Вам также может понравиться

- The Effect of Sales Promotion On Consumer Buying Behavior in An FMCG IndustryДокумент4 страницыThe Effect of Sales Promotion On Consumer Buying Behavior in An FMCG IndustryHemant KumarОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Final BeДокумент8 страницFinal BeHemant KumarОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Excel OutputДокумент143 страницыExcel OutputHemant KumarОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Final Report - International Marketing: Institute of Management Technology Nagpur Trimester V / PGDM (2008-10) / IMДокумент6 страницFinal Report - International Marketing: Institute of Management Technology Nagpur Trimester V / PGDM (2008-10) / IMHemant KumarОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- IMT Nagpur PGDM 2008-2010: Financial MeltdownДокумент35 страницIMT Nagpur PGDM 2008-2010: Financial MeltdownHemant KumarОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- MIS ReportДокумент1 страницаMIS ReportHemant KumarОценок пока нет

- Quantitative Methods: Commodity Excel Macro ModelingДокумент2 страницыQuantitative Methods: Commodity Excel Macro ModelingHemant KumarОценок пока нет

- UPSC CSE PRLIMS-Paper-I-2020-Answer-KeyДокумент1 страницаUPSC CSE PRLIMS-Paper-I-2020-Answer-Keyprg302Оценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- BankДокумент79 страницBankvivek1313Оценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- SBI Clerk Mains Exam PDF February 2024 1Документ223 страницыSBI Clerk Mains Exam PDF February 2024 1Unique SolutionОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Global Financial Crisis and Its Impact On IndiaДокумент23 страницыThe Global Financial Crisis and Its Impact On IndiagdОценок пока нет

- Developer List-9.6.21Документ8 страницDeveloper List-9.6.21Dhananjayan GopinathanОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Quarterly Update - June 2021Документ5 страницQuarterly Update - June 2021Chaitanya Jagarlapudi100% (1)

- Gate ScorecardДокумент1 страницаGate ScorecardRishabh Tripathi100% (1)

- Total BCs-1Документ360 страницTotal BCs-1naina saxenaОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- India Top500Companies2016Документ624 страницыIndia Top500Companies2016Sandeep ElluubhollОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Step by Step Guide: Online Process of APEDA RegistrationДокумент6 страницStep by Step Guide: Online Process of APEDA RegistrationNandaniОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Agra Database Sallery ClassДокумент9 страницAgra Database Sallery ClassvishalОценок пока нет

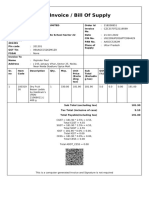

- Tax Invoice / Bill of SupplyДокумент1 страницаTax Invoice / Bill of SupplyCruise Films ProductionsОценок пока нет

- Good Service Tax (GST) Exam Week 3Документ2 страницыGood Service Tax (GST) Exam Week 3M Daiko S PОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Tourism in IndiaДокумент18 страницTourism in IndiaAishОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1091)

- My Final ProjectДокумент68 страницMy Final ProjectSAIОценок пока нет

- Jute Industry AnalysisДокумент56 страницJute Industry AnalysisShaj Han100% (5)

- Hra Cca RuleДокумент5 страницHra Cca Rulebinod12340% (1)

- Fundamental Analysis OfwiproДокумент35 страницFundamental Analysis OfwiproLavina Chandalia100% (3)

- Simone TataДокумент5 страницSimone TataHarry Khanna100% (1)

- Identifying and Addressing Social ProblemsДокумент26 страницIdentifying and Addressing Social ProblemsAniaОценок пока нет

- No 50 - 99 00Документ175 страницNo 50 - 99 00chaudharyaastik93Оценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Sri Shankara Matt: Cummulative Statement 2017Документ28 страницSri Shankara Matt: Cummulative Statement 2017Vijaya BhaskarОценок пока нет

- Nse 20121009Документ33 страницыNse 20121009Dhawan SandeepОценок пока нет

- Ankleshwar ListДокумент11 страницAnkleshwar ListMeghayu AdhvaryuОценок пока нет

- Royal Sundaram Alliance Insurance Company LimitedДокумент2 страницыRoyal Sundaram Alliance Insurance Company Limitedtplinklg1Оценок пока нет

- Coal Industry in Present Scenario in India (Coal Scam)Документ11 страницCoal Industry in Present Scenario in India (Coal Scam)Anoop MishraОценок пока нет

- Henex New Letter 19 NOv 2022Документ21 страницаHenex New Letter 19 NOv 2022Vivek AgОценок пока нет

- Industrial Development in India Since IndependenceДокумент19 страницIndustrial Development in India Since IndependenceRupali RamtekeОценок пока нет

- A Study of Gems and Jewellery ExportДокумент64 страницыA Study of Gems and Jewellery ExportAjay Yadav80% (5)

- Chapter 2 Indian Economy 1950-1990Документ27 страницChapter 2 Indian Economy 1950-1990Ajay pandeyОценок пока нет