Вам также может понравиться

- What Would Billionaires Do Quickstart GuideДокумент36 страницWhat Would Billionaires Do Quickstart GuideRich Diaz100% (24)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- EVA Vyaderm Case QДокумент14 страницEVA Vyaderm Case QMANSI SHARMAОценок пока нет

- Components of A Compensation PlanДокумент13 страницComponents of A Compensation PlanBarbara GatumutaОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Accounting For Non-AccountantsДокумент129 страницAccounting For Non-Accountantsdesikan_r100% (7)

- Tax Reform For Acceleration and Inclusion LawДокумент28 страницTax Reform For Acceleration and Inclusion LawGloriosa SzeОценок пока нет

- Decision Making 36 Practice Questions & SolutionsДокумент33 страницыDecision Making 36 Practice Questions & SolutionsAbdullah Naeem57% (7)

- Consumer Math Score GuidesДокумент30 страницConsumer Math Score GuidesCrystal WelchОценок пока нет

- A Correlational Study About The Monthly Allowances To The Daily Expenses of The Accountancy and Business Management Grade 11 Students of Sti Academic Center of Las PiñasДокумент17 страницA Correlational Study About The Monthly Allowances To The Daily Expenses of The Accountancy and Business Management Grade 11 Students of Sti Academic Center of Las PiñasMia Grace100% (6)

- Income Taxation Chapter1Документ50 страницIncome Taxation Chapter1Ja Red100% (1)

- BOMA Measuring GuidelinesДокумент2 страницыBOMA Measuring Guidelinespaulstevens1Оценок пока нет

- BOMA Measuring GuidelinesДокумент2 страницыBOMA Measuring Guidelinespaulstevens1Оценок пока нет

- The Nature of Small BusinessДокумент33 страницыThe Nature of Small BusinessRae MorganОценок пока нет

- Item7 KPMG Audit Strategy Planning MemorandumДокумент14 страницItem7 KPMG Audit Strategy Planning Memorandumshane natividad100% (3)

- Warren SM Ch.02 FinalДокумент68 страницWarren SM Ch.02 FinalLidya Silvia Rahma50% (2)

- BBO Invoice 5-4-06Документ1 страницаBBO Invoice 5-4-06paulstevens1Оценок пока нет

- Growing BuildingДокумент3 страницыGrowing Buildingpaulstevens1Оценок пока нет

- Case Study #9Документ1 страницаCase Study #9paulstevens1Оценок пока нет

- Case Study #6Документ1 страницаCase Study #6paulstevens1Оценок пока нет

- Case Study #7Документ1 страницаCase Study #7paulstevens1Оценок пока нет

- Case Study #5Документ1 страницаCase Study #5paulstevens1Оценок пока нет

- Case Study #4Документ1 страницаCase Study #4paulstevens1Оценок пока нет

- Case Study - 1Документ1 страницаCase Study - 1paulstevens1Оценок пока нет

- Iloilo-Capiz-Aklan Road (New Route)Документ1 страницаIloilo-Capiz-Aklan Road (New Route)Legal Division DPWH Region 6Оценок пока нет

- Question No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswerДокумент7 страницQuestion No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswerHarsh KumarОценок пока нет

- Full PVC FootwearДокумент5 страницFull PVC Footwearpradip_kumarОценок пока нет

- Chapter 1 Quiz Review PDFДокумент24 страницыChapter 1 Quiz Review PDFPhil SingletonОценок пока нет

- MAC 1E Study Guide CompleteДокумент225 страницMAC 1E Study Guide Completealicia1990Оценок пока нет

- Quiz - iCPAДокумент15 страницQuiz - iCPAJericho PedragosaОценок пока нет

- SP - Information Gathering & SynthesisДокумент9 страницSP - Information Gathering & SynthesisAshish AnandОценок пока нет

- PayslipДокумент1 страницаPayslipVenu GudlaОценок пока нет

- Weboc. Reg List N Formate DocumentsДокумент7 страницWeboc. Reg List N Formate DocumentsSaeed Ahmed KiyaniОценок пока нет

- Pro Forma Financial Statements 2014 2015 2016 Income StatementДокумент4 страницыPro Forma Financial Statements 2014 2015 2016 Income Statementpriyanka khobragadeОценок пока нет

- Contoh Soal Pelaporan KorporatДокумент4 страницыContoh Soal Pelaporan Korporatirma cahyani kawi0% (1)

- Chapter 15Документ88 страницChapter 15YukiОценок пока нет

- Cost-Volume-Profit and Breakeven AnalysisДокумент36 страницCost-Volume-Profit and Breakeven AnalysisJosartОценок пока нет

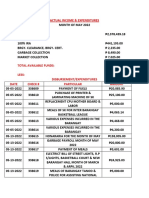

- Actual Income & ExpendituresДокумент5 страницActual Income & Expendituressan nicolas 2nd betis guagua pampangaОценок пока нет

- Warranty Liability Actually Incurred: Total Available Warranty Cost For Products SoldДокумент2 страницыWarranty Liability Actually Incurred: Total Available Warranty Cost For Products SoldCzar RabayaОценок пока нет

- M&M 2006-2007Документ160 страницM&M 2006-2007Ramajit BhartiОценок пока нет

- Fin3n Cap Budgeting Quiz 1Документ1 страницаFin3n Cap Budgeting Quiz 1Kirsten Marie EximОценок пока нет

- Financial Reporting WДокумент345 страницFinancial Reporting Wgordonomond2022Оценок пока нет