Вам также может понравиться

- Satvik-Predictve Analytics Deck - v2Документ52 страницыSatvik-Predictve Analytics Deck - v2curlin13Оценок пока нет

- 36 Questions To Answer: The Essentials of A Documented Content Marketing StrategyДокумент16 страниц36 Questions To Answer: The Essentials of A Documented Content Marketing StrategySilvia Beatle SnapeОценок пока нет

- GlobalData Keytrendsinculinarytourism 130918-1Документ24 страницыGlobalData Keytrendsinculinarytourism 130918-1raisincookiesОценок пока нет

- ATB Entrepreneur's Edge: Bronze, Silver and Gold-Three Levels of M&A AdvisorsДокумент4 страницыATB Entrepreneur's Edge: Bronze, Silver and Gold-Three Levels of M&A AdvisorsAli Gokhan KocanОценок пока нет

- Store PlanningДокумент12 страницStore PlanningGladwin JosephОценок пока нет

- Implementing The Account and Financial Dimensions Framework AX2012Документ43 страницыImplementing The Account and Financial Dimensions Framework AX2012Sky Boon Kok LeongОценок пока нет

- 1B.+SaaS+Marketing+Playbook+2021+ +Part+BДокумент33 страницы1B.+SaaS+Marketing+Playbook+2021+ +Part+BVivek BandebucheОценок пока нет

- Bridging The Gap Between Social Media and Behavioral Brand LoyaltyДокумент11 страницBridging The Gap Between Social Media and Behavioral Brand LoyaltyJp GingoyonОценок пока нет

- Company Profile 2011Документ28 страницCompany Profile 2011najibjaafarОценок пока нет

- Business Strategy - Part 1 and 2Документ34 страницыBusiness Strategy - Part 1 and 2cinderella69Оценок пока нет

- 3 Ways To Improve Excel Data IntegrityДокумент2 страницы3 Ways To Improve Excel Data IntegrityJacinto Gomez EmbolettiОценок пока нет

- Cheese Concentrate MarketДокумент12 страницCheese Concentrate MarketNamrataОценок пока нет

- Building Balanced Scorecard Strategy MapsДокумент18 страницBuilding Balanced Scorecard Strategy MapsRaviram NaiduОценок пока нет

- Service Blueprint TemplateДокумент24 страницыService Blueprint TemplateJosueОценок пока нет

- RFP Competition Ryker Proposal Boston Team 3 Final Version - 1Документ49 страницRFP Competition Ryker Proposal Boston Team 3 Final Version - 1mananoffical100% (1)

- The It Leader'S Checklist For Saas OperationsДокумент19 страницThe It Leader'S Checklist For Saas OperationsfreshmilkОценок пока нет

- Competitor AnalysisДокумент4 страницыCompetitor AnalysisAnmol GoyalОценок пока нет

- Fourth Cut CPGДокумент102 страницыFourth Cut CPGIsha SharmaОценок пока нет

- Standing Operating Procedure-FinalДокумент5 страницStanding Operating Procedure-FinalRaheel KhanОценок пока нет

- BCG RAI - Retail Resurgence in India-Leading in The New Reality (Feb 2021)Документ66 страницBCG RAI - Retail Resurgence in India-Leading in The New Reality (Feb 2021)Aadhar Bhardwaj100% (1)

- SYY Sysco 2018 Jefferies PresentationДокумент27 страницSYY Sysco 2018 Jefferies PresentationAla BasterОценок пока нет

- Loyalty ApproachДокумент22 страницыLoyalty Approachlogan143Оценок пока нет

- Dexlab OnePageДокумент1 страницаDexlab OnePageAlessio SorrentoОценок пока нет

- Co Profile PT - Candramawa PDFДокумент12 страницCo Profile PT - Candramawa PDFDede KendorОценок пока нет

- 2016 Customer Engagement ResearchДокумент14 страниц2016 Customer Engagement ResearchIDG_World100% (1)

- The Change Trifecta: Measuring ROI To Maximize Change EffectivenessДокумент12 страницThe Change Trifecta: Measuring ROI To Maximize Change EffectivenessHernanОценок пока нет

- Analytics in Action - How Marketelligent Helped A Beverage Manufacturer Better Its Production PlanningДокумент2 страницыAnalytics in Action - How Marketelligent Helped A Beverage Manufacturer Better Its Production PlanningMarketelligentОценок пока нет

- CFA Level I Three-Month Study PlanДокумент9 страницCFA Level I Three-Month Study Plansashavlad100% (1)

- MERCEDES AMG PETRONAS Formula One Team Invites Fans To Develop New Virtual Reality Solutions To Speed Up Collaboration Between Trackside and Team HQ (Company Update)Документ3 страницыMERCEDES AMG PETRONAS Formula One Team Invites Fans To Develop New Virtual Reality Solutions To Speed Up Collaboration Between Trackside and Team HQ (Company Update)Shyam SunderОценок пока нет

- Pestle Analysis QSRДокумент3 страницыPestle Analysis QSRJoshua RushОценок пока нет

- WP Impact of Strategic Simulation On Product ProfitabilityДокумент6 страницWP Impact of Strategic Simulation On Product ProfitabilitymcruzalvОценок пока нет

- 4 Brands Making Customer Loyalty Programs Work - Customer Engagement, Brand Strategy, Customer Loyalty Programs - CFO WorldДокумент4 страницы4 Brands Making Customer Loyalty Programs Work - Customer Engagement, Brand Strategy, Customer Loyalty Programs - CFO Worldsubashreeskm2836Оценок пока нет

- Market Segmentation and Segmentation StrategiesДокумент19 страницMarket Segmentation and Segmentation StrategiesfarazsaifОценок пока нет

- Uality Customer Management: Loyalty Program T C " U Š Ć E "Документ8 страницUality Customer Management: Loyalty Program T C " U Š Ć E "Rohit MishraОценок пока нет

- Kruze SaaS Fin Model v1Документ66 страницKruze SaaS Fin Model v1IskОценок пока нет

- Summary Business AnalyticsДокумент24 страницыSummary Business AnalyticsLUIGIAОценок пока нет

- Demand Creation Five Metrics That MatterДокумент2 страницыDemand Creation Five Metrics That MatterIan GoldsmidОценок пока нет

- Metamorphosis Campaign Book - Buffalo Wild WingsДокумент52 страницыMetamorphosis Campaign Book - Buffalo Wild WingsMichelle KammermanОценок пока нет

- Loyalty ProgramsДокумент22 страницыLoyalty ProgramsKhawaja_Mahed__3244Оценок пока нет

- New Product Launches:: Success Principles and In-Store ExecutionДокумент12 страницNew Product Launches:: Success Principles and In-Store ExecutionShravan Kumar100% (1)

- Microsoft Dynamics: Presented by - Deepak.JДокумент20 страницMicrosoft Dynamics: Presented by - Deepak.JDeepak Prakash JayaОценок пока нет

- An Innovative Step in Loyalty programs-LOYESYSДокумент18 страницAn Innovative Step in Loyalty programs-LOYESYSJason MullerОценок пока нет

- ERP Buyer's Guide: Top Vendors ReviewedДокумент8 страницERP Buyer's Guide: Top Vendors ReviewedravsachОценок пока нет

- Tesco Case StudyДокумент15 страницTesco Case StudySherene DharshineeОценок пока нет

- How To Make SME Segment ProfitableДокумент35 страницHow To Make SME Segment ProfitableTariq HasanОценок пока нет

- CPG Loyalty FinalДокумент13 страницCPG Loyalty FinalpuneetdubeyОценок пока нет

- Pricing Fit-Gap AnalysisДокумент42 страницыPricing Fit-Gap AnalysisSri Nithya AmritanandaОценок пока нет

- Cheat Sheet MarketingДокумент3 страницыCheat Sheet MarketingCharlotte GillandersОценок пока нет

- Solution Offerings For Retail Industry RCTG ReportДокумент11 страницSolution Offerings For Retail Industry RCTG ReportSurendra Kumar NОценок пока нет

- Mckinsey LoyaltyДокумент4 страницыMckinsey LoyaltyVikram KharviОценок пока нет

- Is Loyalty Program As A Marketing Tool Effective?: Ms. Nisha Nandal, Dr. Naveen Nandal, Dr. Ritika MalikДокумент4 страницыIs Loyalty Program As A Marketing Tool Effective?: Ms. Nisha Nandal, Dr. Naveen Nandal, Dr. Ritika Malikiyah589Оценок пока нет

- View On Cognizant StrategyДокумент30 страницView On Cognizant Strategysiddarthaprasad587100% (1)

- Small Business Budget Template PDFДокумент6 страницSmall Business Budget Template PDFVeasna NounОценок пока нет

- Starbucks Business Report ManagementДокумент21 страницаStarbucks Business Report ManagementParidhi LapalikarОценок пока нет

- Qutiq Company ProfileДокумент8 страницQutiq Company Profilemars deejayОценок пока нет

- Loyalty & Co Branding: Bank Card & Epayment 2005 26 October 2005Документ22 страницыLoyalty & Co Branding: Bank Card & Epayment 2005 26 October 2005sdj32Оценок пока нет

- Pharmacy Closing ChecklistДокумент43 страницыPharmacy Closing ChecklistRedeye AsiaОценок пока нет

- Analytics For Cash Advance Industry - MarketelligentДокумент2 страницыAnalytics For Cash Advance Industry - MarketelligentMarketelligentОценок пока нет

- 10 Step Guide To Creating A Loyalty Program PDFДокумент35 страниц10 Step Guide To Creating A Loyalty Program PDFFranco BressanОценок пока нет

- Analytics in Action - How Marketelligent Helped Increase Customer Engagement Via Targeted Cross-SellДокумент2 страницыAnalytics in Action - How Marketelligent Helped Increase Customer Engagement Via Targeted Cross-SellMarketelligentОценок пока нет

- Analytics in Action - How Marketelligent Helped An Online Remittance Firm Identify Risky TransactionsДокумент2 страницыAnalytics in Action - How Marketelligent Helped An Online Remittance Firm Identify Risky TransactionsMarketelligentОценок пока нет

- Application of Business Sciences To Solve Business Problems - MarketelligentДокумент17 страницApplication of Business Sciences To Solve Business Problems - MarketelligentMarketelligentОценок пока нет

- Analytics in Action - How Marketelligent Helped A Quick Service Restaurant Chain Identify Customer Pain PointsДокумент2 страницыAnalytics in Action - How Marketelligent Helped A Quick Service Restaurant Chain Identify Customer Pain PointsMarketelligentОценок пока нет

- Analytics in Action - How Marketelligent Helped A US Manufacturer Improve Demand ForecastsДокумент2 страницыAnalytics in Action - How Marketelligent Helped A US Manufacturer Improve Demand ForecastsMarketelligentОценок пока нет

- Analytics in Action - How Marketelligent Helped A Petroleum Retailer Identify 'At Risk' CustomersДокумент2 страницыAnalytics in Action - How Marketelligent Helped A Petroleum Retailer Identify 'At Risk' CustomersMarketelligentОценок пока нет

- Analytics in Action - How Marketelligent Helped A Retailer Rationalize SKU'sДокумент2 страницыAnalytics in Action - How Marketelligent Helped A Retailer Rationalize SKU'sMarketelligentОценок пока нет

- Analytics in Action - How Marketelligent Helped A Beverage Manufacturer Better Its Production PlanningДокумент2 страницыAnalytics in Action - How Marketelligent Helped A Beverage Manufacturer Better Its Production PlanningMarketelligentОценок пока нет

- Analytics in Action - How Marketelligent Helped A CPG Company Boost Store Order ValueДокумент2 страницыAnalytics in Action - How Marketelligent Helped A CPG Company Boost Store Order ValueMarketelligentОценок пока нет

- Analytics in Action - How Marketelligent Helped A Publishing House Identify Its Social InfluencersДокумент2 страницыAnalytics in Action - How Marketelligent Helped A Publishing House Identify Its Social InfluencersMarketelligentОценок пока нет

- Analytics in Action - How Marketelligent Helped A CPG Company Optimize Its Media PlanningДокумент2 страницыAnalytics in Action - How Marketelligent Helped A CPG Company Optimize Its Media PlanningMarketelligentОценок пока нет

- Analytics in Action - How Marketelligent Helped A Bank Validate A Predictive ModelДокумент2 страницыAnalytics in Action - How Marketelligent Helped A Bank Validate A Predictive ModelMarketelligentОценок пока нет

- Analytics For Retail Banking - MarketelligentДокумент2 страницыAnalytics For Retail Banking - MarketelligentMarketelligent100% (1)

- Analytics Solutions For Retail Banking - MarketelligentДокумент25 страницAnalytics Solutions For Retail Banking - MarketelligentMarketelligentОценок пока нет

- Application of Decision Sciences To Solve Business Problems in The Consumer Packaged Goods (CPG) IndustryДокумент24 страницыApplication of Decision Sciences To Solve Business Problems in The Consumer Packaged Goods (CPG) IndustryMarketelligentОценок пока нет

- Analytics in Action - How Marketelligent Helped A B2B Retailer Increase Its Lead VelocityДокумент2 страницыAnalytics in Action - How Marketelligent Helped A B2B Retailer Increase Its Lead VelocityMarketelligentОценок пока нет

- Analytics in Action - How Marketelligent Helped A Manufacturer Optimize Trade Promotion SpendsДокумент2 страницыAnalytics in Action - How Marketelligent Helped A Manufacturer Optimize Trade Promotion SpendsMarketelligentОценок пока нет

- Trade Promotion Optimization - MarketelligentДокумент12 страницTrade Promotion Optimization - MarketelligentMarketelligentОценок пока нет

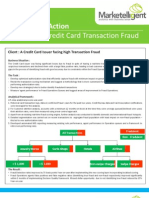

- Analytics in Action - How Marketelligent Helped A Card Issuer Combat Transaction FraudДокумент2 страницыAnalytics in Action - How Marketelligent Helped A Card Issuer Combat Transaction FraudMarketelligentОценок пока нет

- Analytics For Cash Advance Industry - MarketelligentДокумент2 страницыAnalytics For Cash Advance Industry - MarketelligentMarketelligentОценок пока нет

- CRM Analytics - MarketelligentДокумент2 страницыCRM Analytics - MarketelligentMarketelligentОценок пока нет

- CPG Analytics - MarketelligentДокумент2 страницыCPG Analytics - MarketelligentMarketelligent100% (3)

- Instructions: Reflect On The Topics That Were Previously Discussed. Write at Least Three (3) Things Per TopicДокумент2 страницыInstructions: Reflect On The Topics That Were Previously Discussed. Write at Least Three (3) Things Per TopicGuevarra KeithОценок пока нет

- 2501 Mathematics Paper+with+solution EveningДокумент10 страниц2501 Mathematics Paper+with+solution EveningNenavath GaneshОценок пока нет

- Syllabus For B.A. (Philosophy) Semester-Wise Titles of The Papers in BA (Philosophy)Документ26 страницSyllabus For B.A. (Philosophy) Semester-Wise Titles of The Papers in BA (Philosophy)Ayan AhmadОценок пока нет

- The Biofloc Technology (BFT) Water Quality, Biofloc Composition, and GrowthДокумент8 страницThe Biofloc Technology (BFT) Water Quality, Biofloc Composition, and GrowthHafez MabroukОценок пока нет

- Cambridge English Key Sample Paper 1 Reading and Writing v2Документ9 страницCambridge English Key Sample Paper 1 Reading and Writing v2kalinguer100% (1)

- Public Service Media in The Networked Society Ripe 2017 PDFДокумент270 страницPublic Service Media in The Networked Society Ripe 2017 PDFTriszt Tviszt KapitányОценок пока нет

- Data Science Online Workshop Data Science vs. Data AnalyticsДокумент1 страницаData Science Online Workshop Data Science vs. Data AnalyticsGaurav VarshneyОценок пока нет

- Rosenberg Et Al - Through Interpreters' Eyes, Comparing Roles of Professional and Family InterpretersДокумент7 страницRosenberg Et Al - Through Interpreters' Eyes, Comparing Roles of Professional and Family InterpretersMaria AguilarОценок пока нет

- Birds (Aves) Are A Group Of: WingsДокумент1 страницаBirds (Aves) Are A Group Of: WingsGabriel Angelo AbrauОценок пока нет

- Shrek FSCДокумент5 страницShrek FSCMafer CastroОценок пока нет

- Directions: Choose The Best Answer For Each Multiple Choice Question. Write The Best Answer On The BlankДокумент2 страницыDirections: Choose The Best Answer For Each Multiple Choice Question. Write The Best Answer On The BlankRanulfo MayolОценок пока нет

- Risteski Space and Boundaries Between The WorldsДокумент9 страницRisteski Space and Boundaries Between The WorldsakunjinОценок пока нет

- Physics - TRIAL S1, STPM 2022 - CoverДокумент1 страницаPhysics - TRIAL S1, STPM 2022 - CoverbenОценок пока нет

- Zimbabwe Mag Court Rules Commentary Si 11 of 2019Документ6 страницZimbabwe Mag Court Rules Commentary Si 11 of 2019Vusi BhebheОценок пока нет

- Form No. 10-I: Certificate of Prescribed Authority For The Purposes of Section 80DDBДокумент1 страницаForm No. 10-I: Certificate of Prescribed Authority For The Purposes of Section 80DDBIam KarthikeyanОценок пока нет

- EELE 202 Lab 6 AC Nodal and Mesh Analysis s14Документ8 страницEELE 202 Lab 6 AC Nodal and Mesh Analysis s14Nayr JTОценок пока нет

- Acfrogb0i3jalza4d2cm33ab0kjvfqevdmmcia - Kifkmf7zqew8tpk3ef Iav8r9j0ys0ekwrl4a8k7yqd0pqdr9qk1cpmjq Xx5x6kxzc8uq9it Zno Fwdrmyo98jelpvjb-9ahfdekf3cqptДокумент1 страницаAcfrogb0i3jalza4d2cm33ab0kjvfqevdmmcia - Kifkmf7zqew8tpk3ef Iav8r9j0ys0ekwrl4a8k7yqd0pqdr9qk1cpmjq Xx5x6kxzc8uq9it Zno Fwdrmyo98jelpvjb-9ahfdekf3cqptbbОценок пока нет

- 2022 Drik Panchang Hindu FestivalsДокумент11 страниц2022 Drik Panchang Hindu FestivalsBikash KumarОценок пока нет

- Invitation 2023Документ10 страницInvitation 2023Joanna Marie Cruz FelipeОценок пока нет

- Payment Billing System DocumentДокумент65 страницPayment Billing System Documentshankar_718571% (7)

- 2019 Ulverstone Show ResultsДокумент10 страниц2019 Ulverstone Show ResultsMegan PowellОценок пока нет

- Bab 3 - Soal-Soal No. 4 SD 10Документ4 страницыBab 3 - Soal-Soal No. 4 SD 10Vanni LimОценок пока нет

- Esse 3600Документ15 страницEsse 3600api-324911878100% (1)

- Booklet - Frantic Assembly Beautiful BurnoutДокумент10 страницBooklet - Frantic Assembly Beautiful BurnoutMinnie'xoОценок пока нет

- Chapter 8 - FluidДокумент26 страницChapter 8 - FluidMuhammad Aminnur Hasmin B. HasminОценок пока нет

- Facilitation TheoryДокумент2 страницыFacilitation TheoryYessamin Valerie PergisОценок пока нет

- TypeFinderReport ENFPДокумент10 страницTypeFinderReport ENFPBassant AdelОценок пока нет

- India: SupplyДокумент6 страницIndia: SupplyHarish NathanОценок пока нет

- A New Cloud Computing Governance Framework PDFДокумент8 страницA New Cloud Computing Governance Framework PDFMustafa Al HassanОценок пока нет

- Delaware Met CSAC Initial Meeting ReportДокумент20 страницDelaware Met CSAC Initial Meeting ReportKevinOhlandtОценок пока нет