Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Trendsetter Term SheetPPTДокумент16 страницTrendsetter Term SheetPPTMary Williams100% (2)

- Resume Book: Columbia Healthcare and Pharmaceutical Management ProgramДокумент44 страницыResume Book: Columbia Healthcare and Pharmaceutical Management ProgramJohn Mathias100% (2)

- UPSC Result 2015Документ43 страницыUPSC Result 2015Vishal KumarОценок пока нет

- Upsc Pre 2015 Gs Paper 1Документ25 страницUpsc Pre 2015 Gs Paper 1rmbj94_scribdОценок пока нет

- Essential Guide to Satellite CommunicationДокумент60 страницEssential Guide to Satellite CommunicationKevin Hefayana Putra100% (1)

- SSC Fci Grade II Exam Paper I Solved Question PaperДокумент15 страницSSC Fci Grade II Exam Paper I Solved Question Papernainesh goteОценок пока нет

- UPSC CSM2015 Press Note EAdmitCard EnglДокумент1 страницаUPSC CSM2015 Press Note EAdmitCard EnglNaga NagendraОценок пока нет

- Disaster ManagementДокумент53 страницыDisaster ManagementVivek RanganathanОценок пока нет

- UPSC - CSM2015 - Press Note - eAdmitCard - Engl PDFДокумент1 страницаUPSC - CSM2015 - Press Note - eAdmitCard - Engl PDFNaga NagendraОценок пока нет

- Chapter-1 Indian Contract Act 1872Документ100 страницChapter-1 Indian Contract Act 1872aahana77Оценок пока нет

- ResultДокумент10 страницResultNidhin Das SОценок пока нет

- The Invisible Landscape 1975Документ9 страницThe Invisible Landscape 1975Naga NagendraОценок пока нет

- Natural Hazards & Disaster Management 44Документ51 страницаNatural Hazards & Disaster Management 44Lohith GsОценок пока нет

- The Invisible Landscape 1975Документ9 страницThe Invisible Landscape 1975Naga NagendraОценок пока нет

- Scra-14 Cut-OffДокумент1 страницаScra-14 Cut-OffShamal KambleОценок пока нет

- Using Earthquakes To Image Earth's InteriorДокумент5 страницUsing Earthquakes To Image Earth's Interiorbancom25596Оценок пока нет

- Mpunyb Wolfrum Matz 4Документ36 страницMpunyb Wolfrum Matz 4Naga NagendraОценок пока нет

- Papers Environment and AgricultureДокумент10 страницPapers Environment and AgricultureNaga NagendraОценок пока нет

- Motion in The Ocean: Ocean Currents Lesson PlanДокумент17 страницMotion in The Ocean: Ocean Currents Lesson PlanNaga Nagendra100% (1)

- Ocean MotionДокумент48 страницOcean MotionNaga NagendraОценок пока нет

- Study On Fuel Policy Reforms in India by IEAДокумент116 страницStudy On Fuel Policy Reforms in India by IEAAshok PatsamatlaОценок пока нет

- Islam, Globalization, and CounterterrorismДокумент8 страницIslam, Globalization, and CounterterrorismMatejic MilanОценок пока нет

- Rupert Sheldrake - Morphic Resonance PaperДокумент12 страницRupert Sheldrake - Morphic Resonance Paperniklase79Оценок пока нет

- Nature and Teaching by PlatoДокумент10 страницNature and Teaching by PlatoNaga NagendraОценок пока нет

- 1 Evidence For Earth's Crust, Mantle & CoreДокумент12 страниц1 Evidence For Earth's Crust, Mantle & CoreNaga NagendraОценок пока нет

- Stereotypes of Muslims and Support For The War On Terror: Jsides@gwu - EduДокумент59 страницStereotypes of Muslims and Support For The War On Terror: Jsides@gwu - EduNaga NagendraОценок пока нет

- Migration Crisis Solutions v4 Perspective 0Документ2 страницыMigration Crisis Solutions v4 Perspective 0Naga NagendraОценок пока нет

- Kumar Law of These AДокумент25 страницKumar Law of These ANaga NagendraОценок пока нет

- Rupert Sheldrake - Society, Spirit & Ritual - Morphic Resonance and The Collective Unconcsious II.Документ7 страницRupert Sheldrake - Society, Spirit & Ritual - Morphic Resonance and The Collective Unconcsious II.Dositheus SethОценок пока нет

- Kumar Law of These AДокумент25 страницKumar Law of These ANaga NagendraОценок пока нет

- MAMCom MSCДокумент10 страницMAMCom MSCNaga NagendraОценок пока нет

- Jamine 0607 MozambiqueДокумент166 страницJamine 0607 MozambiqueKevin Ken Sison GancheroОценок пока нет

- Chapter 4 - Investments in Equity SecuritiesДокумент51 страницаChapter 4 - Investments in Equity SecuritiesYel100% (2)

- Imc NotesДокумент2 страницыImc NotesAiko KawachiОценок пока нет

- Spring 2016 Revision Guide Fin 4050 Section B and CДокумент1 страницаSpring 2016 Revision Guide Fin 4050 Section B and CPuneetPurshotamОценок пока нет

- 24 Securities OperationsДокумент61 страница24 Securities OperationsPaula Ella BatasОценок пока нет

- Statement of Account: L246G SBI Gold Fund - Regular Plan - Growth NAV As On 14/10/2015: 8.8804Документ4 страницыStatement of Account: L246G SBI Gold Fund - Regular Plan - Growth NAV As On 14/10/2015: 8.8804hari sharmaОценок пока нет

- We TubeДокумент38 страницWe TubeGaurav ChikhalikarОценок пока нет

- BUS227Документ70 страницBUS227Dauda AdijatОценок пока нет

- Mining case nationality disputeДокумент15 страницMining case nationality disputeteryo expressОценок пока нет

- EF3A HDT BoP Currency Exchange PCB4Документ45 страницEF3A HDT BoP Currency Exchange PCB4Prapendra SinghОценок пока нет

- Managerial Finance Chapter 8 - Risk and Return by Endah RiwayatunДокумент43 страницыManagerial Finance Chapter 8 - Risk and Return by Endah RiwayatunEndah Riwayatun100% (2)

- Unit 3: Ind As 110: Consolidated Financial StatementsДокумент49 страницUnit 3: Ind As 110: Consolidated Financial StatementsA.S. Nooruddin AhmedОценок пока нет

- Islamic REITsДокумент6 страницIslamic REITsfarhanОценок пока нет

- EBIT EPS AnalysisДокумент17 страницEBIT EPS AnalysisAditya GuptaОценок пока нет

- McDonald's Stock Clearly Benefits From Its Large Buybacks - Here Is Why (NYSE - MCD) - Seeking AlphaДокумент12 страницMcDonald's Stock Clearly Benefits From Its Large Buybacks - Here Is Why (NYSE - MCD) - Seeking AlphaWaleed TariqОценок пока нет

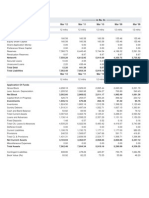

- Balance Sheet and P&L of CiplaДокумент2 страницыBalance Sheet and P&L of CiplaPratik AhluwaliaОценок пока нет

- Getting Started Tech AnalysisДокумент42 страницыGetting Started Tech Analysiszubair latif100% (1)

- Chapter 11: Arbitrage Pricing TheoryДокумент7 страницChapter 11: Arbitrage Pricing TheorySilviu TrebuianОценок пока нет

- Darden Case GuideДокумент123 страницыDarden Case Guidemaverick3581Оценок пока нет

- Comparative Study On Ulips in The Indian Insurance Market For Tata Aig Life by Delnaaz ParvezДокумент71 страницаComparative Study On Ulips in The Indian Insurance Market For Tata Aig Life by Delnaaz Parveznarayanamohan0% (2)

- SIRA1H11Документ8 страницSIRA1H11Inde Pendent LkОценок пока нет

- Retail Financial Services Products 2022 FL 509 Report enДокумент78 страницRetail Financial Services Products 2022 FL 509 Report enStathis MetsovitisОценок пока нет

- Golden Midcap Portfolio: UpdateДокумент7 страницGolden Midcap Portfolio: UpdateKshitij MathurОценок пока нет

- Money Banking MGT 411 LecturesДокумент148 страницMoney Banking MGT 411 LecturesshazadОценок пока нет

- Post Qualification FormДокумент25 страницPost Qualification FormLalit Trivedi100% (1)

- Indian Ladies Handbag Industry ReportДокумент38 страницIndian Ladies Handbag Industry ReportReevolv Advisory Services Private LimitedОценок пока нет

- Consolidated Financial Statements of Eicher MotorsДокумент1 страницаConsolidated Financial Statements of Eicher MotorsAyushi PandagreОценок пока нет

- 5 Ways to Win in a Post BTFD MarketДокумент17 страниц5 Ways to Win in a Post BTFD Marketemirav2Оценок пока нет