Вам также может понравиться

- Business Plan TemplateДокумент26 страницBusiness Plan TemplateUmAr FArooqОценок пока нет

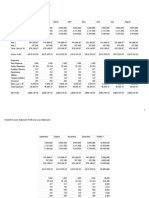

- 12-Month Income Statement Profit-And-Loss Statement - Sheet1Документ2 страницы12-Month Income Statement Profit-And-Loss Statement - Sheet1api-462952636100% (1)

- An MBA in a Book: Everything You Need to Know to Master Business - In One Book!От EverandAn MBA in a Book: Everything You Need to Know to Master Business - In One Book!Оценок пока нет

- How Time Value of Money Affects Investments and Financial Decisions in Financial Minagement.Документ28 страницHow Time Value of Money Affects Investments and Financial Decisions in Financial Minagement.Ishtiaq Ahmed82% (11)

- Financial Risk Management: A Simple IntroductionОт EverandFinancial Risk Management: A Simple IntroductionРейтинг: 4.5 из 5 звезд4.5/5 (7)

- About Warren BuffetДокумент14 страницAbout Warren BuffetPadregarcia Mps100% (1)

- Cost Accounting (Chapter 1-3)Документ5 страницCost Accounting (Chapter 1-3)eunice0% (1)

- Applied Corporate Finance. What is a Company worth?От EverandApplied Corporate Finance. What is a Company worth?Рейтинг: 3 из 5 звезд3/5 (2)

- Finman Modules Chapter 5Документ9 страницFinman Modules Chapter 5Angel ColarteОценок пока нет

- Practice Exercises # 2 - CH 14Документ4 страницыPractice Exercises # 2 - CH 14Hamna AzeezОценок пока нет

- Time Value of Money ConceptsДокумент19 страницTime Value of Money Conceptsjohnnyboy30003223Оценок пока нет

- Stocks and BondsДокумент28 страницStocks and BondsPrincess Macariola100% (1)

- Stéphane Grappelli - Wikipedia, The Free EncyclopediaДокумент8 страницStéphane Grappelli - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Financial Management - The Time Value of MoneyДокумент29 страницFinancial Management - The Time Value of MoneySoledad PerezОценок пока нет

- Aqa Gcse Economics SpecificationДокумент27 страницAqa Gcse Economics SpecificationastargroupОценок пока нет

- Time Value of MoneyДокумент18 страницTime Value of MoneyJunaid SubhaniОценок пока нет

- Amway Business Plan STP by Mandeep Kaur and Kulwinder SinghДокумент22 страницыAmway Business Plan STP by Mandeep Kaur and Kulwinder SinghKulwinder SinghОценок пока нет

- Time Value of MoneyДокумент18 страницTime Value of MoneyAlston PereiraОценок пока нет

- Present Value Formula ExplainedДокумент9 страницPresent Value Formula ExplainedChabelita SantillanОценок пока нет

- Time ValueДокумент9 страницTime Valuemohanraokp2279Оценок пока нет

- 304A Financial Management and Decision MakingДокумент67 страниц304A Financial Management and Decision MakingSam SamОценок пока нет

- Formula For The Amount of An Ordinary AnnuityДокумент3 страницыFormula For The Amount of An Ordinary AnnuityAbbyОценок пока нет

- Time Value of MoneyДокумент21 страницаTime Value of MoneyAkshay MestryОценок пока нет

- NOTES ON TIME VALUE OF MONEYДокумент10 страницNOTES ON TIME VALUE OF MONEYFariya HossainОценок пока нет

- PV of cash flows formulaДокумент3 страницыPV of cash flows formulaAditya GuptaОценок пока нет

- Time Value of MoneyДокумент4 страницыTime Value of Moneyshiva ranjaniОценок пока нет

- Discounted Cash Flows and Valuation Learning ObjectivesДокумент74 страницыDiscounted Cash Flows and Valuation Learning ObjectivesAmbrish (gYpr.in)Оценок пока нет

- Engineering EconomyДокумент96 страницEngineering EconomyHinata UzumakiОценок пока нет

- DHA-BHI-404 - Unit4 - Time Value of MoneyДокумент17 страницDHA-BHI-404 - Unit4 - Time Value of MoneyFë LïçïäОценок пока нет

- Present Value 1Документ7 страницPresent Value 1shotejОценок пока нет

- Present Value Chapter 3 SolutionsДокумент7 страницPresent Value Chapter 3 SolutionsJonavie Lamoste HubahibОценок пока нет

- Malinab Aira Bsba FM 2-2 Activity 2 Finman 1Документ3 страницыMalinab Aira Bsba FM 2-2 Activity 2 Finman 1Aira MalinabОценок пока нет

- Ch04 2021 - UpdatedДокумент37 страницCh04 2021 - UpdatedAryan KalyanОценок пока нет

- The Time Value of Money: Chapter FiveДокумент14 страницThe Time Value of Money: Chapter Fivemahfuz alamОценок пока нет

- Fin - Group 2Документ57 страницFin - Group 2Heidi NatividadОценок пока нет

- Present Value The Current Worth of A Future Sum of Money or Stream of Cash FlowsДокумент10 страницPresent Value The Current Worth of A Future Sum of Money or Stream of Cash FlowsPhamela Mae RicoОценок пока нет

- TVM Concepts ExplainedДокумент15 страницTVM Concepts ExplainedIstiaque AhmedОценок пока нет

- Fidelia Agatha - 2106715765 - Summary & Problem MK - Pertemuan Ke-4Документ12 страницFidelia Agatha - 2106715765 - Summary & Problem MK - Pertemuan Ke-4Fidelia AgathaОценок пока нет

- ENERGY AUDITING & DCFДокумент18 страницENERGY AUDITING & DCFDIVYA PRASOONA CОценок пока нет

- Time Value of MoneyДокумент24 страницыTime Value of MoneyCharu Modi100% (1)

- TVMДокумент28 страницTVMafnantahirОценок пока нет

- Basic Practical Examples: Simple Interest Compound Interest. PrincipalДокумент10 страницBasic Practical Examples: Simple Interest Compound Interest. PrincipalArvie Angeles AlferezОценок пока нет

- Chapter 4 Problem SetДокумент3 страницыChapter 4 Problem SetNasir Ali RizviОценок пока нет

- Chapter 4Документ50 страницChapter 422GayeonОценок пока нет

- Research Paper Time Value of Money 2Документ11 страницResearch Paper Time Value of Money 2Nhung TaОценок пока нет

- Fm-Module II Word Document - Anjitha Jyothish Uvais PDFДокумент17 страницFm-Module II Word Document - Anjitha Jyothish Uvais PDFMuhammed HuvaisОценок пока нет

- SemiFinals Topic On InterestДокумент9 страницSemiFinals Topic On InterestNami LaurennnОценок пока нет

- BCH 503 SM02Документ4 страницыBCH 503 SM02sugandh bajajОценок пока нет

- Chapter 4 - Time Value of MoneyДокумент46 страницChapter 4 - Time Value of MoneyAubrey AlvarezОценок пока нет

- Compound Interest Factors ExplainedДокумент61 страницаCompound Interest Factors ExplainedJom Ancheta BautistaОценок пока нет

- Importance of Time Value of Money in Financial ManagementДокумент16 страницImportance of Time Value of Money in Financial Managementtanmayjoshi969315Оценок пока нет

- FM I Note - Chapter Three (TVM)Документ15 страницFM I Note - Chapter Three (TVM)zewdieОценок пока нет

- Time Value of Money Concepts ExplainedДокумент22 страницыTime Value of Money Concepts ExplainedmedrekОценок пока нет

- Chapter 3Документ19 страницChapter 3GODОценок пока нет

- TVM: Calculating Future, Present Values and Loan PaymentsДокумент26 страницTVM: Calculating Future, Present Values and Loan PaymentsSushil KharelОценок пока нет

- Financial Management 1: Prof. R Madhumathi Department of Management StudiesДокумент31 страницаFinancial Management 1: Prof. R Madhumathi Department of Management StudiesKishore JohnОценок пока нет

- Topic 2 Principles of Money-Time RelationshipДокумент28 страницTopic 2 Principles of Money-Time RelationshipJeshua Llorera0% (1)

- MathДокумент4 страницыMathTrisha ChanОценок пока нет

- Learning Packet 5 Time Value of MoneyДокумент10 страницLearning Packet 5 Time Value of MoneyPrincess Marie BaldoОценок пока нет

- Lecture 5-9 Chapter 4aДокумент30 страницLecture 5-9 Chapter 4aAli AlluwaimiОценок пока нет

- Time Value of Money ConceptsДокумент38 страницTime Value of Money ConceptsBablooОценок пока нет

- Present Value of AnДокумент1 страницаPresent Value of AnAMAN KHANNAОценок пока нет

- Compound Interest: The Mathematical Constant eДокумент33 страницыCompound Interest: The Mathematical Constant emhrscribd014Оценок пока нет

- The Time Value of MoneyДокумент75 страницThe Time Value of MoneySanchit AroraОценок пока нет

- The Time Value of MoneyДокумент43 страницыThe Time Value of MoneyLAKKAMTHOTI DAVIDRAJUОценок пока нет

- Interest and The Time Value of MoneyДокумент23 страницыInterest and The Time Value of MoneyReian Cais SayatОценок пока нет

- FM Chapter 5Документ65 страницFM Chapter 5Nagiib Haibe Ibrahim Awale 6107Оценок пока нет

- Concept of Value and Return Question and AnswerДокумент4 страницыConcept of Value and Return Question and Answervinesh1515Оценок пока нет

- Remembering The Lonely Struggle of Otto OtepkaДокумент3 страницыRemembering The Lonely Struggle of Otto OtepkabmxengineeringОценок пока нет

- Giant Pumpkin Tips From Record-Breaking Grower Ron Wallace - ABC NewsДокумент8 страницGiant Pumpkin Tips From Record-Breaking Grower Ron Wallace - ABC NewsbmxengineeringОценок пока нет

- Highlights For Children - Wikipedia, The Free EncyclopediaДокумент6 страницHighlights For Children - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Roger Blaine Porter (Born 19 June 1946) Is An American: From Wikipedia, The Free EncyclopediaДокумент3 страницыRoger Blaine Porter (Born 19 June 1946) Is An American: From Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Clyde Engineering - Wikipedia, The Free EncyclopediaДокумент6 страницClyde Engineering - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Shot Put - Wikipedia, The Free EncyclopediaДокумент13 страницShot Put - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Knock-Knock Joke - Wikipedia, The Free EncyclopediaДокумент3 страницыKnock-Knock Joke - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- A D.C. Politician's Secret Woes and Shocking End - WAMU 88Документ4 страницыA D.C. Politician's Secret Woes and Shocking End - WAMU 88bmxengineeringОценок пока нет

- New South Wales 82 Class Locomotive - Wikipedia, The Free EncyclopediaДокумент2 страницыNew South Wales 82 Class Locomotive - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Knock-Knock Joke - Wikipedia, The Free EncyclopediaДокумент3 страницыKnock-Knock Joke - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Geochemistry - Wikipedia, The Free EncyclopediaДокумент6 страницGeochemistry - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Richard Bronson - Wikipedia, The Free EncyclopediaДокумент5 страницRichard Bronson - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Hollis BДокумент3 страницыHollis BbmxengineeringОценок пока нет

- Shot Put - Wikipedia, The Free EncyclopediaДокумент13 страницShot Put - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Christopher Chenery - Wikipedia, The Free EncyclopediaДокумент3 страницыChristopher Chenery - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Christopher Chenery - Wikipedia, The Free EncyclopediaДокумент3 страницыChristopher Chenery - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Meadow Event Park - Wikipedia, The Free EncyclopediaДокумент2 страницыMeadow Event Park - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Hollis BДокумент3 страницыHollis BbmxengineeringОценок пока нет

- Anne Osborn Krueger - Wikipedia, The Free EncyclopediaДокумент3 страницыAnne Osborn Krueger - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- World Bank - Wikipedia, The Free EncyclopediaДокумент19 страницWorld Bank - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Django Reinhardt - Wikipedia, The Free EncyclopediaДокумент11 страницDjango Reinhardt - Wikipedia, The Free Encyclopediabmxengineering100% (1)

- Air-Raid Shelter - Wikipedia, The Free EncyclopediaДокумент15 страницAir-Raid Shelter - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Bhopal - Wikipedia, The Free EncyclopediaДокумент15 страницBhopal - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Air-Raid Shelter - Wikipedia, The Free EncyclopediaДокумент15 страницAir-Raid Shelter - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Noddy Holder - Wikipedia, The Free EncyclopediaДокумент7 страницNoddy Holder - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Semolina Pudding - Wikipedia, The Free EncyclopediaДокумент2 страницыSemolina Pudding - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Tributary - Wikipedia, The Free EncyclopediaДокумент2 страницыTributary - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Sago Pudding - Wikipedia, The Free EncyclopediaДокумент1 страницаSago Pudding - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Sago Pudding - Wikipedia, The Free EncyclopediaДокумент1 страницаSago Pudding - Wikipedia, The Free EncyclopediabmxengineeringОценок пока нет

- Internship ReportДокумент70 страницInternship ReportVishwaMohan50% (2)

- 03 AGS General Principles of Taxation VI C PDFДокумент10 страниц03 AGS General Principles of Taxation VI C PDFGabriel Jhick SaliwanОценок пока нет

- Bcom V Semester SyllabusДокумент23 страницыBcom V Semester SyllabusPriyadharshini RОценок пока нет

- Atul Auto LTD.: Ratio & Company AnalysisДокумент7 страницAtul Auto LTD.: Ratio & Company AnalysisMohit KanjwaniОценок пока нет

- Insurance Commission Ruling on Life Insurance ClaimsДокумент8 страницInsurance Commission Ruling on Life Insurance ClaimsMarioneMaeThiamОценок пока нет

- Chapter 4Документ28 страницChapter 4Shibly SadikОценок пока нет

- Economy 1 PDFДокумент163 страницыEconomy 1 PDFAnil Kumar SudarsiОценок пока нет

- Chapter 2 Practice Questions PDFДокумент9 страницChapter 2 Practice Questions PDFleili fallahОценок пока нет

- 2013 Year in Review - Dave CollumДокумент51 страница2013 Year in Review - Dave CollumAllen BainsОценок пока нет

- Adampak AR 09Документ74 страницыAdampak AR 09diffsoftОценок пока нет

- Chapter 6-Cost TheoryДокумент28 страницChapter 6-Cost TheoryFuad HasanОценок пока нет

- Notes - Sap BPC 340Документ10 страницNotes - Sap BPC 340anusssnair8808Оценок пока нет

- FA1Документ289 страницFA1Abhishek BhatnagarОценок пока нет

- Dumy The 14th Surana and Surana National Corporate LawДокумент23 страницыDumy The 14th Surana and Surana National Corporate Lawkarti_am100% (1)

- Cost Online QuestionДокумент7 страницCost Online QuestionKashif RaheemОценок пока нет

- Pricing Strategies of Airtel: Under The Supervision of Submitted byДокумент31 страницаPricing Strategies of Airtel: Under The Supervision of Submitted byAnurag RahejaОценок пока нет

- Nature, Scope, Need and Problems For International BusinessДокумент5 страницNature, Scope, Need and Problems For International BusinessSonia LawsonОценок пока нет

- DuPont analysis assignmentДокумент5 страницDuPont analysis assignmentআশিকুর রহমান100% (1)

- Costs, Scale of Production and Break-Even Analysis: Revision AnswersДокумент4 страницыCosts, Scale of Production and Break-Even Analysis: Revision AnswersQ. T.100% (1)

- Power Points Sets Milgrom&Roberts Chapter7Документ12 страницPower Points Sets Milgrom&Roberts Chapter7Neel ChakravartyОценок пока нет

- Research Grant GuidelinesДокумент12 страницResearch Grant GuidelinessckamoteОценок пока нет

- Aa2 - Chapter 8 Suggested Answers: Exercise 8 - 1Документ5 страницAa2 - Chapter 8 Suggested Answers: Exercise 8 - 1Izzy BОценок пока нет