Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Final PPT UmppДокумент13 страницFinal PPT UmppDhritiman PanigrahiОценок пока нет

- Nas DataДокумент1 страницаNas Datavenugopalreddy.vootuОценок пока нет

- Decontrol Further - The Indian ExpressДокумент2 страницыDecontrol Further - The Indian Expressvenugopalreddy.vootuОценок пока нет

- NasData PUBLICATIONS THETIMESOFINDIA DELHI 2014-12-17 PagePrint 17-12-2014 026Документ1 страницаNasData PUBLICATIONS THETIMESOFINDIA DELHI 2014-12-17 PagePrint 17-12-2014 026venugopalreddy.vootuОценок пока нет

- Lesson 10 - Religious Reform Movements in Modern India (82 KB) PDFДокумент15 страницLesson 10 - Religious Reform Movements in Modern India (82 KB) PDFharsh.nsit2007752100% (1)

- Idioms AllДокумент23 страницыIdioms AllJitendra SharmaОценок пока нет

- 25 Ethics Case Study For IAS Mains 2014 by S. K. Mishra, IAS (Retd PDFДокумент21 страница25 Ethics Case Study For IAS Mains 2014 by S. K. Mishra, IAS (Retd PDFvenugopalreddy.vootu100% (1)

- Decontrol Further - The Indian ExpressДокумент2 страницыDecontrol Further - The Indian Expressvenugopalreddy.vootuОценок пока нет

- Decontrol Further - The Indian ExpressДокумент2 страницыDecontrol Further - The Indian Expressvenugopalreddy.vootuОценок пока нет

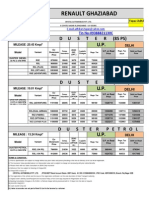

- Duster Price List-AugustДокумент6 страницDuster Price List-Augustvenugopalreddy.vootuОценок пока нет

- Direction Book List For IAS ExamsДокумент6 страницDirection Book List For IAS Examsvenugopalreddy.vootuОценок пока нет

- Biodiesel - Wikipedia, The Free EncyclopediaДокумент31 страницаBiodiesel - Wikipedia, The Free Encyclopediavenugopalreddy.vootuОценок пока нет

- Geothermal Energy - Indian Power SectorДокумент10 страницGeothermal Energy - Indian Power Sectorvenugopalreddy.vootuОценок пока нет

- BIOFUELS - National Policy Analyis FINALДокумент19 страницBIOFUELS - National Policy Analyis FINALvenugopalreddy.vootuОценок пока нет

- Critically Endangered Animal Species of India PDFДокумент26 страницCritically Endangered Animal Species of India PDFUtkarsh RajОценок пока нет

- Fundamentals of Human GeographyДокумент113 страницFundamentals of Human Geographyvenugopalreddy.vootuОценок пока нет

- Annual Report 2015Документ234 страницыAnnual Report 2015roshansm1978Оценок пока нет

- Competitive Bidding Review PrayasДокумент67 страницCompetitive Bidding Review PrayasBharath VijayОценок пока нет

- Project Appraisal of Power Project-A Case of Private Sector UtilityДокумент65 страницProject Appraisal of Power Project-A Case of Private Sector Utilityvineet sarawagi50% (2)

- 03-4000mw Mundra Ultra Mega Power Project Brief Overview-BrrangaswamyДокумент23 страницы03-4000mw Mundra Ultra Mega Power Project Brief Overview-BrrangaswamyPrashant PatilОценок пока нет

- Annual Report (2007-08) - Ministry of PowerДокумент204 страницыAnnual Report (2007-08) - Ministry of Powerabhikdb100% (1)

- Ultra Mega Thermal Power PlantДокумент10 страницUltra Mega Thermal Power PlantAshish VermaОценок пока нет

- Umpp Greener Future121015 PDFДокумент68 страницUmpp Greener Future121015 PDFMohan KrishnaОценок пока нет

- Ultra Mega Power ProjectДокумент5 страницUltra Mega Power ProjectAmit SharmaОценок пока нет

- Government of India Ministry of Power Ultra Mega Power Projects 1. BackgroundДокумент7 страницGovernment of India Ministry of Power Ultra Mega Power Projects 1. BackgroundsudehelyRОценок пока нет

- Case Analysis-Sasan Power LTDДокумент19 страницCase Analysis-Sasan Power LTDpranjaligОценок пока нет