Вам также может понравиться

- Asset Classification and Provisioning Regulations 2017 ENG PDFДокумент4 страницыAsset Classification and Provisioning Regulations 2017 ENG PDFNelsonОценок пока нет

- Format of Financial Statements Under The Revised Schedule VIДокумент97 страницFormat of Financial Statements Under The Revised Schedule VIDebadarshi RoyОценок пока нет

- 5.1 Financial Accounting-15cp51t PDFДокумент22 страницы5.1 Financial Accounting-15cp51t PDFSuraj NK100% (1)

- Fixed Asset Register SampleДокумент40 страницFixed Asset Register SampleTheresaОценок пока нет

- Inter Company Process v6 SYДокумент65 страницInter Company Process v6 SYrikizalkarnain88Оценок пока нет

- PFRS 15 Work ProgramДокумент101 страницаPFRS 15 Work ProgramMichael ArciagaОценок пока нет

- UAP Chart of Accounts 070110Документ1 страницаUAP Chart of Accounts 070110chaskar1983Оценок пока нет

- Bad Debts ProcedureДокумент3 страницыBad Debts ProcedureCM_NguyenОценок пока нет

- Presentation On Pre-Audit of PaymentДокумент55 страницPresentation On Pre-Audit of Paymentsanjay_sbi100% (1)

- Diversey Product Catalogue 28ppДокумент28 страницDiversey Product Catalogue 28ppJohn WaweruОценок пока нет

- IC Internal Audit Checklist 8624Документ3 страницыIC Internal Audit Checklist 8624Tarun KumarОценок пока нет

- Corporate Budget Memo No. 39Документ95 страницCorporate Budget Memo No. 39mcla28Оценок пока нет

- Activity Based Costing With Two ActivitiesДокумент3 страницыActivity Based Costing With Two ActivitiesArun JosephОценок пока нет

- ChartOfAccount YAIN 2012Документ20 страницChartOfAccount YAIN 2012litu84Оценок пока нет

- Fixed Assets Purchse Flow ChartДокумент41 страницаFixed Assets Purchse Flow ChartAbu NaserОценок пока нет

- Account PayablesДокумент95 страницAccount Payablestiwari_anupam2003Оценок пока нет

- Old Dominion University Office of Finance Procedure Manual Title: Fixed Asset Management Procedure: 3-800Документ3 страницыOld Dominion University Office of Finance Procedure Manual Title: Fixed Asset Management Procedure: 3-800Priyanka BujugundlaОценок пока нет

- Audit Responsibilities and ObjectivesДокумент25 страницAudit Responsibilities and ObjectivesNisa sudinkebudayaan100% (1)

- Financial Risk MetricsДокумент21 страницаFinancial Risk MetricsSandip Chaudhuri100% (1)

- Accounting For RoyaltiesДокумент19 страницAccounting For RoyaltieskwameОценок пока нет

- Quality Management ProcessesДокумент9 страницQuality Management Processesselinasimpson0701Оценок пока нет

- K1 ExpenseДокумент30 страницK1 ExpenseKyaw Htin WinОценок пока нет

- Manual - Fixed AssetsДокумент48 страницManual - Fixed AssetsIliIllilI IliIllilIIliIllilIОценок пока нет

- Management Accounting SampleДокумент25 страницManagement Accounting SampleEdward Baffoe100% (1)

- Audit Fees For Initial Audit Engagements Before and After SOXДокумент20 страницAudit Fees For Initial Audit Engagements Before and After SOXNugraha AhmadОценок пока нет

- Bit - Financial StatementsДокумент10 страницBit - Financial StatementsAldrin ZolinaОценок пока нет

- Capex Form TemplateДокумент2 страницыCapex Form TemplateAnonymous 3aUuJQОценок пока нет

- Debit NoteДокумент1 страницаDebit NoteShaik NoorshaОценок пока нет

- ISA 610 Using The Work of Internal AuditorsДокумент4 страницыISA 610 Using The Work of Internal AuditorsNURUL FAEIZAH BINTI AHMAD ANWAR / UPMОценок пока нет

- Financial Report 2017Документ106 страницFinancial Report 2017Le Phong100% (1)

- Finance AccountsДокумент13 страницFinance AccountsVishal ChaudharyОценок пока нет

- Compensating ControlДокумент10 страницCompensating Controlkasim_arkin2707100% (1)

- Statutory Checklist-Tds OthersДокумент15 страницStatutory Checklist-Tds OthersGaurav KumarОценок пока нет

- Chart of AccountДокумент300 страницChart of AccountyadadОценок пока нет

- Coa Mapping Int enДокумент26 страницCoa Mapping Int enMuhammad Javed IqbalОценок пока нет

- The Chart of Accounts For Banks and Other Financial Institutions of The Republic of MoldovaДокумент87 страницThe Chart of Accounts For Banks and Other Financial Institutions of The Republic of MoldovaPedro PrietoОценок пока нет

- Audit Module 1 - Trial Balance Account MappingДокумент6 страницAudit Module 1 - Trial Balance Account MappingGaurav KumarОценок пока нет

- TEM Reporting DashboardДокумент21 страницаTEM Reporting DashboardLawrence BrownОценок пока нет

- University of Exeter B.SC Hon of Mining EngineeringДокумент5 страницUniversity of Exeter B.SC Hon of Mining Engineeringbeku_ggs_bekuОценок пока нет

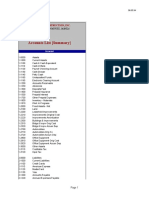

- Accounts List (Summary) : CC Puno Jr. Construction, IncДокумент4 страницыAccounts List (Summary) : CC Puno Jr. Construction, IncAndrew CatamaОценок пока нет

- Investments ProgramfdgfgfДокумент30 страницInvestments Programfdgfgfredearth2929Оценок пока нет

- Audit Planning Scenarios AnalysisДокумент6 страницAudit Planning Scenarios AnalysisUsman PirzadaОценок пока нет

- Sop 02 10Документ4 страницыSop 02 10neha vatsОценок пока нет

- Airport Service Level Agreement (SLA) - Best PracticeДокумент3 страницыAirport Service Level Agreement (SLA) - Best PracticeSa Xev100% (1)

- Fixed Asset RegisterДокумент2 страницыFixed Asset RegisterUsman AhmadОценок пока нет

- Accounting System MannualДокумент84 страницыAccounting System MannualBhushan ParalkarОценок пока нет

- NIA R12 Finance FlowchartДокумент6 страницNIA R12 Finance FlowchartAngelita BarcelonaОценок пока нет

- Sap Fi AP Manual For Common Daily TransactionsДокумент72 страницыSap Fi AP Manual For Common Daily TransactionsMehmood Ul HassanОценок пока нет

- Internal Controls QuestionnaireДокумент5 страницInternal Controls QuestionnaireCarlos Eduardo C. da SilvaОценок пока нет

- Cma DataДокумент18 страницCma DataPriti Ranjan NaskarОценок пока нет

- Cash Book RulesДокумент33 страницыCash Book RulesNarasimha Murthy InampudiОценок пока нет

- Advanced AccountingДокумент13 страницAdvanced AccountingprateekfreezerОценок пока нет

- Draft Attached Formats: 1. Resignation Letter by AuditorДокумент6 страницDraft Attached Formats: 1. Resignation Letter by AuditorAlamba Charitable TrustОценок пока нет

- Cost Center and GL CodeДокумент51 страницаCost Center and GL CodeHarshanand KalgeОценок пока нет

- Difference Between Ind As 16, As 10Документ6 страницDifference Between Ind As 16, As 10VivekОценок пока нет

- Nepal Accounting Standards On Property, Plant and Equipment: Initial Cost 11 Subsequent Cost 12-14Документ24 страницыNepal Accounting Standards On Property, Plant and Equipment: Initial Cost 11 Subsequent Cost 12-14Gemini_0804Оценок пока нет

- Plant, Property and EquipmentДокумент21 страницаPlant, Property and Equipmentumarsaleem92Оценок пока нет

- Property, Plant and Equipment: International Accounting Standard 16Документ13 страницProperty, Plant and Equipment: International Accounting Standard 16Laura BalcanОценок пока нет

- Module 6 Property, Plant, and EquipmentДокумент31 страницаModule 6 Property, Plant, and EquipmentNicole ConcepcionОценок пока нет

- Indian Accounting Standard (Ind AS) 16 Property, Plant and EquipmentДокумент20 страницIndian Accounting Standard (Ind AS) 16 Property, Plant and EquipmentSandeepPusarapuОценок пока нет

- June'16 Sales QtyДокумент61 страницаJune'16 Sales QtyKyaw Htin WinОценок пока нет

- CustomerДокумент2 страницыCustomerKyaw Htin WinОценок пока нет

- Purchase Cash Paid To ESI Date 18.7.2015 RichДокумент9 страницPurchase Cash Paid To ESI Date 18.7.2015 RichKyaw Htin WinОценок пока нет

- Purchase Cash Paid To ESI Date 11.7.15 RichДокумент11 страницPurchase Cash Paid To ESI Date 11.7.15 RichKyaw Htin WinОценок пока нет

- Platinum Sales MixДокумент1 страницаPlatinum Sales MixKyaw Htin WinОценок пока нет

- Account ChatДокумент4 страницыAccount ChatKyaw Htin WinОценок пока нет

- Survey ResearchДокумент5 страницSurvey ResearchKyaw Htin WinОценок пока нет

- MKN BudgetДокумент1 страницаMKN BudgetKyaw Htin WinОценок пока нет

- Transportation CostДокумент2 страницыTransportation CostKyaw Htin WinОценок пока нет

- ReadmeДокумент1 страницаReadmebilma85Оценок пока нет

- Yangon ExpenseДокумент2 страницыYangon ExpenseKyaw Htin WinОценок пока нет

- K1 ExpenseДокумент30 страницK1 ExpenseKyaw Htin WinОценок пока нет

- Lcci BS 1Документ17 страницLcci BS 1Kyaw Htin WinОценок пока нет

- Lcci BS 1Документ17 страницLcci BS 1Kyaw Htin WinОценок пока нет

- Hercule Monthly AC FEB 2014Документ34 страницыHercule Monthly AC FEB 2014Kyaw Htin WinОценок пока нет

- Hercule Monthly AC APR 2014 11.5.2014Документ38 страницHercule Monthly AC APR 2014 11.5.2014Kyaw Htin WinОценок пока нет

- Hercule Monthly AC MAY 2014Документ39 страницHercule Monthly AC MAY 2014Kyaw Htin WinОценок пока нет

- Hercule Monthly AC JUNE 2014Документ34 страницыHercule Monthly AC JUNE 2014Kyaw Htin WinОценок пока нет

- Accounts For Non-Profit Making OrganisationsДокумент2 страницыAccounts For Non-Profit Making OrganisationsKyaw Htin WinОценок пока нет

- Hercule Monthly AC JAN 2014 AmenedДокумент31 страницаHercule Monthly AC JAN 2014 AmenedKyaw Htin WinОценок пока нет

- Hercule Monthly AC-NOV.2013Документ37 страницHercule Monthly AC-NOV.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-AUG.2013Документ20 страницHercule Monthly AC-AUG.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-OCT.2013Документ21 страницаHercule Monthly AC-OCT.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-AUG.2013Документ20 страницHercule Monthly AC-AUG.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-FEB.2013Документ19 страницHercule Monthly AC-FEB.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC Nov 2012 Dec 2012Документ19 страницHercule Monthly AC Nov 2012 Dec 2012Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-AUG.2013Документ20 страницHercule Monthly AC-AUG.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-JUNE.2013Документ20 страницHercule Monthly AC-JUNE.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-DeC.2013Документ40 страницHercule Monthly AC-DeC.2013Kyaw Htin WinОценок пока нет

- Hercule Monthly AC-AUG.2013Документ20 страницHercule Monthly AC-AUG.2013Kyaw Htin WinОценок пока нет

- Taxation First Preboard 93 - QuestionnaireДокумент16 страницTaxation First Preboard 93 - QuestionnaireAmeroden AbdullahОценок пока нет

- US Internal Revenue Service: p1459Документ111 страницUS Internal Revenue Service: p1459IRSОценок пока нет

- Fall 2015 Test 3Документ14 страницFall 2015 Test 3Adam MichaelОценок пока нет

- Managerial Accounting Final Presentation: Seligram, Inc.: Electronic Testing OperationsДокумент12 страницManagerial Accounting Final Presentation: Seligram, Inc.: Electronic Testing OperationsJuragan BiasaОценок пока нет

- ACC, Capter Wiz-Quespapers.Документ32 страницыACC, Capter Wiz-Quespapers.minakshi sahuОценок пока нет

- Ebook b291 Ab E3i1 Web027466Документ40 страницEbook b291 Ab E3i1 Web027466Graham Burns100% (1)

- Leases - Payment in AdvanceДокумент21 страницаLeases - Payment in AdvanceNurul Ain Kisz'tinaОценок пока нет

- Fixed Asset Register, MethodsДокумент6 страницFixed Asset Register, Methodsuzma qadirОценок пока нет

- Chap 003Документ98 страницChap 003Mokhtar Elshaer0% (1)

- ICAI QuestionsДокумент244 страницыICAI QuestionsdonaОценок пока нет

- AS Part 2Документ209 страницAS Part 2hariinshrОценок пока нет

- Week 4 - AEC 201 - Activities-PrelimДокумент12 страницWeek 4 - AEC 201 - Activities-PrelimNathalie HeartОценок пока нет

- 03 LeasingДокумент16 страниц03 Leasingnotes.mcpuОценок пока нет

- Updates On Pas, PFRS, IfricДокумент6 страницUpdates On Pas, PFRS, IfricPrincessAngelaDeLeonОценок пока нет

- Chapter 16Документ21 страницаChapter 16Aiko E. LaraОценок пока нет

- Accounting: Plant AssetsДокумент41 страницаAccounting: Plant AssetsFlower T.Оценок пока нет

- National IncomeДокумент14 страницNational Incomevmktpt100% (1)

- Financial Reporting & Analysis Solutions Statement of Cash Flows ExercisesДокумент72 страницыFinancial Reporting & Analysis Solutions Statement of Cash Flows ExerciseskazimkorogluОценок пока нет

- Intermediate Accounting 1st Edition Gordon Solutions Manual 1Документ61 страницаIntermediate Accounting 1st Edition Gordon Solutions Manual 1shaun100% (36)

- Quiz 5Документ7 страницQuiz 5Arjay CarolinoОценок пока нет

- 6 PMP6 CostДокумент62 страницы6 PMP6 CostKareem Mohammad100% (1)

- Valuation PROFESSIONAL PRACTICEДокумент15 страницValuation PROFESSIONAL PRACTICEsanchit guptaОценок пока нет

- Heineken ENG Financial StatementsДокумент85 страницHeineken ENG Financial StatementscrazyscorpionОценок пока нет

- Lums Cases Bibliography FinalДокумент171 страницаLums Cases Bibliography FinalAli ShehrwaniОценок пока нет

- MCQ in Engineering Economics Part 3 ECE Board ExamДокумент17 страницMCQ in Engineering Economics Part 3 ECE Board ExamEj ParañalОценок пока нет

- Income Statement (Accrual) PT ManunggalДокумент1 страницаIncome Statement (Accrual) PT ManunggalDelia OktaОценок пока нет

- The Budget Committee of Miranda Fashions An Upscale Women S ClothingДокумент1 страницаThe Budget Committee of Miranda Fashions An Upscale Women S ClothingAmit PandeyОценок пока нет

- Audit of Insurance CompaniesДокумент15 страницAudit of Insurance CompaniesYoung MetroОценок пока нет

- Week 11 Tutorial WorkingsДокумент51 страницаWeek 11 Tutorial WorkingsKwang Yi JuinОценок пока нет

- Depreciation and Carrying AmountДокумент12 страницDepreciation and Carrying AmountNouman MujahidОценок пока нет