 страницыDarlana FurnitureWidyawan Widarto 闘志Оценок пока нет

- Management 122 Course XXXXZAXReader - Rev J - SolutionsДокумент43 страницыManagement 122 Course XXXXZAXReader - Rev J - SolutionsWOw WongОценок пока нет

- The Quaker Oats Company and Subsidiaries Consolidated Statements of IncomeДокумент3 страницыThe Quaker Oats Company and Subsidiaries Consolidated Statements of IncomeNaseer AhmedОценок пока нет

- ISM Case Analysis (Cisco Systems) : Group 13 Section - AДокумент6 страницISM Case Analysis (Cisco Systems) : Group 13 Section - AManish Kumar BansalОценок пока нет

- SCM - Managing Uncertainty in DemandДокумент27 страницSCM - Managing Uncertainty in DemandHari Madhavan Krishna KumarОценок пока нет

- A Letter From PrisonДокумент2 страницыA Letter From PrisonLejla ArapcicОценок пока нет

- Chapter 26Документ32 страницыChapter 26karlosgwapo3Оценок пока нет

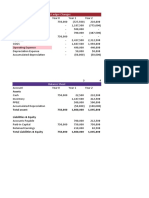

- Precision WorldwideДокумент9 страницPrecision WorldwidePedro José ZapataОценок пока нет

- Chapter 7Документ24 страницыChapter 7Palos DoseОценок пока нет

- Finance Minicase 1 Sunset BoardsДокумент12 страницFinance Minicase 1 Sunset Boardsapi-31397810480% (5)

- Prashanti Technologies: A Case Analysis On in Partial Fulfilment of Advanced Course in Labour Laws Submitted byДокумент5 страницPrashanti Technologies: A Case Analysis On in Partial Fulfilment of Advanced Course in Labour Laws Submitted byANUSHKA PGPHRM 2020 BatchОценок пока нет

- Prestige Telephone CompanyДокумент2 страницыPrestige Telephone CompanyArbaz AbbasОценок пока нет

- Pharmacy Service Improvement at CVSДокумент18 страницPharmacy Service Improvement at CVSnatya lakshitaОценок пока нет

- 18-Conway IndustriesДокумент5 страниц18-Conway IndustriesKiranJumanОценок пока нет

- Management Sheet 1 (Decision Making Assignment)Документ6 страницManagement Sheet 1 (Decision Making Assignment)Dalia EhabОценок пока нет

- Apple Watch (A) - The Launch Case Study Solution: Marginal EconomicsДокумент4 страницыApple Watch (A) - The Launch Case Study Solution: Marginal Economicshimani rathore100% (1)

- Dreamworld Amusement Park Case Study: Initial Years of OperationДокумент3 страницыDreamworld Amusement Park Case Study: Initial Years of OperationArnav MittalОценок пока нет

- Session 17 MBA 703 2018 BeforeclassДокумент43 страницыSession 17 MBA 703 2018 BeforeclassGeeta SinghОценок пока нет

- Project Cash Flow ComparisonДокумент6 страницProject Cash Flow Comparisonanhdu7Оценок пока нет

- MANAC II - Morrissey Forgings CaseДокумент8 страницMANAC II - Morrissey Forgings CaseKaran Oberoi100% (1)

- Operations Management Assignment Don't Bother Me I Can't CopeДокумент3 страницыOperations Management Assignment Don't Bother Me I Can't CopeSharan SaarsarОценок пока нет

- Group 7 - Morrissey ForgingsДокумент10 страницGroup 7 - Morrissey ForgingsVishal AgarwalОценок пока нет

- Kentucky Fried Chicken in JapanДокумент3 страницыKentucky Fried Chicken in Japanezeasor arinzeОценок пока нет

- As Sig Ment 2 PrivateДокумент138 страницAs Sig Ment 2 PrivateluisОценок пока нет

- O.M Scoott and Sons Case Study HarvardДокумент6 страницO.M Scoott and Sons Case Study Harvardnicole rodríguezОценок пока нет

- California CreameryДокумент2 страницыCalifornia CreameryHeena GuptaОценок пока нет

- Newell Case StudyДокумент1 страницаNewell Case StudyNaina AgrawalОценок пока нет

- Name: Affan Ahmed Course: ACN 202 ID: 1821868 Section: 07Документ11 страницName: Affan Ahmed Course: ACN 202 ID: 1821868 Section: 07Affan AhmedОценок пока нет

- Revenue and Monetary Assets: Changes From Eleventh EditionДокумент21 страницаRevenue and Monetary Assets: Changes From Eleventh EditionMenahil KОценок пока нет

- Journal Entries for Three Month Business TransactionsДокумент4 страницыJournal Entries for Three Month Business TransactionsVinayak SinglaОценок пока нет

- Marshall Chapter 3 Case StudyДокумент2 страницыMarshall Chapter 3 Case Studyapi-3173686540% (1)

- Naukri Employee Retention CaseДокумент13 страницNaukri Employee Retention CaseBhanu NirwanОценок пока нет

- Decision+Analysis+for+UG 2C+Fall+2014 2C+Course+Outline+2014-08-14Документ9 страницDecision+Analysis+for+UG 2C+Fall+2014 2C+Course+Outline+2014-08-14tuahasiddiqui0% (1)

- Chapter 5Документ3 страницыChapter 5zixuan weiОценок пока нет

- Swati Anand - FRMcaseДокумент5 страницSwati Anand - FRMcaseBhavin MohiteОценок пока нет

- PIA Breakeven Analysis and Financial Performance ReportДокумент3 страницыPIA Breakeven Analysis and Financial Performance ReportsaadsahilОценок пока нет

- Seligram Summary DetailsДокумент6 страницSeligram Summary DetailsSachin MailareОценок пока нет

- Colgate-Palmolive in Mexico (Group 1) : July 2016Документ6 страницColgate-Palmolive in Mexico (Group 1) : July 2016GloryОценок пока нет

- O.M Scott and Sons Case SummaryДокумент2 страницыO.M Scott and Sons Case SummarySUSHMITA SHUBHAMОценок пока нет

- Garanti Payment Systems:: Digital Transformation StrategyДокумент12 страницGaranti Payment Systems:: Digital Transformation StrategySwarnajit SahaОценок пока нет

- Corporate Financial Analysis with Microsoft ExcelОт EverandCorporate Financial Analysis with Microsoft ExcelРейтинг: 5 из 5 звезд5/5 (1)

- It’s Not What You Sell—It’s How You Sell It: Outshine Your Competition & Create Loyal CustomersОт EverandIt’s Not What You Sell—It’s How You Sell It: Outshine Your Competition & Create Loyal CustomersОценок пока нет

- Value Chain Management Capability A Complete Guide - 2020 EditionОт EverandValue Chain Management Capability A Complete Guide - 2020 EditionОценок пока нет

- Additional Aspects of Product Costing Systems: Changes From Eleventh EditionДокумент21 страницаAdditional Aspects of Product Costing Systems: Changes From Eleventh EditionceojiОценок пока нет

- Lieberose Solar ParkДокумент23 страницыLieberose Solar ParkNeetu RajaramanОценок пока нет

- Lieberose Solar Park - Presentation-WorkedДокумент43 страницыLieberose Solar Park - Presentation-WorkedNeetu RajaramanОценок пока нет

- Management Accounting System Design Case StudyДокумент12 страницManagement Accounting System Design Case StudyRand Al-akam100% (1)

- Chap 025Документ17 страницChap 025Neetu Rajaraman100% (7)

- Chap 016Документ8 страницChap 016Neetu Rajaraman100% (2)

- Chap 021Документ19 страницChap 021Neetu Rajaraman100% (1)

- Chap 020Документ10 страницChap 020Neetu RajaramanОценок пока нет

- Solution Manual For AccountingДокумент21 страницаSolution Manual For AccountingNeetu RajaramanОценок пока нет

- Chap 026Документ17 страницChap 026Neetu Rajaraman100% (2)

- Chap 024Документ22 страницыChap 024Neetu RajaramanОценок пока нет

- Chap 015Документ4 страницыChap 015Neetu RajaramanОценок пока нет

- Chap 014Документ7 страницChap 014Neetu RajaramanОценок пока нет

- Chap 023Документ23 страницыChap 023Neetu RajaramanОценок пока нет

- Chap 017Документ12 страницChap 017Neetu Rajaraman100% (1)

- Chap 019Документ20 страницChap 019Neetu RajaramanОценок пока нет

- Chap 013Документ12 страницChap 013Neetu RajaramanОценок пока нет

- Chap 010Документ22 страницыChap 010Neetu RajaramanОценок пока нет

- Chap 012Документ11 страницChap 012Neetu RajaramanОценок пока нет

- Chap 011Документ8 страницChap 011Neetu RajaramanОценок пока нет

- Chap 007Документ13 страницChap 007Neetu RajaramanОценок пока нет

- Chap 008Документ17 страницChap 008Neetu RajaramanОценок пока нет

- Chap 009Документ19 страницChap 009Neetu RajaramanОценок пока нет

- Chap 005Документ12 страницChap 005SurajAluruОценок пока нет

- Chap 001Документ17 страницChap 001Neetu RajaramanОценок пока нет

- Chap 004Документ28 страницChap 004mzblossom100% (1)

- Chap 3 Accounting For ManagersДокумент19 страницChap 3 Accounting For ManagersBitan BanerjeeОценок пока нет

- Chapter 8corporation Formation ExercisesДокумент5 страницChapter 8corporation Formation ExerciseshoranghaeОценок пока нет

- Marketing Plan Presentation on Jaul Green Coconut WaterДокумент18 страницMarketing Plan Presentation on Jaul Green Coconut WaterShelveyElmoDias100% (2)

- Estimating Costs For Mining Prefeasibility StudiesДокумент5 страницEstimating Costs For Mining Prefeasibility Studiesdghfhh444t5566gfg0% (1)

- MBH Reference Materials Catalogue GuideДокумент112 страницMBH Reference Materials Catalogue GuideCristian WalkerОценок пока нет

- Electro Smelting of IlmeniteДокумент14 страницElectro Smelting of IlmeniteRavi KiranОценок пока нет

- NeoIT India Cities ComparisonДокумент13 страницNeoIT India Cities Comparisonbskris8727Оценок пока нет

- Saad SB (Q (4+9) ) FinalДокумент4 страницыSaad SB (Q (4+9) ) Finalayazmustafa100% (1)

- MGMT614 (2) NotesДокумент82 страницыMGMT614 (2) NotesSyed Abdul Mussaver ShahОценок пока нет

- Zero HookahДокумент5 страницZero Hookahzszd5nc9tgОценок пока нет

- 02-05-MILESTONE1TASK2 Back To Envelope CalculationДокумент2 страницы02-05-MILESTONE1TASK2 Back To Envelope CalculationMuhamad AnnurОценок пока нет

- Thesis Draft-Dec 15,2019 (Naila Ashraf)Документ114 страницThesis Draft-Dec 15,2019 (Naila Ashraf)AmmaraAfzalОценок пока нет

- San Ramon Feasibility StudyДокумент467 страницSan Ramon Feasibility StudyPabsepulvОценок пока нет

- Solved The Following Relations Describe Monthly Demand and Supply Conditions inДокумент1 страницаSolved The Following Relations Describe Monthly Demand and Supply Conditions inM Bilal SaleemОценок пока нет

- Ref Om McDonald's Generic Strategy & Intensive Growth Strategies - Panmore InstituteДокумент4 страницыRef Om McDonald's Generic Strategy & Intensive Growth Strategies - Panmore InstituteJing CruzОценок пока нет

- India Prepares - April 2012 (Vol.1 Issue 7)Документ96 страницIndia Prepares - April 2012 (Vol.1 Issue 7)India PreparesОценок пока нет

- Forex Price Action Trading Plan BreakdownДокумент13 страницForex Price Action Trading Plan Breakdownnbbarath1988Оценок пока нет

- Tax System India Before and After GSTДокумент4 страницыTax System India Before and After GSTmeenakshishrm250Оценок пока нет

- Strategic Management and Business Policy 15e, Global EditionДокумент37 страницStrategic Management and Business Policy 15e, Global EditionTeh Chu Leong0% (1)

- Pre-Feasibility Study Tuff Tiles Manufacturing Unit: Small and Medium Enterprises Development AuthorityДокумент18 страницPre-Feasibility Study Tuff Tiles Manufacturing Unit: Small and Medium Enterprises Development AuthorityMuhammad SalahuddinОценок пока нет

- CP v1993 n6 2Документ6 страницCP v1993 n6 2leelaОценок пока нет

- Ratchet EffectДокумент3 страницыRatchet EffectCatherine Roween Chico-AlmadenОценок пока нет

- Annual Report Fy0708Документ177 страницAnnual Report Fy0708amitbherwaniОценок пока нет

- Marketing Strategy Starbucks IndiaДокумент5 страницMarketing Strategy Starbucks IndiaMohammad Imad Shahid Khan100% (1)

- CH 2Документ34 страницыCH 2assaОценок пока нет

- Marijuana Seeds SAДокумент7 страницMarijuana Seeds SAMarijuana Seeds SA50% (2)

- Parachute Hair Oil Marketing ReportДокумент21 страницаParachute Hair Oil Marketing Reportanon_3791287190% (1)

- In Na CL1 CL2 PDFДокумент6 страницIn Na CL1 CL2 PDFamaiaferreroОценок пока нет

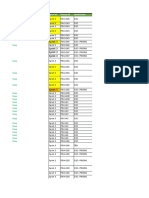

- Sprint 3 Process Tracking ReportДокумент32 страницыSprint 3 Process Tracking ReportPratik MandlikОценок пока нет

- ECO 561 MART Teaching Effectively Eco561martdotcomДокумент27 страницECO 561 MART Teaching Effectively Eco561martdotcomaadam456Оценок пока нет

- Satyam ScandalДокумент9 страницSatyam ScandalAmol AggarwalОценок пока нет