Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Auditing Notes - Chapter 3Документ24 страницыAuditing Notes - Chapter 3Future CPA100% (7)

- Solutions To Problems: Pe On Estate TaxДокумент11 страницSolutions To Problems: Pe On Estate TaxErica NicolasuraОценок пока нет

- Your Payment Receipt PDFДокумент1 страницаYour Payment Receipt PDFoiciruaОценок пока нет

- Cisa NotesДокумент2 страницыCisa Notesesskae59mОценок пока нет

- Christopher Verizon BillДокумент4 страницыChristopher Verizon BillSharon Jones100% (2)

- UNIT II Tax RemediesДокумент17 страницUNIT II Tax RemediesAl BertОценок пока нет

- CIR Vs AlgueДокумент1 страницаCIR Vs AlgueJolas E. BrutasОценок пока нет

- Network Security TutorialДокумент15 страницNetwork Security TutorialArmaan Singh ChawlaОценок пока нет

- HQ03 - 6th BATCH - General Principles of Income TaxationДокумент13 страницHQ03 - 6th BATCH - General Principles of Income TaxationJimmyChaoОценок пока нет

- Domain 1Документ3 страницыDomain 1esskae59mОценок пока нет

- 478 613Документ8 страниц478 613Fahad AliОценок пока нет

- 12v1 Database BackupДокумент6 страниц12v1 Database Backupnarasi64Оценок пока нет

- Stock BasisДокумент3 страницыStock Basisesskae59mОценок пока нет

- Corp-Tax Rosenberg s05Документ32 страницыCorp-Tax Rosenberg s05stonecerberusОценок пока нет

- Excise Taxes Are Imposed Upon The Transfer of Goods and Services and Based On The ValueДокумент1 страницаExcise Taxes Are Imposed Upon The Transfer of Goods and Services and Based On The Valueesskae59mОценок пока нет

- Dividends Received Deduction: 0% - 19% 70% 20% - 79% 80% 80% or More 100%Документ2 страницыDividends Received Deduction: 0% - 19% 70% 20% - 79% 80% 80% or More 100%esskae59mОценок пока нет

- Excise Taxes Are Imposed Upon The Transfer of Goods and Services and Based On The ValueДокумент1 страницаExcise Taxes Are Imposed Upon The Transfer of Goods and Services and Based On The Valueesskae59mОценок пока нет

- ItemizedДокумент1 страницаItemizedesskae59mОценок пока нет

- AMT TaxationДокумент1 страницаAMT Taxationesskae59mОценок пока нет

- Kunezle & StreiffДокумент3 страницыKunezle & StreiffJanna Robles SantosОценок пока нет

- Tally: Chap-1:-Company Creation & Deletation Create CompanyДокумент32 страницыTally: Chap-1:-Company Creation & Deletation Create CompanysananathaniОценок пока нет

- Form MTR 6 CSTДокумент1 страницаForm MTR 6 CSTca_kamalОценок пока нет

- Authorization For Credit Card Transactions: U.S. Citizenship and Immigration ServicesДокумент1 страницаAuthorization For Credit Card Transactions: U.S. Citizenship and Immigration ServicesDIEGO BUSTOSОценок пока нет

- Plastic Money Full Project Copy ARNABДокумент41 страницаPlastic Money Full Project Copy ARNABarnab_b8767% (3)

- Accumulated Depreciation: EquipmentДокумент9 страницAccumulated Depreciation: EquipmentAndrewVazОценок пока нет

- Application For Registration: Republic of The Philippines Department of Finance Bureau of Internal Revenue BIR Form NoДокумент2 страницыApplication For Registration: Republic of The Philippines Department of Finance Bureau of Internal Revenue BIR Form NoehrgsdОценок пока нет

- SarikaДокумент55 страницSarikaStella PaulОценок пока нет

- Amerbran CompanyДокумент1 страницаAmerbran CompanyJalad Mukerjee100% (1)

- 1706Документ2 страницы1706May Chan Cuyos100% (1)

- Natural Care Service Package (NCSP) Agreement: Cuckoo International (B) SDN BHDДокумент1 страницаNatural Care Service Package (NCSP) Agreement: Cuckoo International (B) SDN BHDWesdi DОценок пока нет

- Evidence: The Detail of Source of Income Has Been Mentioned in TheДокумент2 страницыEvidence: The Detail of Source of Income Has Been Mentioned in TheDrone TewatiaОценок пока нет

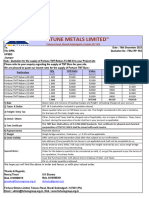

- "Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301Документ1 страница"Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301S K SharmaОценок пока нет

- Instructor's Manual - Vol. 1 - Solutions To Appendix E Tax Cases - 2011Документ48 страницInstructor's Manual - Vol. 1 - Solutions To Appendix E Tax Cases - 2011Heather Green100% (1)

- Ride Details Bill Details: Thanks For Travelling With Us, GautamengineeringcompanyДокумент3 страницыRide Details Bill Details: Thanks For Travelling With Us, Gautamengineeringcompanyanon_523618295Оценок пока нет

- Fee Structure 7Документ1 страницаFee Structure 7ABHISHEKОценок пока нет

- 23 UgsthbДокумент84 страницы23 UgsthbChawla DimpleОценок пока нет

- Tally TestДокумент2 страницыTally Testsathish kumarОценок пока нет

- TAX 1601 Answers Additions To TaxДокумент4 страницыTAX 1601 Answers Additions To TaxAlrahjie AnsariОценок пока нет

- Income Taxation - Regular Income Tax 2Документ5 страницIncome Taxation - Regular Income Tax 2Drew BanlutaОценок пока нет

- Balance - Sheet 1119Документ2 страницыBalance - Sheet 1119BASKOROОценок пока нет

- HBL Id (Key Fact Sheet) - Jul - Dec 2020 PDFДокумент1 страницаHBL Id (Key Fact Sheet) - Jul - Dec 2020 PDFAli ShahОценок пока нет

- In A NutshellДокумент3 страницыIn A NutshellJane TuazonОценок пока нет

- Wealth Management PPT FinalДокумент42 страницыWealth Management PPT FinalCyvita VeigasОценок пока нет