Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- SAP CO-PC Product Costing WorkshopДокумент150 страницSAP CO-PC Product Costing Workshopramamurali82% (11)

- zMSQ-02 - Variable & Absorption CostingДокумент11 страницzMSQ-02 - Variable & Absorption CostingKekenn EscabasОценок пока нет

- CostingДокумент11 страницCostingJustine VitorinoОценок пока нет

- Profit Maximization Basic Objective of FirmДокумент4 страницыProfit Maximization Basic Objective of FirmSuriyaprakash Settu50% (2)

- Chap 7 - Flexible Budget, Direct Cost Variance and Management Control - Students NoteДокумент13 страницChap 7 - Flexible Budget, Direct Cost Variance and Management Control - Students NoteZulIzzamreeZolkepliОценок пока нет

- AA025 PYQ 2015 - 2014 (ANS) by SectionДокумент4 страницыAA025 PYQ 2015 - 2014 (ANS) by Sectionnurauniatiqah49Оценок пока нет

- Section 4 - Schedule of Prices - Appendix - B r3Документ14 страницSection 4 - Schedule of Prices - Appendix - B r3Prakash MuthukaruppanОценок пока нет

- Accounting Grade 11 Presentation ECДокумент3 страницыAccounting Grade 11 Presentation ECAnonymous tWAXPAkJd50% (2)

- F5 ATC - Study - Text - June - 2012 PDFДокумент382 страницыF5 ATC - Study - Text - June - 2012 PDFLong Ngo100% (3)

- Prolongation CostДокумент5 страницProlongation CostUsmanОценок пока нет

- EXAMДокумент41 страницаEXAMJoebet Balbin BonifacioОценок пока нет

- PRTC First Answer Key PDFДокумент48 страницPRTC First Answer Key PDFnanabaОценок пока нет

- 14e GNB ch12 SMДокумент67 страниц14e GNB ch12 SMJosé Luismar100% (1)

- Study Note 7.1, Page 470 508Документ39 страницStudy Note 7.1, Page 470 508s4sahithОценок пока нет

- Accounting Standards 32Документ91 страницаAccounting Standards 32bathinisridhar100% (3)

- Study Note - 7.3, Page 535-541Документ7 страницStudy Note - 7.3, Page 535-541s4sahith100% (1)

- Study Note 5.2 (353-378)Документ26 страницStudy Note 5.2 (353-378)s4sahith100% (1)

- Study Note 4.4 Page (264-289)Документ26 страницStudy Note 4.4 Page (264-289)s4sahith75% (24)

- Study Note 4.2, Page 169-197Документ29 страницStudy Note 4.2, Page 169-197s4sahith0% (1)

- Study Note 4.3, Page 198-263Документ66 страницStudy Note 4.3, Page 198-263s4sahithОценок пока нет

- Studdy Note 7Документ42 страницыStuddy Note 7s4sahith100% (1)

- Study Note 4.1, Page 143-168Документ26 страницStudy Note 4.1, Page 143-168s4sahith40% (5)

- Study Note 3, Page 114-142Документ29 страницStudy Note 3, Page 114-142s4sahithОценок пока нет

- Study Note 2.2 Page (80-113)Документ34 страницыStudy Note 2.2 Page (80-113)s4sahithОценок пока нет

- Study Note-1.3, Page 33-46Документ14 страницStudy Note-1.3, Page 33-46s4sahithОценок пока нет

- Study Note 1.2, Page 12 32Документ21 страницаStudy Note 1.2, Page 12 32s4sahithОценок пока нет

- Paper 6: Commercial & Industrial Law and AuditingДокумент6 страницPaper 6: Commercial & Industrial Law and Auditings4sahithОценок пока нет

- Questions Paper 399-406Документ8 страницQuestions Paper 399-406s4sahithОценок пока нет

- 3.3 Workman Ti 198 - 225Документ28 страниц3.3 Workman Ti 198 - 225s4sahithОценок пока нет

- Factories ActДокумент64 страницыFactories ActsubhasishmajumdarОценок пока нет

- Solutions To Chapter 7 Chapter 8Документ10 страницSolutions To Chapter 7 Chapter 8Saurabh SinghОценок пока нет

- ACCA F5 Part A Specialist Cost and Management Accounting TechniquesДокумент5 страницACCA F5 Part A Specialist Cost and Management Accounting TechniquesNguyen Dac ThichОценок пока нет

- Engineering Economy - Lecture 1Документ15 страницEngineering Economy - Lecture 1Patty Seyo0% (1)

- Q.1. Something More Ltd. Is Considering Adding To Its Product Line. After A Lot of DeliberationsДокумент3 страницыQ.1. Something More Ltd. Is Considering Adding To Its Product Line. After A Lot of DeliberationsPrabhmeet SethiОценок пока нет

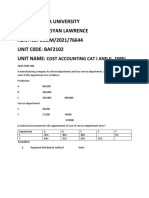

- Baf2102 Cost Accounting CatДокумент5 страницBaf2102 Cost Accounting CatDante MbaeОценок пока нет

- Chap 002Документ7 страницChap 002api-27091131Оценок пока нет

- MS 3413 Activity-Based Costing SystemДокумент5 страницMS 3413 Activity-Based Costing SystemMonica GarciaОценок пока нет

- DM Various SceneriousДокумент15 страницDM Various SceneriousSyed FaizanОценок пока нет

- CostingДокумент3 страницыCostingSukhrut MОценок пока нет

- Assignment Relevant Costing or Incremental AnalysisДокумент3 страницыAssignment Relevant Costing or Incremental AnalysisShannon ElizaldeОценок пока нет

- (FASP - 01) Question Paper Limited Departmental Competitive Examination - 2007 For The Post of Chargeman-Gr - Ii (T) & (NT)Документ9 страниц(FASP - 01) Question Paper Limited Departmental Competitive Examination - 2007 For The Post of Chargeman-Gr - Ii (T) & (NT)murthy gОценок пока нет

- Module (5) Sales Budget, Quotas & TerritoriesДокумент40 страницModule (5) Sales Budget, Quotas & Territorieskrish macОценок пока нет

- Sem 2 B.Com Cost and Management Accounting-IДокумент1 страницаSem 2 B.Com Cost and Management Accounting-IAnimesh BarnwalОценок пока нет

- Cost Accounting Problem 10-10Документ6 страницCost Accounting Problem 10-10Kezia Rev Lim100% (1)

- MB6138Документ23 страницыMB6138Marco Baeza0% (2)

- Contract Costing Sample QuestionsДокумент12 страницContract Costing Sample QuestionsArjan AdhikariОценок пока нет

- Cost Audit ReportДокумент20 страницCost Audit ReportVishesh DwivediОценок пока нет