Вам также может понравиться

- Colorado Economic and Fiscal Outlook March 2020Документ36 страницColorado Economic and Fiscal Outlook March 2020Michael_Lee_Roberts100% (1)

- Natasha Patnode Settlement AgreementДокумент6 страницNatasha Patnode Settlement AgreementMichael_Lee_RobertsОценок пока нет

- Lookout Mountain Youth Services Center: Council of Juvenile Correctional Administrators Recommendations With Action StepsДокумент20 страницLookout Mountain Youth Services Center: Council of Juvenile Correctional Administrators Recommendations With Action StepsMichael_Lee_RobertsОценок пока нет

- Lookout Mountain Youth Services Center: Council of Juvenile Correctional Administrators ReportДокумент25 страницLookout Mountain Youth Services Center: Council of Juvenile Correctional Administrators ReportMichael_Lee_RobertsОценок пока нет

- Officer Susan Mercado: Denver Police Department Order of DisciplineДокумент15 страницOfficer Susan Mercado: Denver Police Department Order of DisciplineMichael_Lee_RobertsОценок пока нет

- Mesa County Economic Update, Fourth Quarter 2019Документ13 страницMesa County Economic Update, Fourth Quarter 2019Michael_Lee_RobertsОценок пока нет

- U.S. Supreme Court Petition: Leo Lech, Et Al., v. City of Greenwood Village, Et Al.Документ34 страницыU.S. Supreme Court Petition: Leo Lech, Et Al., v. City of Greenwood Village, Et Al.Michael_Lee_RobertsОценок пока нет

- Officer Austin Barela: Denver Police Department Order of DisciplineДокумент15 страницOfficer Austin Barela: Denver Police Department Order of DisciplineMichael_Lee_RobertsОценок пока нет

- Paul Vranas Denver Pit Bull Expert Testimony and Evidence ReviewДокумент4 страницыPaul Vranas Denver Pit Bull Expert Testimony and Evidence ReviewMichael_Lee_Roberts0% (1)

- Senate Bill 20-156Документ8 страницSenate Bill 20-156Michael_Lee_RobertsОценок пока нет

- Estate of Allan George, Et Al., v. City of Rifle, Et Al.Документ20 страницEstate of Allan George, Et Al., v. City of Rifle, Et Al.Michael_Lee_RobertsОценок пока нет

- Missing and Murdered Indigenous Women and Girls ReportДокумент28 страницMissing and Murdered Indigenous Women and Girls ReportMichael_Lee_RobertsОценок пока нет

- Denver Dog and Cat Bites by Breed 2019Документ2 страницыDenver Dog and Cat Bites by Breed 2019Michael_Lee_RobertsОценок пока нет

- Additional Denver Dog Bite Statistics 2019Документ2 страницыAdditional Denver Dog Bite Statistics 2019Michael_Lee_RobertsОценок пока нет

- House Bill 20-1014Документ6 страницHouse Bill 20-1014Michael_Lee_RobertsОценок пока нет

- Xiaoli Gao and Zhong Wei Zhang IndictmentДокумент12 страницXiaoli Gao and Zhong Wei Zhang IndictmentMichael_Lee_RobertsОценок пока нет

- Paul Vranas Letter To Denver City Council Re: Pit BullsДокумент1 страницаPaul Vranas Letter To Denver City Council Re: Pit BullsMichael_Lee_RobertsОценок пока нет

- Dr. William Moreau Lawsuit Press ReleaseДокумент1 страницаDr. William Moreau Lawsuit Press ReleaseMichael_Lee_RobertsОценок пока нет

- Senate Joint Resolution 20-006Документ7 страницSenate Joint Resolution 20-006Michael_Lee_RobertsОценок пока нет

- Suicide by Cop: Protocol and Training GuideДокумент12 страницSuicide by Cop: Protocol and Training GuideMichael_Lee_RobertsОценок пока нет

- Brandon Valdez Officer-Involved Shooting Decision LetterДокумент13 страницBrandon Valdez Officer-Involved Shooting Decision LetterMichael_Lee_RobertsОценок пока нет

- Senate Bill 19-091Документ6 страницSenate Bill 19-091Michael_Lee_RobertsОценок пока нет

- Integrating Communications, Assessment and Tactics (ICAT) Training GuideДокумент72 страницыIntegrating Communications, Assessment and Tactics (ICAT) Training GuideMichael_Lee_Roberts100% (1)

- Denver Public Schools Gender-Neutral Bathrooms ResolutionДокумент3 страницыDenver Public Schools Gender-Neutral Bathrooms ResolutionMichael_Lee_Roberts100% (1)

- Travis Cook v. City of Arvada, Et Al.Документ19 страницTravis Cook v. City of Arvada, Et Al.Michael_Lee_RobertsОценок пока нет

- House Bill 20-1148Документ3 страницыHouse Bill 20-1148Michael_Lee_RobertsОценок пока нет

- Re-Engineering Training On Police Use of ForceДокумент84 страницыRe-Engineering Training On Police Use of ForceMichael_Lee_RobertsОценок пока нет

- Erik Jensen Sentence Commutation LetterДокумент1 страницаErik Jensen Sentence Commutation LetterMichael_Lee_RobertsОценок пока нет

- Colorado Senate Bill 20-065Документ7 страницColorado Senate Bill 20-065Michael_Lee_RobertsОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- VCCGenerator - Valid Credit Card Generator 2021 (Документ1 страницаVCCGenerator - Valid Credit Card Generator 2021 (Safir JalaliОценок пока нет

- Fee Receipt: Student InformationДокумент1 страницаFee Receipt: Student InformationAVNEESH SINGHANIA100% (1)

- UPI Procedural Guidelines - PDF 26112019 OnwebsiteLIVE 0Документ141 страницаUPI Procedural Guidelines - PDF 26112019 OnwebsiteLIVE 0Andy_suman100% (1)

- 7 Commissioner of Internal Revenue v. John Gotamco & Sons, Inc.Документ6 страниц7 Commissioner of Internal Revenue v. John Gotamco & Sons, Inc.Vianice BaroroОценок пока нет

- Klaus Vogel On Double Taxation Conventions - BrochureДокумент4 страницыKlaus Vogel On Double Taxation Conventions - Brochuremejocoba820% (1)

- StatementДокумент3 страницыStatementStephen SnowdenОценок пока нет

- Bar Exam Questions Income TaxationДокумент11 страницBar Exam Questions Income TaxationG.B. SevillaОценок пока нет

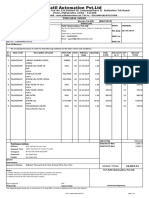

- Patil Automation PVT - LTDДокумент1 страницаPatil Automation PVT - LTDAnonymous ehfNj9FFj7Оценок пока нет

- IncomeTax Banggawan2019 Ch6Документ15 страницIncomeTax Banggawan2019 Ch6Noreen Ledda25% (4)

- GST - PersonalДокумент62 страницыGST - PersonalSri NiОценок пока нет

- SAP Business One Tables - Business One - SCN WikiДокумент7 страницSAP Business One Tables - Business One - SCN WikiMaicon Macedo100% (1)

- Ir 292Документ22 страницыIr 292samsujОценок пока нет

- Assignment 2 MIS 207 1612631030Документ6 страницAssignment 2 MIS 207 1612631030shamim islam limonОценок пока нет

- Tax Rights and RemediesДокумент122 страницыTax Rights and RemediesMiguel Cornelius HerreraОценок пока нет

- Percentage Taxes NotesДокумент4 страницыPercentage Taxes NotesWearIt Co.Оценок пока нет

- Adobe Scan Mar 24, 2023Документ1 страницаAdobe Scan Mar 24, 2023SIDDHANT KUMARОценок пока нет

- Barops Taxation 2020Документ241 страницаBarops Taxation 2020Gerry Ombrog100% (1)

- New York 501c3 ChecklistДокумент6 страницNew York 501c3 ChecklistFred AbramsonОценок пока нет

- America 1st Legal Foundation IRS990 Fiscal Year 2021Документ37 страницAmerica 1st Legal Foundation IRS990 Fiscal Year 2021File 411Оценок пока нет

- April BillДокумент1 страницаApril BillAlpesh PatelОценок пока нет

- Annex N of RMO No. 29-2002Документ1 страницаAnnex N of RMO No. 29-2002BuenafeОценок пока нет

- Value Plus Current AccountДокумент5 страницValue Plus Current AccountmalikzaidОценок пока нет

- Gmail - Booking Confirmation On IRCTC, Train - 22691, 28-May-2022, 3A, GTL - NZMДокумент1 страницаGmail - Booking Confirmation On IRCTC, Train - 22691, 28-May-2022, 3A, GTL - NZMkridddhОценок пока нет

- Oracle ARДокумент6 страницOracle ARMr. JalilОценок пока нет

- E-Way Bill: Government of IndiaДокумент1 страницаE-Way Bill: Government of IndiaVIVEK N KHAKHARAОценок пока нет

- Evolution OF Philippine Taxation Evolution OF Philippine TaxationДокумент6 страницEvolution OF Philippine Taxation Evolution OF Philippine TaxationEunji eunОценок пока нет

- PNB Notes For ClassДокумент6 страницPNB Notes For ClassmankОценок пока нет

- Megahertz Internet Network Pvt. LTD.: Retail InvoiceДокумент1 страницаMegahertz Internet Network Pvt. LTD.: Retail InvoiceAyush ThapliyalОценок пока нет

- Your Bill: 74759534 2 Nov 2018 1 Oct 2018 - 31 Oct 2018 4.2822.18.00.102482Документ7 страницYour Bill: 74759534 2 Nov 2018 1 Oct 2018 - 31 Oct 2018 4.2822.18.00.102482janu_jeОценок пока нет

- Kepco Philippines Corporation v. CIRДокумент17 страницKepco Philippines Corporation v. CIRAronJamesОценок пока нет