Вам также может понравиться

- Excise Tax AnjДокумент4 страницыExcise Tax AnjAngelyn Marie SavilloОценок пока нет

- Canada Application1Документ5 страницCanada Application1Sharat ChandraОценок пока нет

- Processing An Export Order: I. Confirmation of OrderДокумент4 страницыProcessing An Export Order: I. Confirmation of Orderkaran singhОценок пока нет

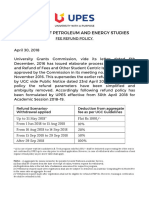

- Upes Refund PolicyДокумент1 страницаUpes Refund PolicyPiyushSharmaОценок пока нет

- Motorcycle Registration Procedure in BangladeshДокумент37 страницMotorcycle Registration Procedure in BangladeshAarajita ParinОценок пока нет

- Horizon Housing REIT PLC ProspectusДокумент214 страницHorizon Housing REIT PLC ProspectusSean SongОценок пока нет

- RCL Bond Format NEWДокумент3 страницыRCL Bond Format NEWALWAR CHAОценок пока нет

- Particulars of Firm: HQ Frontier Works OrganizationДокумент7 страницParticulars of Firm: HQ Frontier Works OrganizationSayam Mughal67% (3)

- 1601C Final Jan 2018 With DPA Comp 2Документ2 страницы1601C Final Jan 2018 With DPA Comp 2Donjoe JoejoejoejoeОценок пока нет

- Les AllégationsДокумент157 страницLes AllégationsRadio-CanadaОценок пока нет

- BusinessДокумент2 страницыBusinessAnonymous l97i3ZОценок пока нет

- Financial Offer of Public Address (PA) Systems FДокумент3 страницыFinancial Offer of Public Address (PA) Systems FMd Omid Hasan SheikhОценок пока нет

- The Boring Company Wastewater Disposal PermitДокумент8 страницThe Boring Company Wastewater Disposal PermitMaria MeranoОценок пока нет

- TRA Taxes at Glance - 2016-17Документ22 страницыTRA Taxes at Glance - 2016-17Timothy Rogatus67% (3)

- Obverse: Received For The Month of .. 20 . Classification MonthlyДокумент2 страницыObverse: Received For The Month of .. 20 . Classification MonthlyAbdul Rehman CheemaОценок пока нет

- FHB Volume - 2Документ155 страницFHB Volume - 2K V Sridharan General Secretary P3 NFPE67% (3)

- Excise Taxes On Certain GoodsДокумент4 страницыExcise Taxes On Certain GoodsshakiraОценок пока нет

- Title ViДокумент30 страницTitle Vimiss independentОценок пока нет

- Ecuador PDFДокумент4 страницыEcuador PDFAndy HidalgoОценок пока нет

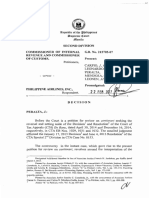

- CIR-vs-PhilAirplinesДокумент11 страницCIR-vs-PhilAirplinesPernia Orsal RomeoОценок пока нет

- Excise Tax WowoweeДокумент18 страницExcise Tax WowoweeAmado Vallejo IIIОценок пока нет

- Hi PdffffffrruДокумент5 страницHi Pdffffffrruswaglordswag123Оценок пока нет

- Percentage TaxДокумент22 страницыPercentage TaxMa.annОценок пока нет

- Goods Documents Required Customs Prescriptions Remarks: United KingdomДокумент6 страницGoods Documents Required Customs Prescriptions Remarks: United KingdomKelz YouknowmynameОценок пока нет

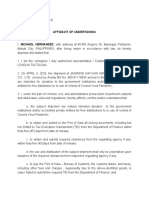

- AFFIDAVIT OF UNDERTAKING SampleДокумент2 страницыAFFIDAVIT OF UNDERTAKING SampleAllanОценок пока нет

- Provided, Further, That Importations of Cigars and Cigarettes, Distilled Spirits and Wines by A Government-Owned and Operated DutyДокумент8 страницProvided, Further, That Importations of Cigars and Cigarettes, Distilled Spirits and Wines by A Government-Owned and Operated DutyJongJongОценок пока нет

- Second Division Commissioner of Internal Revenue and Commissioner of Customs, G.R. No. 215705-07 PresentДокумент12 страницSecond Division Commissioner of Internal Revenue and Commissioner of Customs, G.R. No. 215705-07 PresentLizzette GuiuntabОценок пока нет

- VAT ReviewerДокумент72 страницыVAT ReviewerJohn Kenneth AcostaОценок пока нет

- Value Added TaxДокумент13 страницValue Added TaxKatrina FregillanaОценок пока нет

- BoliviaДокумент6 страницBoliviaKelz YouknowmynameОценок пока нет

- Chapter 12: Tariff and Customs Code: Tax Reviewer: Law of Basic Taxation in The PhilippinesДокумент18 страницChapter 12: Tariff and Customs Code: Tax Reviewer: Law of Basic Taxation in The PhilippinesTeps RaccaОценок пока нет

- Brazil Personal Effect ShipmentДокумент5 страницBrazil Personal Effect ShipmentAugustus DeepakОценок пока нет

- Goods Documents Required Customs Prescriptions Remarks: ChileДокумент4 страницыGoods Documents Required Customs Prescriptions Remarks: ChileKelz YouknowmynameОценок пока нет

- CHAPTER II-Donorrs TaxДокумент5 страницCHAPTER II-Donorrs TaxShiela May Agustin MacarayanОценок пока нет

- Dominican Republic: Goods Documents Required Customs Prescriptions RemarksДокумент4 страницыDominican Republic: Goods Documents Required Customs Prescriptions RemarksKelz YouknowmynameОценок пока нет

- NamibiaДокумент3 страницыNamibiaKelz YouknowmynameОценок пока нет

- Title Iv Value-Added Tax: Chapter I - Imposition of TaxДокумент3 страницыTitle Iv Value-Added Tax: Chapter I - Imposition of TaxNickОценок пока нет

- Cir & Coc v. PALДокумент11 страницCir & Coc v. PALHi Law SchoolОценок пока нет

- VAT - No. 2Документ6 страницVAT - No. 2Jay-ar Pre0% (1)

- Tax Booklet As of 10 November 2016Документ20 страницTax Booklet As of 10 November 2016Trixy ComiaОценок пока нет

- Value-Added TaxДокумент30 страницValue-Added TaxmeriiОценок пока нет

- Tariffs and CustomsДокумент24 страницыTariffs and CustomsNikki GОценок пока нет

- A Requirement On Management, Tax and Consultancy: Cyrra Q. Balignasay BSA-5Документ14 страницA Requirement On Management, Tax and Consultancy: Cyrra Q. Balignasay BSA-5Cyrra BalignasayОценок пока нет

- Value Added TaxДокумент11 страницValue Added TaxYvette Pauline JovenОценок пока нет

- Reviewer BTTДокумент14 страницReviewer BTTAlthea Frances VasalloОценок пока нет

- Business Taxes: Certified Accounting Technician NIAT Office 2015Документ33 страницыBusiness Taxes: Certified Accounting Technician NIAT Office 2015Anonymous Lz2qH7Оценок пока нет

- Section 1Документ46 страницSection 1Luke CruzОценок пока нет

- Goods Documents Required Customs Prescriptions Remarks: IrelandДокумент4 страницыGoods Documents Required Customs Prescriptions Remarks: IrelandKelz YouknowmynameОценок пока нет

- CMTAДокумент11 страницCMTAJaya RhysОценок пока нет

- Republic Act No. 11346: CD Technologies Asia, Inc. 2020Документ15 страницRepublic Act No. 11346: CD Technologies Asia, Inc. 2020Randolph Jon GuerzonОценок пока нет

- Uruguay: Goods Documents Required Customs Prescriptions RemarksДокумент9 страницUruguay: Goods Documents Required Customs Prescriptions RemarksKelz YouknowmynameОценок пока нет

- IBM 2004 Assignment 29th MarchДокумент8 страницIBM 2004 Assignment 29th MarchJaspreet Kaur 541Оценок пока нет

- Excise TaxДокумент50 страницExcise TaxQuinnee VallejosОценок пока нет

- Secret Files For TXДокумент118 страницSecret Files For TXGrace EnriquezОценок пока нет

- Goods Documents Required Customs Prescriptions Remarks: VenezuelaДокумент4 страницыGoods Documents Required Customs Prescriptions Remarks: VenezuelaKelz YouknowmynameОценок пока нет

- Goods Documents Required Customs Prescriptions Remarks: MartiniqueДокумент3 страницыGoods Documents Required Customs Prescriptions Remarks: MartiniqueKelz YouknowmynameОценок пока нет

- RR 3-2008 - DigestДокумент6 страницRR 3-2008 - DigestMich GuarinoОценок пока нет

- Title ViДокумент23 страницыTitle ViErica Mae GuzmanОценок пока нет

- I. Title: Tax Refund Case of Philippine Airlines On Its Imported Cigarettes, Wines, and LiquorsДокумент16 страницI. Title: Tax Refund Case of Philippine Airlines On Its Imported Cigarettes, Wines, and LiquorsEina Rivera TapnioОценок пока нет

- Cmta - Section 800Документ15 страницCmta - Section 800isabella fordОценок пока нет

- Queue Using Linked ListДокумент2 страницыQueue Using Linked ListHassan ZiaОценок пока нет

- Aga 11Документ7 страницAga 11elijbbОценок пока нет

- Financial Ratio Analysis FormulasДокумент4 страницыFinancial Ratio Analysis FormulasVaishali Jhaveri100% (1)

- TSD OSD Portal Quick Start Guide V1.0Документ5 страницTSD OSD Portal Quick Start Guide V1.0sijovow282Оценок пока нет

- 1 - Pengenalan Enterprise ArchitectureДокумент37 страниц1 - Pengenalan Enterprise ArchitectureSILVERОценок пока нет

- Introduction To SCILABДокумент14 страницIntroduction To SCILABMertwysef DevrajОценок пока нет

- Synchronization Checklist PDFДокумент8 страницSynchronization Checklist PDFAdhyartha KerafОценок пока нет

- S No Name of The Company Regional OfficeДокумент39 страницS No Name of The Company Regional OfficeNo nameОценок пока нет

- CorpДокумент14 страницCorpIELTSОценок пока нет

- Appointments & Other Personnel Actions Submission, Approval/Disapproval of AppointmentДокумент7 страницAppointments & Other Personnel Actions Submission, Approval/Disapproval of AppointmentZiiee BudionganОценок пока нет

- Corporation Law Syllabus With Assignment of CasesДокумент4 страницыCorporation Law Syllabus With Assignment of CasesMarilou AgustinОценок пока нет

- Project 2 - Home InsuranceДокумент15 страницProject 2 - Home InsuranceNaveen KumarОценок пока нет

- Debugging With The PL/SQL Debugger: PhilippДокумент51 страницаDebugging With The PL/SQL Debugger: PhilippBenjytox BenjytoxОценок пока нет

- Linux Internet Web Server and Domain Configuration TutorialДокумент59 страницLinux Internet Web Server and Domain Configuration Tutorialrajnishmishra2488Оценок пока нет

- Icd-10 CM Step by Step Guide SheetДокумент12 страницIcd-10 CM Step by Step Guide SheetEdel DurdallerОценок пока нет

- Welcome To Our Presentation: Submitted byДокумент30 страницWelcome To Our Presentation: Submitted byShamim MridhaОценок пока нет

- Salonga Vs Farrales Digest Ful Case PDF FreeДокумент6 страницSalonga Vs Farrales Digest Ful Case PDF FreeElyka RamosОценок пока нет

- NDT Technician TrainingДокумент6 страницNDT Technician TraininglarsonndeservicesОценок пока нет

- Iata 2008 - Annex AДокумент11 страницIata 2008 - Annex Agurungbhim100% (1)

- Ti - e - Protegol 32-97 Jan 08Документ3 страницыTi - e - Protegol 32-97 Jan 08A MahmoodОценок пока нет

- COEN 252 Computer Forensics: Incident ResponseДокумент39 страницCOEN 252 Computer Forensics: Incident ResponseDudeviswaОценок пока нет

- Status of Implementation of Prior Years' Audit RecommendationsДокумент10 страницStatus of Implementation of Prior Years' Audit RecommendationsJoy AcostaОценок пока нет

- Agriculture Water Usage Poster ProjectДокумент1 страницаAgriculture Water Usage Poster Projectapi-339004071Оценок пока нет

- Community Support For IYCF As of 22 SeptДокумент57 страницCommunity Support For IYCF As of 22 SeptMJ ArcillaОценок пока нет

- Type SAP Usage / Definition Example Procurement RotablesДокумент4 страницыType SAP Usage / Definition Example Procurement Rotablessabya1411Оценок пока нет

- 13 Ways The Coronavirus Pandemic Could Forever Change The Way We WorkДокумент20 страниц13 Ways The Coronavirus Pandemic Could Forever Change The Way We WorkAbidullahОценок пока нет

- Stoxx Dividend Points Calculation Guide: Version 1.1 March 2010Документ4 страницыStoxx Dividend Points Calculation Guide: Version 1.1 March 2010mrtandonОценок пока нет

- Unit 5 PythonДокумент10 страницUnit 5 PythonVikas PareekОценок пока нет

- Cargas Termicas HapДокумент2 страницыCargas Termicas HapArq Alfonso RicoОценок пока нет

- Bank Details and Payment MethodsДокумент1 страницаBank Details and Payment Methodsetrit0% (1)