Вам также может понравиться

- Myanmar Accounting Standard 7: Statement of Cash FlowsДокумент18 страницMyanmar Accounting Standard 7: Statement of Cash FlowsKyaw Htin WinОценок пока нет

- Direct Property & Casualty Insurance Carrier Revenues World Summary: Market Values & Financials by CountryОт EverandDirect Property & Casualty Insurance Carrier Revenues World Summary: Market Values & Financials by CountryОценок пока нет

- By CA Rajeev Kumar Ranjan Mob. No. 8100052661: Management's Responsibility For The Financial StatementsДокумент3 страницыBy CA Rajeev Kumar Ranjan Mob. No. 8100052661: Management's Responsibility For The Financial Statementspathan1990Оценок пока нет

- Financial Condition Report (FCR) For General Insurance CompaniesДокумент28 страницFinancial Condition Report (FCR) For General Insurance Companiesraheja_ashishОценок пока нет

- Borrowing Costs: Myanmar Accounting Standard 23Документ5 страницBorrowing Costs: Myanmar Accounting Standard 23Kyaw Htin WinОценок пока нет

- Guidance Manual FinalДокумент27 страницGuidance Manual FinalrosdobОценок пока нет

- Form No. 15G: Area Code AO Type Range Code Ao NoДокумент2 страницыForm No. 15G: Area Code AO Type Range Code Ao NoRanjan ManoОценок пока нет

- Know More About Income TaxДокумент5 страницKnow More About Income TaxcanarayananОценок пока нет

- 201455200239Amendments-F.a. 2013 - For UplaodingДокумент7 страниц201455200239Amendments-F.a. 2013 - For UplaodingvishalniОценок пока нет

- India Sudar TaxFile 2005-06Документ7 страницIndia Sudar TaxFile 2005-06India Sudar Educational and Charitable Trust100% (1)

- Lending To Msme SectorДокумент8 страницLending To Msme Sectorpradeep johnОценок пока нет

- Ch13 RevAnsДокумент16 страницCh13 RevAnssamuel_dwumfourОценок пока нет

- Revenue RegulationsДокумент13 страницRevenue RegulationsErika AvedilloОценок пока нет

- Notes On Exempted IncomeДокумент4 страницыNotes On Exempted Incomevaibs8900Оценок пока нет

- Financial Statements and Financial AnalysisДокумент23 страницыFinancial Statements and Financial AnalysisShadab AshfaqОценок пока нет

- Muthoot Fincorp CalrificationsДокумент6 страницMuthoot Fincorp CalrificationslulughoshОценок пока нет

- Allama Iqbal Open University, Islamabad (Department of Commerce)Документ11 страницAllama Iqbal Open University, Islamabad (Department of Commerce)ziabuttОценок пока нет

- Dimaampao Tax NotesДокумент63 страницыDimaampao Tax NotesMaruSalvatierra100% (1)

- MPRA Paper 36783Документ8 страницMPRA Paper 36783ksmuthupandian2098Оценок пока нет

- Financial Results & Limited Review For March 31, 2015 (Standalone) (Result)Документ4 страницыFinancial Results & Limited Review For March 31, 2015 (Standalone) (Result)Shyam SunderОценок пока нет

- Unlock-14.20lkas 2010-Events 20after 20the 20reporting 20periodДокумент10 страницUnlock-14.20lkas 2010-Events 20after 20the 20reporting 20periodAnuruddha RajasuriyaОценок пока нет

- IAS 10 - Sư Kien Sau Ky BC (Eng)Документ8 страницIAS 10 - Sư Kien Sau Ky BC (Eng)Hồ Đan ThụcОценок пока нет

- Appraisal Fast Corporation 12-01-14Документ14 страницAppraisal Fast Corporation 12-01-14Zahid RaihanОценок пока нет

- Working Capital Policy and ManagementДокумент64 страницыWorking Capital Policy and ManagementsevillaarvinОценок пока нет

- IAS 10 Events After The Reporting Period-A Closer LookДокумент7 страницIAS 10 Events After The Reporting Period-A Closer LookFahmi AbdullaОценок пока нет

- Form 3CD NewДокумент16 страницForm 3CD NewRikta KariaОценок пока нет

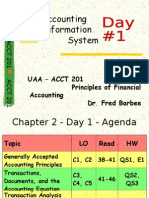

- Accounting Information System: Uaa - Acct 201 Principles of Financial Accounting Dr. Fred BarbeeДокумент55 страницAccounting Information System: Uaa - Acct 201 Principles of Financial Accounting Dr. Fred BarbeeyenzelОценок пока нет

- SOX OverviewДокумент7 страницSOX Overview2010 mujtaba qureshiОценок пока нет

- Accounting Standard 4: Guided By: Dr. Narshing Subash Giri (Sir)Документ12 страницAccounting Standard 4: Guided By: Dr. Narshing Subash Giri (Sir)Siddhant GaikwadОценок пока нет

- C EM Peshawer 1Документ14 страницC EM Peshawer 1Sikandar KhattakОценок пока нет

- Central Board of Direct Taxes, E-Filing Project: ITR 1 - Validation Rules For AY 2018-19Документ10 страницCentral Board of Direct Taxes, E-Filing Project: ITR 1 - Validation Rules For AY 2018-19LEo GEnji KhunnuОценок пока нет

- Kaiser Tax Sheltered Annuity 5500 For 2010Документ38 страницKaiser Tax Sheltered Annuity 5500 For 2010James LindonОценок пока нет

- Accounting FrameworkДокумент6 страницAccounting FrameworkjoannaberroОценок пока нет

- Ias 10Документ12 страницIas 10Reever RiverОценок пока нет

- CPAR Financial StatementsДокумент5 страницCPAR Financial StatementsAnjo EllisОценок пока нет

- Chapter 1 Introduction of Accounting and Financial Reporting For Government and Not For Profit.Документ5 страницChapter 1 Introduction of Accounting and Financial Reporting For Government and Not For Profit.molango007Оценок пока нет

- Kieso IFRS TestBank Ch03Документ44 страницыKieso IFRS TestBank Ch03Zhim Handjoko100% (1)

- Artisan Card BimayoyonaДокумент8 страницArtisan Card BimayoyonayahooshuvajoyОценок пока нет

- Revised Schedule VIДокумент23 страницыRevised Schedule VIJitendra GahanduleОценок пока нет

- Ans Key IMO Class 1 To 10 01 12 16Документ10 страницAns Key IMO Class 1 To 10 01 12 16DaisyQueenОценок пока нет

- Ch24 Full Disclosure in Financial ReportingДокумент31 страницаCh24 Full Disclosure in Financial ReportingAries BautistaОценок пока нет

- Solution Financial Management Strategy May 2009Документ7 страницSolution Financial Management Strategy May 2009samuel_dwumfourОценок пока нет

- Chap 010Документ16 страницChap 010trinhbang100% (1)

- Form No.16: Part AДокумент5 страницForm No.16: Part APradeep KumarОценок пока нет

- Short Form Return of Organization Exempt From Income Tax: Inspectio Ec - 31, 20 04 94: 325 6921Документ3 страницыShort Form Return of Organization Exempt From Income Tax: Inspectio Ec - 31, 20 04 94: 325 6921lesliebrodieОценок пока нет

- Reliance Auditors ReportДокумент6 страницReliance Auditors Reportjinalshah21097946Оценок пока нет

- Final - Asset Accounting ProcedureДокумент38 страницFinal - Asset Accounting ProcedureSonianNareshОценок пока нет

- Introduction: This Memorandum Sets Out Our Proposed Strategy For Auditing The Karnataka State Khadi and Village Industries Board (KVIB) For The Year Ended 31 March 2006Документ3 страницыIntroduction: This Memorandum Sets Out Our Proposed Strategy For Auditing The Karnataka State Khadi and Village Industries Board (KVIB) For The Year Ended 31 March 2006Rachyl SacramedОценок пока нет

- Annex VII E3h8 Expendverif enДокумент22 страницыAnnex VII E3h8 Expendverif ensdiamanОценок пока нет

- Karpagam Institute of Technology Mca Continuous Assessment Internal Test-IДокумент5 страницKarpagam Institute of Technology Mca Continuous Assessment Internal Test-IanglrОценок пока нет

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Документ4 страницыStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderОценок пока нет

- Navios Maritime Holdings Inc - Form 20-F (Apr-06-2011)Документ261 страницаNavios Maritime Holdings Inc - Form 20-F (Apr-06-2011)charliej973Оценок пока нет

- Standalone & Consolidated Financial Results, Auditors Report For June 30, 2016 (Result)Документ6 страницStandalone & Consolidated Financial Results, Auditors Report For June 30, 2016 (Result)Shyam SunderОценок пока нет

- Witholding Tax To VAT NotesДокумент22 страницыWitholding Tax To VAT NoteslchieSОценок пока нет

- Order in The Matter of Greentouch Projects Ltd.Документ15 страницOrder in The Matter of Greentouch Projects Ltd.Shyam Sunder0% (1)

- JULY 14, 2010: by Pritam Mahure, CA A Business Group Venturing in Different Business Segments UsuallyДокумент8 страницJULY 14, 2010: by Pritam Mahure, CA A Business Group Venturing in Different Business Segments UsuallySeemaNaikОценок пока нет

- O o o o o O: Amortisation, Acquisition, Restructure Charges, In-Process R&D, Pension CurtailmentДокумент18 страницO o o o o O: Amortisation, Acquisition, Restructure Charges, In-Process R&D, Pension CurtailmentmkОценок пока нет

- FAQsДокумент10 страницFAQsrajdeeppawarОценок пока нет

- Events After BS DATE Recognition and Measurement From WWWДокумент8 страницEvents After BS DATE Recognition and Measurement From WWWszn1Оценок пока нет

- Platinum Sales MixДокумент1 страницаPlatinum Sales MixKyaw Htin WinОценок пока нет

- June'16 Sales QtyДокумент61 страницаJune'16 Sales QtyKyaw Htin WinОценок пока нет

- Survey ResearchДокумент5 страницSurvey ResearchKyaw Htin WinОценок пока нет

- Purchase Cash Paid To ESI Date 11.7.15 RichДокумент11 страницPurchase Cash Paid To ESI Date 11.7.15 RichKyaw Htin WinОценок пока нет

- MKN BudgetДокумент1 страницаMKN BudgetKyaw Htin WinОценок пока нет

- Purchase Cash Paid To ESI Date 18.7.2015 RichДокумент9 страницPurchase Cash Paid To ESI Date 18.7.2015 RichKyaw Htin WinОценок пока нет

- Lcci BS 1Документ17 страницLcci BS 1Kyaw Htin WinОценок пока нет

- K1 ExpenseДокумент30 страницK1 ExpenseKyaw Htin WinОценок пока нет

- CustomerДокумент2 страницыCustomerKyaw Htin WinОценок пока нет

- ReadmeДокумент1 страницаReadmebilma85Оценок пока нет

- Yangon ExpenseДокумент2 страницыYangon ExpenseKyaw Htin WinОценок пока нет

- Hercule Monthly AC-AUG.2013Документ20 страницHercule Monthly AC-AUG.2013Kyaw Htin WinОценок пока нет

- Account ChatДокумент4 страницыAccount ChatKyaw Htin WinОценок пока нет

- Transportation CostДокумент2 страницыTransportation CostKyaw Htin WinОценок пока нет

- Hercule Monthly AC-AUG.2013Документ20 страницHercule Monthly AC-AUG.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC JUNE 2014Документ34 страницыHercule Monthly AC JUNE 2014Kyaw Htin WinОценок пока нет

- Lcci BS 1Документ17 страницLcci BS 1Kyaw Htin WinОценок пока нет

- Hercule Monthly AC FEB 2014Документ34 страницыHercule Monthly AC FEB 2014Kyaw Htin WinОценок пока нет

- Hercule Monthly AC JAN 2014 AmenedДокумент31 страницаHercule Monthly AC JAN 2014 AmenedKyaw Htin WinОценок пока нет

- Hercule Monthly AC MAY 2014Документ39 страницHercule Monthly AC MAY 2014Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-OCT.2013Документ21 страницаHercule Monthly AC-OCT.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC Nov 2012 Dec 2012Документ19 страницHercule Monthly AC Nov 2012 Dec 2012Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-NOV.2013Документ37 страницHercule Monthly AC-NOV.2013Kyaw Htin WinОценок пока нет

- Accounts For Non-Profit Making OrganisationsДокумент2 страницыAccounts For Non-Profit Making OrganisationsKyaw Htin WinОценок пока нет

- Hercule Monthly AC APR 2014 11.5.2014Документ38 страницHercule Monthly AC APR 2014 11.5.2014Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-AUG.2013Документ20 страницHercule Monthly AC-AUG.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-JUNE.2013Документ20 страницHercule Monthly AC-JUNE.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-AUG.2013Документ20 страницHercule Monthly AC-AUG.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-FEB.2013Документ19 страницHercule Monthly AC-FEB.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-DeC.2013Документ40 страницHercule Monthly AC-DeC.2013Kyaw Htin WinОценок пока нет

- Jurisdiction: NAME: Lordy Jessah B. Aggabao Student No. 19-13758-526 InstructionsДокумент6 страницJurisdiction: NAME: Lordy Jessah B. Aggabao Student No. 19-13758-526 InstructionsKen AggabaoОценок пока нет

- Social Contract Theory by Hobbes Locke AДокумент15 страницSocial Contract Theory by Hobbes Locke APulkit ChannanОценок пока нет

- Case Digests 010619Документ9 страницCase Digests 010619Andrea IvanneОценок пока нет

- Addendum To The Extrajudicial Settlement of EstateДокумент6 страницAddendum To The Extrajudicial Settlement of EstateZarjoshkyen MactarОценок пока нет

- Rule 6Документ342 страницыRule 6airene_edano4678Оценок пока нет

- Courtesy of Professor Kaufman: Part II - EssayДокумент3 страницыCourtesy of Professor Kaufman: Part II - EssayEmely AlmonteОценок пока нет

- LOMLE - Case Digest 2Документ35 страницLOMLE - Case Digest 2Rino Gonzales100% (1)

- Lico Vs ComelecДокумент20 страницLico Vs ComelecyanieggОценок пока нет

- MOA 1-Classroom Beautification-GPTAДокумент2 страницыMOA 1-Classroom Beautification-GPTASALVACION MABELINОценок пока нет

- Statutory CorporationДокумент5 страницStatutory CorporationSebastian GhermanОценок пока нет

- Bret D. Landrith v. Don Jordon Secretary of SRS, Et Al 10C1436Документ23 страницыBret D. Landrith v. Don Jordon Secretary of SRS, Et Al 10C1436LandrithОценок пока нет

- Kuwait V Aminoil 66 ILR 518 PDFДокумент109 страницKuwait V Aminoil 66 ILR 518 PDFΜάνος ΓιακουμάκηςОценок пока нет

- Sps. Del Campo vs. Heirs of Regalado, Sr.Документ2 страницыSps. Del Campo vs. Heirs of Regalado, Sr.May RMОценок пока нет

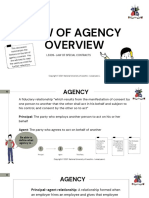

- L3309 - Law of Agency - End of Module SummaryДокумент27 страницL3309 - Law of Agency - End of Module SummarySethetse Mats'oeleОценок пока нет

- Sample Demurrer To Answer For CaliforniaДокумент4 страницыSample Demurrer To Answer For CaliforniaStan Burman83% (6)

- Republic Vs SerenoДокумент39 страницRepublic Vs SerenoKP Gonzales CabauatanОценок пока нет

- KCHavNBtEeibDRJgCTeJlA - Introduction To English Common Law MOOCДокумент2 страницыKCHavNBtEeibDRJgCTeJlA - Introduction To English Common Law MOOCAngelikRdjОценок пока нет

- PIL Forum Non ConvenienceДокумент73 страницыPIL Forum Non ConvenienceDon BallesterosОценок пока нет

- Installation, Storage, and Compute With Windows Server 2016Документ790 страницInstallation, Storage, and Compute With Windows Server 2016Cristina MariaОценок пока нет

- March 13Документ4 страницыMarch 13ACSOtweetОценок пока нет

- Ra 10884Документ4 страницыRa 10884Kevin BonaobraОценок пока нет

- East Bengal Estate Acquisition Rules, 1951Документ38 страницEast Bengal Estate Acquisition Rules, 1951KBSОценок пока нет

- Judge Kurtis Loy DocktedДокумент2 страницыJudge Kurtis Loy DocktedConflict GateОценок пока нет

- SF C1 Request Letter From PIA For Changes in Project ParametersДокумент5 страницSF C1 Request Letter From PIA For Changes in Project ParametersVINAY BANSAL100% (1)

- Case Summary - Lily Thomas v. Union of I PDFДокумент3 страницыCase Summary - Lily Thomas v. Union of I PDFVivek SinghОценок пока нет

- Complete Legal Ethics Neu Barreviewer2022Документ14 страницComplete Legal Ethics Neu Barreviewer2022Jan MendezОценок пока нет

- Payment Form: Voluntary Assessment and Payment Program (VAPP)Документ2 страницыPayment Form: Voluntary Assessment and Payment Program (VAPP)Joel SyОценок пока нет

- IMMI Refusal NotificationДокумент2 страницыIMMI Refusal NotificationAnn Borong100% (1)

- Guest Artists - RulebookДокумент5 страницGuest Artists - Rulebooktizzler07Оценок пока нет

- Learn the Essentials of Business Law in 15 DaysОт EverandLearn the Essentials of Business Law in 15 DaysРейтинг: 4 из 5 звезд4/5 (13)

- How to Win Your Case In Traffic Court Without a LawyerОт EverandHow to Win Your Case In Traffic Court Without a LawyerРейтинг: 4 из 5 звезд4/5 (5)

- Fundamentals of Theatrical Design: A Guide to the Basics of Scenic, Costume, and Lighting DesignОт EverandFundamentals of Theatrical Design: A Guide to the Basics of Scenic, Costume, and Lighting DesignРейтинг: 3.5 из 5 звезд3.5/5 (3)

- The Small-Business Guide to Government Contracts: How to Comply with the Key Rules and Regulations . . . and Avoid Terminated Agreements, Fines, or WorseОт EverandThe Small-Business Guide to Government Contracts: How to Comply with the Key Rules and Regulations . . . and Avoid Terminated Agreements, Fines, or WorseОценок пока нет

- How to Win Your Case in Small Claims Court Without a LawyerОт EverandHow to Win Your Case in Small Claims Court Without a LawyerРейтинг: 5 из 5 звезд5/5 (1)

- Digital Technical Theater Simplified: High Tech Lighting, Audio, Video and More on a Low BudgetОт EverandDigital Technical Theater Simplified: High Tech Lighting, Audio, Video and More on a Low BudgetОценок пока нет

- The Business of Broadway: An Insider's Guide to Working, Producing, and Investing in the World's Greatest Theatre CommunityОт EverandThe Business of Broadway: An Insider's Guide to Working, Producing, and Investing in the World's Greatest Theatre CommunityОценок пока нет

- Starting Your Career as a Photo Stylist: A Comprehensive Guide to Photo Shoots, Marketing, Business, Fashion, Wardrobe, Off Figure, Product, Prop, Room Sets, and Food StylingОт EverandStarting Your Career as a Photo Stylist: A Comprehensive Guide to Photo Shoots, Marketing, Business, Fashion, Wardrobe, Off Figure, Product, Prop, Room Sets, and Food StylingРейтинг: 5 из 5 звезд5/5 (1)