Вам также может понравиться

- Syllabus-IPC First Semester 2015-2016Документ14 страницSyllabus-IPC First Semester 2015-2016Dorothy PuguonОценок пока нет

- PD 1354Документ5 страницPD 1354Dorothy PuguonОценок пока нет

- RMC 73-2007Документ2 страницыRMC 73-2007Dorothy PuguonОценок пока нет

- List of Revenue Regulations 2012Документ42 страницыList of Revenue Regulations 2012Dorothy PuguonОценок пока нет

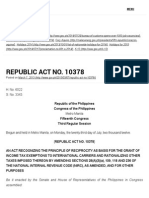

- Ra 10378Документ6 страницRa 10378Dorothy PuguonОценок пока нет

- List of Revenue Memorandum Orders 2012Документ88 страницList of Revenue Memorandum Orders 2012Dorothy PuguonОценок пока нет

- Rmo 17-2002Документ4 страницыRmo 17-2002Anonymous Q0KzFR2iОценок пока нет

- PD 87Документ18 страницPD 87Dorothy PuguonОценок пока нет

- Ra 9504 Minimum Wage and Optional Standard DeductionДокумент6 страницRa 9504 Minimum Wage and Optional Standard Deductionapi-247793055Оценок пока нет

- RMC 77-2003Документ4 страницыRMC 77-2003Dorothy PuguonОценок пока нет

- RA No.7549Документ2 страницыRA No.7549Dorothy PuguonОценок пока нет

- 76-2003 Exemption Nonstock Non ProfitДокумент3 страницы76-2003 Exemption Nonstock Non Profitapi-247793055Оценок пока нет

- RR 13-98Документ17 страницRR 13-98Dorothy PuguonОценок пока нет

- RMC 76 2003Документ1 страницаRMC 76 2003Dorothy PuguonОценок пока нет

- Pal V Palea 19 Scra 483Документ2 страницыPal V Palea 19 Scra 483Dorothy PuguonОценок пока нет

- Producers Bank of The Phil Vs NLRC - 118069 - November 16, 1998Документ4 страницыProducers Bank of The Phil Vs NLRC - 118069 - November 16, 1998Dorothy PuguonОценок пока нет

- Nestle V NLRCДокумент3 страницыNestle V NLRCDorothy PuguonОценок пока нет

- RR 2-98Документ57 страницRR 2-98Dorothy PuguonОценок пока нет

- FEATI V BautistaДокумент16 страницFEATI V BautistaDorothy PuguonОценок пока нет

- Cebu Seamen's Assoc V 1992Документ3 страницыCebu Seamen's Assoc V 1992Dorothy PuguonОценок пока нет

- 109406Документ14 страниц109406Dorothy PuguonОценок пока нет

- RespondentsДокумент17 страницRespondentsDorothy PuguonОценок пока нет

- MarcusДокумент10 страницMarcusAngeles Sabandal SalinasОценок пока нет

- Nea V CoaДокумент10 страницNea V CoaDorothy PuguonОценок пока нет

- Province of North Cotabato Vs RepublicДокумент55 страницProvince of North Cotabato Vs Republicfidel_ramos_1100% (1)

- Civil Liberties Vs Executive SecretaryДокумент9 страницCivil Liberties Vs Executive SecretarySannie RemotinОценок пока нет

- RespondentsДокумент9 страницRespondentsDorothy PuguonОценок пока нет

- Nac V CoaДокумент8 страницNac V CoaDorothy PuguonОценок пока нет

- Cruz V CoaДокумент4 страницыCruz V CoaDorothy PuguonОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Municipal Ordinance No. 05-2014Документ2 страницыMunicipal Ordinance No. 05-2014SBGuinobatanОценок пока нет

- Is Silence Truly AcquiessenceДокумент9 страницIs Silence Truly Acquiessencebmhall65100% (1)

- Burma Will Remain Rich, Poor and Controversial': Published: 9 April 2010Документ11 страницBurma Will Remain Rich, Poor and Controversial': Published: 9 April 2010rheito6745Оценок пока нет

- Biography Nelson MandelaДокумент4 страницыBiography Nelson MandelaBunga ChanОценок пока нет

- Court of Appeals: Fourth DivisionДокумент14 страницCourt of Appeals: Fourth DivisionBrian del MundoОценок пока нет

- Universal Food Corp. v. CAДокумент2 страницыUniversal Food Corp. v. CAAiress Canoy CasimeroОценок пока нет

- Pavon v. Norfolk Police Department Et Al - Document No. 5Документ3 страницыPavon v. Norfolk Police Department Et Al - Document No. 5Justia.comОценок пока нет

- Affidavit of Consent Exhumation 2 (BONG)Документ3 страницыAffidavit of Consent Exhumation 2 (BONG)Tonton Reyes100% (1)

- Citizens' Perceptions On Uganda's Governance - An Opinion Poll ReportДокумент40 страницCitizens' Perceptions On Uganda's Governance - An Opinion Poll ReportAfrican Centre for Media ExcellenceОценок пока нет

- Fil-Estate - Properties - Inc. - v. - Spouses - Go - DigestДокумент2 страницыFil-Estate - Properties - Inc. - v. - Spouses - Go - DigestAllen Windel BernabeОценок пока нет

- 2021 2 1502 46783 Judgement 11-Sep-2023Документ12 страниц2021 2 1502 46783 Judgement 11-Sep-2023Rahul TiwariОценок пока нет

- Langer, David Alan Sklansky - Prosecutors and Democracy, A Cross-National Study (2017, Cambridge University Press)Документ361 страницаLanger, David Alan Sklansky - Prosecutors and Democracy, A Cross-National Study (2017, Cambridge University Press)fbracacciniОценок пока нет

- Bureau of Customs V Whelan DigestДокумент2 страницыBureau of Customs V Whelan DigestJaypee OrtizОценок пока нет

- Introduction To Philippine Criminal Justice SystemДокумент68 страницIntroduction To Philippine Criminal Justice SystemLouvieBuhayОценок пока нет

- Updated Bandolera Constitution Appendix A-General InfoДокумент3 страницыUpdated Bandolera Constitution Appendix A-General Infoapi-327108361Оценок пока нет

- PP V Sergio & Lacanilao, GR No. 240053, Oct 9, 2019 FactsДокумент3 страницыPP V Sergio & Lacanilao, GR No. 240053, Oct 9, 2019 FactsBerliBeb100% (1)

- Guaranteed Tobacco Arrival Condition DisputeДокумент12 страницGuaranteed Tobacco Arrival Condition DisputeFaye Cience BoholОценок пока нет

- What Is An Unenforceable ContractДокумент5 страницWhat Is An Unenforceable ContractJarvy PinonganОценок пока нет

- Legal requirements for international marriageДокумент1 страницаLegal requirements for international marriagemaria fe moncadaОценок пока нет

- VII World Human Rights Moot Court Competition 8-10 December 2015 Geneva, SwitzerlandДокумент52 страницыVII World Human Rights Moot Court Competition 8-10 December 2015 Geneva, SwitzerlandShobhit ChaudharyОценок пока нет

- Eo 292 PDFДокумент286 страницEo 292 PDFWilma P.Оценок пока нет

- KP Law BROCHUREДокумент7 страницKP Law BROCHUREIvan_jaydee100% (1)

- POLITICAL AND INTERNATIONAL LAW REVIEW: THE APPOINTING POWER OF THE PRESIDENTДокумент16 страницPOLITICAL AND INTERNATIONAL LAW REVIEW: THE APPOINTING POWER OF THE PRESIDENTJumel John H. ValeroОценок пока нет

- Union of India Driving License: Issuing Authority: ASST - RTO, JAUNPURДокумент1 страницаUnion of India Driving License: Issuing Authority: ASST - RTO, JAUNPURRAMESH YADAVОценок пока нет

- Vasai Housing Federation AppendicesДокумент6 страницVasai Housing Federation AppendicesPrasadОценок пока нет

- The Code of Civil Procedure, 1908 Non-Joinder and Misjoinder Parties To SuitsДокумент13 страницThe Code of Civil Procedure, 1908 Non-Joinder and Misjoinder Parties To Suitsnirav doshiОценок пока нет

- Pentagon PapersДокумент4 страницыPentagon PapersGill ChetanpalОценок пока нет

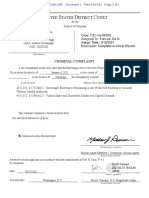

- USA Vs Andrew CavanaughДокумент1 страницаUSA Vs Andrew CavanaughNBC MontanaОценок пока нет

- Transpo DIGESTДокумент5 страницTranspo DIGESTJesterОценок пока нет

- Objective-Questions CLДокумент119 страницObjective-Questions CLRaja Ahsan TariqОценок пока нет