Вам также может понравиться

- 1 ReviewДокумент98 страниц1 ReviewMuhammad UsmanОценок пока нет

- Attitudes Towards Offensive Advertising Malaysian Muslims ViewsДокумент12 страницAttitudes Towards Offensive Advertising Malaysian Muslims ViewsMuhammad UsmanОценок пока нет

- Manage Opportunity Cost Risk with Zero Cash PracticesДокумент4 страницыManage Opportunity Cost Risk with Zero Cash PracticesMuhammad UsmanОценок пока нет

- Food & Beverages Cost Control Audit ProgramДокумент4 страницыFood & Beverages Cost Control Audit ProgramMuhammad Usman100% (1)

- Cost Audit PresentationДокумент34 страницыCost Audit PresentationMuhammad UsmanОценок пока нет

- Audit Report TemplateДокумент9 страницAudit Report TemplateMuhammad Usman100% (1)

- Manage Opportunity Cost Risk with Zero Cash PracticesДокумент4 страницыManage Opportunity Cost Risk with Zero Cash PracticesMuhammad UsmanОценок пока нет

- Methods of Provision For Bad DebtsДокумент9 страницMethods of Provision For Bad DebtsMuhammad UsmanОценок пока нет

- Skinder e AzamДокумент0 страницSkinder e AzamMuhammad UsmanОценок пока нет

- CIA HandbookДокумент42 страницыCIA HandbookMuhammad UsmanОценок пока нет

- Proposal Preparation GuideДокумент17 страницProposal Preparation GuiderkbayalОценок пока нет

- Ammann Oesch Schmid 2010 Corporate GovernanceДокумент51 страницаAmmann Oesch Schmid 2010 Corporate GovernanceMuhammad UsmanОценок пока нет

- UCP 600 - Training IssuesДокумент12 страницUCP 600 - Training IssuesMuhammad UsmanОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Thesis FinaleДокумент93 страницыThesis FinaleAubreyCapuleОценок пока нет

- WestmountДокумент5 страницWestmountsai chandra100% (1)

- Materi 1 Desain RisetДокумент8 страницMateri 1 Desain RisetDavila Rubianti ArundinaОценок пока нет

- Dabur BRM Assignment AnalysisДокумент11 страницDabur BRM Assignment AnalysisDevОценок пока нет

- MS 07 SolvedДокумент10 страницMS 07 Solvedomshanker44Оценок пока нет

- A Project Report On Microeconomic Analysis of Coca ColaДокумент23 страницыA Project Report On Microeconomic Analysis of Coca ColaAnonymous uZw6hSvkuОценок пока нет

- EntrepreneurshipДокумент16 страницEntrepreneurshipAndreaMarabe100% (1)

- Manufacturing Accounts - Principles of AccountingДокумент6 страницManufacturing Accounts - Principles of AccountingAbdulla Maseeh100% (1)

- Resume 1Документ2 страницыResume 1api-298164137Оценок пока нет

- Managing Finances Mock TestДокумент8 страницManaging Finances Mock TestThuy TranОценок пока нет

- RoutingДокумент2 страницыRoutingCorey PageОценок пока нет

- The Body Shop Case StudyДокумент3 страницыThe Body Shop Case StudysahilsureshОценок пока нет

- WalmartДокумент30 страницWalmartNitin RawatОценок пока нет

- Internal Control Questionnaires for Sales CycleДокумент7 страницInternal Control Questionnaires for Sales CycleandengОценок пока нет

- Unit 5 CrosswordДокумент2 страницыUnit 5 Crosswordapi-356491391Оценок пока нет

- Srinivas Subramanian CV 2Документ6 страницSrinivas Subramanian CV 2Amruthesh BalasubramanianОценок пока нет

- CaseДокумент6 страницCaseG Abhishek RaoОценок пока нет

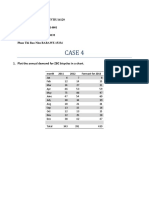

- Case 4: Luyen Ngoc Do Quyen BTFTIU14129 Ngo Khanh Duy BTARIU14601 Pham Gia Huy BTFTIU14132 Phan Thi Bao Nhu BABAWE 15334Документ4 страницыCase 4: Luyen Ngoc Do Quyen BTFTIU14129 Ngo Khanh Duy BTARIU14601 Pham Gia Huy BTFTIU14132 Phan Thi Bao Nhu BABAWE 15334HuynhGiangОценок пока нет

- Wild Shaw (8th Ed.) Connect GuideДокумент494 страницыWild Shaw (8th Ed.) Connect GuideSrikar RootsОценок пока нет

- De Mar's product strategy and OM decisions for service successДокумент4 страницыDe Mar's product strategy and OM decisions for service successMuhammad Jahanzeb Aamir100% (1)

- Brief History of The Consumer MovementДокумент9 страницBrief History of The Consumer MovementAbdur RakibОценок пока нет

- Store Operations: Submitted By: Submitted To: Vipin (53) Mr. Shashank Mehra PGDRM 2A Faculty of Marketing ResearchДокумент17 страницStore Operations: Submitted By: Submitted To: Vipin (53) Mr. Shashank Mehra PGDRM 2A Faculty of Marketing ResearchmesubbuОценок пока нет

- Competitive Advantages and Strategic Information Systems: ItyofmДокумент13 страницCompetitive Advantages and Strategic Information Systems: Ityofmchoudhary_cuteОценок пока нет

- Shoppers Drug Mart Analysis - ResubmitДокумент10 страницShoppers Drug Mart Analysis - ResubmitPhannarat PhomphadungcheepОценок пока нет

- Br100 SCM - OmДокумент83 страницыBr100 SCM - OmFranciscoRBОценок пока нет

- Behavioral Processes in Marketing ChannelsДокумент36 страницBehavioral Processes in Marketing Channelsavi6192100% (1)

- Homework #2: Due: February 1Документ6 страницHomework #2: Due: February 1cvofoxОценок пока нет

- Visual MerchandisingДокумент2 страницыVisual MerchandisingBhuva_janaОценок пока нет

- Besleri Project ReportДокумент81 страницаBesleri Project ReportTanuj SinghОценок пока нет

- Dhirubhai Ambani 3748 PDFДокумент6 страницDhirubhai Ambani 3748 PDFVinayak ShettyОценок пока нет