Вам также может понравиться

- FIN571 Working Capital Simulation WK6Документ7 страницFIN571 Working Capital Simulation WK6Dina100% (3)

- National Geographic SocietyДокумент3 страницыNational Geographic SocietyallanОценок пока нет

- Turnaround Plan For Linens N ThingsДокумент15 страницTurnaround Plan For Linens N ThingsTinakhaladze100% (1)

- Working Capital Simulation - Managing Growth AssignmentДокумент9 страницWorking Capital Simulation - Managing Growth AssignmentMySpam100% (1)

- Barc - Citi - 500.4Документ2 страницыBarc - Citi - 500.4Benjamin Benji Bonilla Cocoma100% (1)

- WESCOДокумент15 страницWESCOPuneet Arora100% (1)

- Walker & CompanyДокумент9 страницWalker & Companyer4sallОценок пока нет

- Embezzlement at Koss Over 12 Years!Документ8 страницEmbezzlement at Koss Over 12 Years!kengsheongtehОценок пока нет

- ch16 KeyДокумент5 страницch16 Keyrocksartha100% (1)

- Beyond Survival: Eight Key Imperatives For Financial Services in The Post-Crisis EraДокумент8 страницBeyond Survival: Eight Key Imperatives For Financial Services in The Post-Crisis EraBrazil offshore jobsОценок пока нет

- Arlington Value's 2013 LetterДокумент7 страницArlington Value's 2013 LetterValueWalk100% (7)

- Avon Products Inc - 2009Документ22 страницыAvon Products Inc - 2009Charisse L. SarateОценок пока нет

- BAIN BRIEF The Return-Of-corporate Strategy in BankingДокумент12 страницBAIN BRIEF The Return-Of-corporate Strategy in BankingMBA MBAОценок пока нет

- Sample Consulting Firm B PlanДокумент18 страницSample Consulting Firm B PlanmskrierОценок пока нет

- 2012 Financial Services - Retail Banking Industry Perspective2012Документ4 страницы2012 Financial Services - Retail Banking Industry Perspective2012Brazil offshore jobsОценок пока нет

- Reflection Paper I (Costco, Financial Health, Jones)Документ3 страницыReflection Paper I (Costco, Financial Health, Jones)xsimplyxjesssОценок пока нет

- BAIN Brief - Divide and Conquer - A Guide To Winning SME Banking StrategiesДокумент12 страницBAIN Brief - Divide and Conquer - A Guide To Winning SME Banking Strategiesapritul3539Оценок пока нет

- Harvard CasesДокумент66 страницHarvard CasesAyush Singhal100% (2)

- Customer Retention Practices A Case of Cal BankДокумент88 страницCustomer Retention Practices A Case of Cal BankCollins Brobbey50% (2)

- Problem StatementДокумент3 страницыProblem StatementLeo Pratama GaniОценок пока нет

- Harvard CasesДокумент66 страницHarvard CasesAkshay Goel100% (1)

- Eastboro Case Write Up For Presentation1Документ4 страницыEastboro Case Write Up For Presentation1Paula Elaine ThorpeОценок пока нет

- Research Company IN Strategic ManagementДокумент9 страницResearch Company IN Strategic ManagementVincent SarmientoОценок пока нет

- Swot AnalysisДокумент3 страницыSwot AnalysisSayali DiwateОценок пока нет

- Groupon Inc Case AnalysisДокумент8 страницGroupon Inc Case Analysispatrick wafulaОценок пока нет

- High Performance: GrowthДокумент11 страницHigh Performance: GrowthL.T. (Tom) HallОценок пока нет

- Research Papers On Finance and Investments Special TopicsДокумент5 страницResearch Papers On Finance and Investments Special TopicsadgecibkfОценок пока нет

- Costco SwotДокумент13 страницCostco SwotHolly SantanaОценок пока нет

- 2014BankingIndustryOutlook DeloitteДокумент20 страниц2014BankingIndustryOutlook DeloittelapogkОценок пока нет

- SWOT Analysis of IndustryДокумент12 страницSWOT Analysis of IndustryZahidur RezaОценок пока нет

- GPCC 07 Case-ReportДокумент5 страницGPCC 07 Case-ReportJames Ryan AlzonaОценок пока нет

- Marks and Spencer PLCДокумент8 страницMarks and Spencer PLCoptimus457Оценок пока нет

- Customer Relationship Management: Safe MethodsДокумент10 страницCustomer Relationship Management: Safe Methodsjason tatumОценок пока нет

- 2011 Annual ReportДокумент162 страницы2011 Annual ReportNooreza PeerooОценок пока нет

- Letter ShareholdersДокумент7 страницLetter ShareholdersRich0087Оценок пока нет

- Research Paper Topics in Banking and FinanceДокумент7 страницResearch Paper Topics in Banking and Finances0l1nawymym3100% (1)

- Chapter 12-14 A FixedДокумент162 страницыChapter 12-14 A FixedDaniel Luke Higgins0% (2)

- Goldman Sachs 2012 Annual ReportДокумент244 страницыGoldman Sachs 2012 Annual ReportddubyaОценок пока нет

- GoldmanДокумент244 страницыGoldmanC.Оценок пока нет

- A New Era of Customer Expectation - Global Consumer Banking SurveyДокумент56 страницA New Era of Customer Expectation - Global Consumer Banking SurveyRahul RajputОценок пока нет

- WESCOДокумент5 страницWESCOGargi VermaОценок пока нет

- Module in Financial Management - 03Документ17 страницModule in Financial Management - 03Angelo DomingoОценок пока нет

- Content of The Strategic PlanДокумент14 страницContent of The Strategic PlanMarjorie MercadoОценок пока нет

- Financial Evaluation Report With SampleДокумент12 страницFinancial Evaluation Report With SamplemaidangphapОценок пока нет

- Oh So LocalДокумент40 страницOh So LocalfredgalleyОценок пока нет

- MC Moelis InitiatingДокумент27 страницMC Moelis InitiatingRCОценок пока нет

- Managing GrowthДокумент7 страницManaging GrowthChitrakalpa SenОценок пока нет

- FNSACC501 Assessment 2Документ6 страницFNSACC501 Assessment 2Daranee TrakanchanОценок пока нет

- Factors Influencing Customer'S Satisfaction Towards Beverages of PepsicoДокумент32 страницыFactors Influencing Customer'S Satisfaction Towards Beverages of PepsicoBeverlie Tabañag100% (1)

- Corporate Communication PlanДокумент13 страницCorporate Communication Planapi-401128290Оценок пока нет

- ENG TranslationДокумент3 страницыENG TranslationTamar PkhakadzeОценок пока нет

- Final ProjectДокумент10 страницFinal ProjectAmna AhmedОценок пока нет

- Swot AnalysisДокумент4 страницыSwot AnalysisAhmad ShahОценок пока нет

- Stuck in NeutralДокумент8 страницStuck in NeutralMike KarlinsОценок пока нет

- Financing A New Venture Trough and Initial Public Offering (IPO)Документ32 страницыFinancing A New Venture Trough and Initial Public Offering (IPO)Manthan LalanОценок пока нет

- Dec 2012 NewsletterpdfДокумент4 страницыDec 2012 NewsletterpdfRich PirrottaОценок пока нет

- Being The Best Thriving Not Just SurvivingДокумент8 страницBeing The Best Thriving Not Just SurvivingBrazil offshore jobsОценок пока нет

- DividendsДокумент5 страницDividendsMinettaLaneОценок пока нет

- The Well-Timed Strategy (Review and Analysis of Navarro's Book)От EverandThe Well-Timed Strategy (Review and Analysis of Navarro's Book)Оценок пока нет

- Implementing Beyond Budgeting: Unlocking the Performance PotentialОт EverandImplementing Beyond Budgeting: Unlocking the Performance PotentialРейтинг: 5 из 5 звезд5/5 (1)

- Financial Literacy for Managers: Finance and Accounting for Better Decision-MakingОт EverandFinancial Literacy for Managers: Finance and Accounting for Better Decision-MakingРейтинг: 5 из 5 звезд5/5 (1)

- A Complete Pool Supply Store Business Plan: A Key Part Of How To Start A Pool & Spa Supply BusinessОт EverandA Complete Pool Supply Store Business Plan: A Key Part Of How To Start A Pool & Spa Supply BusinessОценок пока нет

- Online Payment SystemДокумент27 страницOnline Payment SystemVijetha bhat100% (1)

- Study On Customer Perception Towards E-Banking Services: A Summer Training Project ReportДокумент56 страницStudy On Customer Perception Towards E-Banking Services: A Summer Training Project ReportahenmakkОценок пока нет

- Questionnaire: Brand Loyalty and Relationship Marketing in State Bank of India's Banking System. IДокумент6 страницQuestionnaire: Brand Loyalty and Relationship Marketing in State Bank of India's Banking System. IAanand SharmaОценок пока нет

- Letter To All Member Banks of SLBC (UP)Документ1 страницаLetter To All Member Banks of SLBC (UP)dadan vishwakarmaОценок пока нет

- PldtbillДокумент4 страницыPldtbilljen marquesОценок пока нет

- FY19 Global MNC Plan FinalДокумент21 страницаFY19 Global MNC Plan FinalMARTHA HDEZОценок пока нет

- Demat Acount TradebullsДокумент23 страницыDemat Acount TradebullsMihir SenОценок пока нет

- Mozambique Tourist Visa ApplicationДокумент5 страницMozambique Tourist Visa ApplicationMaria José Andrade PadillaОценок пока нет

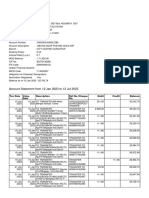

- Account Statement From 12 Jan 2023 To 12 Jul 2023Документ10 страницAccount Statement From 12 Jan 2023 To 12 Jul 2023SouravDeyОценок пока нет

- A Cheque Is A DocumentДокумент15 страницA Cheque Is A Documentmi06bba030Оценок пока нет

- Comparative Financial Statement Analysis of The Big Three Banks Operating in Finland 2015-2016Документ49 страницComparative Financial Statement Analysis of The Big Three Banks Operating in Finland 2015-2016Eugene Rugo AОценок пока нет

- CA2 Group Assignment CompleteДокумент14 страницCA2 Group Assignment CompleteCatherine Yapp100% (1)

- Credit CardДокумент15 страницCredit Cardsrdagpnt100% (1)

- SBI Investment ProductsДокумент20 страницSBI Investment ProductssaravananОценок пока нет

- Yared vs. LBPДокумент2 страницыYared vs. LBPRobОценок пока нет

- Gross Income NotesДокумент20 страницGross Income NotesCheng OlayvarОценок пока нет

- Import Form 2018Документ6 страницImport Form 2018tejasg82100% (2)

- Green Banking in Asia + 3: Edi SetijawanДокумент12 страницGreen Banking in Asia + 3: Edi SetijawanArief MizanОценок пока нет

- RBA APU PPT - OJK 16 April 2018 PDFДокумент46 страницRBA APU PPT - OJK 16 April 2018 PDFBunnyОценок пока нет

- Generated Leads For State FarmДокумент12 страницGenerated Leads For State Farmapi-19783206Оценок пока нет

- Executive Director Senior Center in Tallahassee FL Resume Rodney BigelowДокумент2 страницыExecutive Director Senior Center in Tallahassee FL Resume Rodney BigelowRodneyBigelowОценок пока нет

- Company LawДокумент15 страницCompany Lawpreetibajaj100% (2)

- 72-Finman Assurance Corporation vs. Court of Appeals, 361 SCRA 514 (2001)Документ7 страниц72-Finman Assurance Corporation vs. Court of Appeals, 361 SCRA 514 (2001)Jopan SJОценок пока нет

- Kai Green Chest 2.0Документ12 страницKai Green Chest 2.0Gaurav MalikОценок пока нет

- Confirmation and Acknowledgment - OfW Signing The Docs v2.0Документ1 страницаConfirmation and Acknowledgment - OfW Signing The Docs v2.0Carlo Josef TabulogОценок пока нет

- SBI Savings Account Opening Form For Resident IndividualsДокумент8 страницSBI Savings Account Opening Form For Resident Individualsssbaidya75% (12)

- 997SДокумент404 страницы997SZeeshan AhmedОценок пока нет