Вам также может понравиться

- EuropeLPGReport Sample02082013Документ5 страницEuropeLPGReport Sample02082013Melody CottonОценок пока нет

- FER-White Paper-Sulphur Market VolatilityДокумент4 страницыFER-White Paper-Sulphur Market VolatilityvhlmОценок пока нет

- Crude Oil MKT WireДокумент23 страницыCrude Oil MKT WireAdi SutrisnoОценок пока нет

- Guinea Mining GuideДокумент32 страницыGuinea Mining GuidePalak LimbachiyaОценок пока нет

- Aluminium Outlook CRU 2018 ReportДокумент46 страницAluminium Outlook CRU 2018 ReportMohammad Abubakar SiddiqОценок пока нет

- Industry prepares for Sulphur 2020 deadlineДокумент24 страницыIndustry prepares for Sulphur 2020 deadlinevran77Оценок пока нет

- SulphurДокумент15 страницSulphurrsvasanОценок пока нет

- S&P GlobalДокумент17 страницS&P GlobalVamsi Krishna EvkОценок пока нет

- IHS Markit Overview of Specialty Chemicals InfographicДокумент1 страницаIHS Markit Overview of Specialty Chemicals Infographicalejo ramirezОценок пока нет

- Energy Transition World Economic Forum Report 2021Документ51 страницаEnergy Transition World Economic Forum Report 2021Gonzalo FranklinОценок пока нет

- Argus Oil Market Discussions: LPGДокумент42 страницыArgus Oil Market Discussions: LPGALI ABBASОценок пока нет

- Coal Trader International: Glencore Limiting Coal Output Seen Boosting Fob Newcastle PricesДокумент11 страницCoal Trader International: Glencore Limiting Coal Output Seen Boosting Fob Newcastle PricesI Gede Artha Wijaya100% (1)

- SulphurДокумент15 страницSulphurSusbsisvОценок пока нет

- AmmoniaДокумент37 страницAmmoniaJose Deniz0% (1)

- Decarbonizing Steel PresentationДокумент27 страницDecarbonizing Steel PresentationMitone DiazОценок пока нет

- The Sulphur CompanyДокумент20 страницThe Sulphur CompanyNenadОценок пока нет

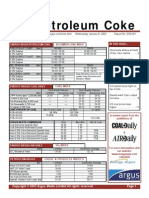

- Pet CokeДокумент12 страницPet Cokezementhead100% (1)

- Argus: Metals InternationalДокумент29 страницArgus: Metals InternationalrezaОценок пока нет

- Alufer - Bauxite Factsheet PDFДокумент2 страницыAlufer - Bauxite Factsheet PDFRaraОценок пока нет

- 7c RM Fertilizers EtcДокумент22 страницы7c RM Fertilizers EtcAbhishek DharОценок пока нет

- Representation of Coal and Coal Derivatives in Process ModellingДокумент16 страницRepresentation of Coal and Coal Derivatives in Process ModellingPrateek PatelОценок пока нет

- Apag 20171110Документ16 страницApag 20171110egif_thahirОценок пока нет

- Americas Chemicals Outlook 2016Документ84 страницыAmericas Chemicals Outlook 2016stavros7Оценок пока нет

- Challenging The Traditional Hydrometallurgy Curriculum-An Industry PerspectiveДокумент9 страницChallenging The Traditional Hydrometallurgy Curriculum-An Industry PerspectiveGustavo Gabriel JimenezОценок пока нет

- Vam PricesДокумент28 страницVam PricesMandar J DeshpandeОценок пока нет

- Carbon BlackДокумент20 страницCarbon BlackHerlin MorenoОценок пока нет

- Physical and Thermal Treatment of Phosphate OresДокумент26 страницPhysical and Thermal Treatment of Phosphate OresManoel Carlos Cerqueira100% (2)

- Summary of Findings From HYBRIT Pre-Feasibility Study 2016-2017Документ11 страницSummary of Findings From HYBRIT Pre-Feasibility Study 2016-2017Okko NОценок пока нет

- Ammonium Nitrate FertilizersДокумент4 страницыAmmonium Nitrate FertilizersLuiz Rodrigo AssisОценок пока нет

- Solvents WireДокумент9 страницSolvents Wirerbrijeshgbiresearch100% (1)

- Rossing - Production ProcessДокумент27 страницRossing - Production ProcessJan LubbeОценок пока нет

- Umm Lulu - UMMLULU201810Документ6 страницUmm Lulu - UMMLULU201810asad raza100% (2)

- MEPS Steel Products Price Levels Across 2008-09Документ2 страницыMEPS Steel Products Price Levels Across 2008-09jtpmlОценок пока нет

- Marketing 2Документ12 страницMarketing 2Saul Martinez MolinaОценок пока нет

- HSFO ReportДокумент17 страницHSFO ReportAtif IqbalОценок пока нет

- GLOBAL PELLET MARKETS & BIOMASS CO-FIRING GROWTHДокумент28 страницGLOBAL PELLET MARKETS & BIOMASS CO-FIRING GROWTHNorzuriani Mohamed SeberiОценок пока нет

- Stainless Steel PriceДокумент1 страницаStainless Steel PriceVicky GautamОценок пока нет

- Catalyst Poisoning or DeactivationДокумент2 страницыCatalyst Poisoning or Deactivationdimas setyawan100% (1)

- FINAL Presentation For ARA ConferenceДокумент26 страницFINAL Presentation For ARA Conferencesaleh4060Оценок пока нет

- Platts APAG Report 01 09 2015 PDFДокумент14 страницPlatts APAG Report 01 09 2015 PDFSafri IchsanОценок пока нет

- Booklet 7 FinalДокумент36 страницBooklet 7 FinalpavijayaОценок пока нет

- Bitumen Report Argus AsphaltДокумент23 страницыBitumen Report Argus AsphaltAtif IqbalОценок пока нет

- UHDE - Nitrate Fertilizers PDFДокумент24 страницыUHDE - Nitrate Fertilizers PDFvzgscribdОценок пока нет

- Small Scale Methaforming Unit Maximizes ProfitsДокумент16 страницSmall Scale Methaforming Unit Maximizes ProfitsramatajamaОценок пока нет

- Oman Industrial Free Trade ZonesДокумент8 страницOman Industrial Free Trade ZonesOdin Marine ServiceОценок пока нет

- Capabilities and Experience in Nickel ResearchДокумент10 страницCapabilities and Experience in Nickel ResearchDavid Budi SaputraОценок пока нет

- 2 Maaden PDFДокумент29 страниц2 Maaden PDFAnonymous q9eCZHMuSОценок пока нет

- AMR SummaryДокумент37 страницAMR SummaryChatkamol KaewbuddeeОценок пока нет

- Petrochemical Feedstock Outlook - A Tale of Two Markets: 7 November 2019 - SingaporeДокумент19 страницPetrochemical Feedstock Outlook - A Tale of Two Markets: 7 November 2019 - SingaporeNhân Trương VănОценок пока нет

- Zinc ProductionДокумент4 страницыZinc ProductionRunkitoОценок пока нет

- Direct Reduction and Smelting ProcessesДокумент40 страницDirect Reduction and Smelting ProcessesAfza NurhakimОценок пока нет

- Cracking The Bottom of The Barrel With MIDAS Technology: Number 104 Fall 2008Документ24 страницыCracking The Bottom of The Barrel With MIDAS Technology: Number 104 Fall 2008deepakattavarОценок пока нет

- CMAI - Paul Blanchard - Nylon ABS Review 5.12Документ42 страницыCMAI - Paul Blanchard - Nylon ABS Review 5.12tiwarivivek2Оценок пока нет

- Refineria de Cartagena (Reficar) Refinery Expansion - Hydrocarbons TechnologyДокумент3 страницыRefineria de Cartagena (Reficar) Refinery Expansion - Hydrocarbons TechnologyGjorgeluisОценок пока нет

- Graphite OutlookДокумент21 страницаGraphite OutlookMasna PrudhviОценок пока нет

- Coal Macerals AssamДокумент5 страницCoal Macerals AssamRabisankar KarmakarОценок пока нет

- EURACOAL Market Report 2015 1 PDFДокумент21 страницаEURACOAL Market Report 2015 1 PDFRamo KissОценок пока нет

- Steel Industries Problem by Amitab - MudgalДокумент22 страницыSteel Industries Problem by Amitab - MudgalRavinder Singh PadamОценок пока нет

- Saudi Arabia's Mineral Industry in 2014Документ12 страницSaudi Arabia's Mineral Industry in 2014red reddОценок пока нет

- Marketsurvey LeadandzincДокумент299 страницMarketsurvey LeadandzincNitisha RathoreОценок пока нет

- Cold Light Up Operational ChecklistДокумент10 страницCold Light Up Operational ChecklistIEPL BELAОценок пока нет

- 3 Goshu 3Документ18 страниц3 Goshu 3nega cheruОценок пока нет

- 2013 - S2E Technical and Technological - Intro - Final PDFДокумент28 страниц2013 - S2E Technical and Technological - Intro - Final PDFJose Kirby100% (1)

- Siemens SSA31.04 PDFДокумент6 страницSiemens SSA31.04 PDFJohn DunbarОценок пока нет

- Aluminum Electrolytic Capacitors Aluminum Electrolytic CapacitorsДокумент6 страницAluminum Electrolytic Capacitors Aluminum Electrolytic CapacitorsAvs ElectronОценок пока нет

- Analysis and Modeling of Interharmonics From Grid-Connected Photovoltaic Systems.Документ12 страницAnalysis and Modeling of Interharmonics From Grid-Connected Photovoltaic Systems.Abdul Qayyum AliОценок пока нет

- Pump Inlet Piping DesignДокумент2 страницыPump Inlet Piping DesignWayaya WaziwupyaОценок пока нет

- Cit Asci tr334 PDFДокумент18 страницCit Asci tr334 PDFraguerreОценок пока нет

- Sennheiser Digital 9000 System Manual 2017 ENДокумент126 страницSennheiser Digital 9000 System Manual 2017 ENAnder AОценок пока нет

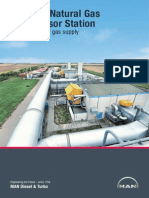

- Compressor Station MallnowДокумент8 страницCompressor Station MallnowMANIU RADU-GEORGIANОценок пока нет

- Advances in Graphene Based Semiconductor Photocatalysts For Solar Energy ConversionДокумент27 страницAdvances in Graphene Based Semiconductor Photocatalysts For Solar Energy ConversiondevОценок пока нет

- Building Services AssignmentДокумент19 страницBuilding Services AssignmentRoushell KhanОценок пока нет

- Busway SpecificationДокумент6 страницBusway SpecificationNATHANОценок пока нет

- Preparation Before Storage of Aviation BatteriesДокумент1 страницаPreparation Before Storage of Aviation BatteriesRaymond ZamoraОценок пока нет

- VCO Based ADCДокумент3 страницыVCO Based ADCBlake PayriceОценок пока нет

- KD Engine Specs and Systems GuideДокумент72 страницыKD Engine Specs and Systems Guidemoises valenzuela janampaОценок пока нет

- About The AuthorsДокумент1 страницаAbout The AuthorsArthur CostaОценок пока нет

- Nseallcompanies 31122020Документ78 страницNseallcompanies 31122020guy fawkesОценок пока нет

- AD534Документ12 страницAD534Vaibhav GaurОценок пока нет

- Electrical Components 2Документ9 страницElectrical Components 2Mark Emerson BernabeОценок пока нет

- Sebp4195 76 01 Allcd - 003 PDFДокумент965 страницSebp4195 76 01 Allcd - 003 PDFFacturas hidrodieselОценок пока нет

- Radiography Sai KripaДокумент4 страницыRadiography Sai KripaSarthak EnterprisesОценок пока нет

- Introduction To Batteries - BatteryДокумент17 страницIntroduction To Batteries - BatteryJ dixojoОценок пока нет

- Miroljub Todorović - ApeironДокумент25 страницMiroljub Todorović - Apeiron"Mycelium" samizdat publishersОценок пока нет

- User Manual: T6DBG721N T6DBG720NДокумент26 страницUser Manual: T6DBG721N T6DBG720NViorica TrohinОценок пока нет

- Geo 2002Документ24 страницыGeo 2002Jennifer WatsonОценок пока нет

- Surge TankДокумент2 страницыSurge TankBilel MarkosОценок пока нет

- Project Report - TarunДокумент5 страницProject Report - TarunrajuОценок пока нет

- Window U-Value ModuleДокумент46 страницWindow U-Value ModuleSze Yan LamОценок пока нет

- Marine Propulsion Engines GuideДокумент20 страницMarine Propulsion Engines GuideyoungfpОценок пока нет