Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Co Blue PrintДокумент52 страницыCo Blue PrintBewqetu SewMehone100% (1)

- BPM Financial Modelling Fundamentals Practical Exercise SolutionsДокумент19 страницBPM Financial Modelling Fundamentals Practical Exercise SolutionsDaria YurovaОценок пока нет

- Review Maam Tormis 1Документ10 страницReview Maam Tormis 1Kristy Dela CernaОценок пока нет

- Tangible Non-Current Assets: QuestionsДокумент5 страницTangible Non-Current Assets: QuestionsЕкатерина КидяшеваОценок пока нет

- Ohada Accounting Plan PDFДокумент72 страницыOhada Accounting Plan PDFNchendeh Christian50% (2)

- Module 6 Leasing (Final)Документ74 страницыModule 6 Leasing (Final)Endrit MansakuОценок пока нет

- Definition and Explanation:: (1) - Adjusting Entries That Convert Assets To ExpensesДокумент8 страницDefinition and Explanation:: (1) - Adjusting Entries That Convert Assets To ExpensesKae Abegail GarciaОценок пока нет

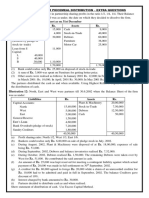

- Piecemeal - Extra QuestionsДокумент4 страницыPiecemeal - Extra Questionskushgarg627Оценок пока нет

- Chapter 2 Cost Terms, Concepts, and ClassificationsДокумент4 страницыChapter 2 Cost Terms, Concepts, and ClassificationsQurat SaboorОценок пока нет

- Self Study Solutions Chapter 5Документ16 страницSelf Study Solutions Chapter 5Jannatul FerdousОценок пока нет

- Delicatessen and Bakery Business PlanДокумент26 страницDelicatessen and Bakery Business PlanJeorge PaxОценок пока нет

- C&MДокумент18 страницC&MSultanaQuader50% (2)

- AP-5906 ReceivablesДокумент6 страницAP-5906 ReceivablesjhouvanОценок пока нет

- Soce2023bskeforms Form1Документ1 страницаSoce2023bskeforms Form1Jamer Ain't SimpОценок пока нет

- Sugarcane Juice Beverage: 1.0 Product and Its ApplicationsДокумент6 страницSugarcane Juice Beverage: 1.0 Product and Its Applicationsygnakumar100% (2)

- Coop 7Документ2 страницыCoop 7hoxhiiОценок пока нет

- Business Studies Paper 3Документ6 страницBusiness Studies Paper 3nkosiissexyОценок пока нет

- Emirates ReportДокумент23 страницыEmirates Reportrussell92Оценок пока нет

- Managerial Accounting Wey Chapter 2Документ88 страницManagerial Accounting Wey Chapter 2Steven ShamОценок пока нет

- (Ahmed Riahi-Belkaoui) Earnings Measurement, DeterДокумент200 страниц(Ahmed Riahi-Belkaoui) Earnings Measurement, DeterdolutamadolutamaОценок пока нет

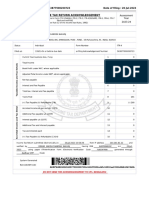

- Itr Fy 22-23-1Документ5 страницItr Fy 22-23-1Omkar kaleОценок пока нет

- Tax 267 Feb21 PyqДокумент8 страницTax 267 Feb21 PyqKenji HiroОценок пока нет

- Chapter FourДокумент14 страницChapter FourMuzamel AbdellaОценок пока нет

- Chapter 7: Accounting For The Business-Type Activities of State and Local GovernmentsДокумент37 страницChapter 7: Accounting For The Business-Type Activities of State and Local GovernmentshagdincloobleОценок пока нет

- Jonaxx Trading Corporation 1ST PageДокумент1 страницаJonaxx Trading Corporation 1ST PageRona Karylle Pamaran DeCastroОценок пока нет

- Chapter 3 Adjusting The AccountsДокумент87 страницChapter 3 Adjusting The AccountsDuyen Dang Binh Phuong100% (1)

- Strb200809 FullДокумент352 страницыStrb200809 FullRohan MaakanОценок пока нет

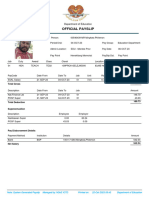

- Official Payslip: Department of EducationДокумент1 страницаOfficial Payslip: Department of Educationphillmingkwa2017Оценок пока нет

- BUS020 Chapter 1 (Outline - Libby Libby)Документ5 страницBUS020 Chapter 1 (Outline - Libby Libby)Amanda RodriguezОценок пока нет

- Ratio AnalysisДокумент37 страницRatio AnalysisPriya SaxenaОценок пока нет