Вам также может понравиться

- Case Study of Stryker CorporationДокумент5 страницCase Study of Stryker CorporationYulfaizah Mohd Yusoff100% (6)

- Stryker CaseДокумент3 страницыStryker Caseionus_2003100% (4)

- Stryker Corporation - Assignment 22 March 17Документ4 страницыStryker Corporation - Assignment 22 March 17Venkatesh K67% (6)

- Vehicle Lease Agreement TEMPLATEДокумент5 страницVehicle Lease Agreement TEMPLATEyassercarloman100% (1)

- Nucleon Case Solution - WorkingДокумент2 страницыNucleon Case Solution - WorkingRitik MaheshwariОценок пока нет

- Tittle of AssignmentДокумент3 страницыTittle of AssignmentRukkie MohammedОценок пока нет

- Case Study of Stryker CorporationДокумент5 страницCase Study of Stryker CorporationYulfaizah Mohd Yusoff40% (5)

- Import Distributors, Inc. : Case 26-1Документ2 страницыImport Distributors, Inc. : Case 26-1NishaОценок пока нет

- Depreciation Singapore & Delta Airline CaseДокумент1 страницаDepreciation Singapore & Delta Airline CaseNavendu Rai100% (1)

- Stryker Corporation PPT SlidesДокумент13 страницStryker Corporation PPT SlidesZahid UsmanОценок пока нет

- BDO v. Crandell, Crandell Answer and CounterclaimДокумент44 страницыBDO v. Crandell, Crandell Answer and CounterclaimAdrienne GonzalezОценок пока нет

- Lipman Bottle Company Case Analysis Group1Документ13 страницLipman Bottle Company Case Analysis Group1Shubham Nigam100% (1)

- Mcs PelicanДокумент6 страницMcs PelicanJasmina Stanojevich100% (1)

- Mystic SportsДокумент34 страницыMystic SportshelloОценок пока нет

- Nview SolnДокумент6 страницNview SolnShashikant SagarОценок пока нет

- This Spreadsheet Supports STUDENT Analysis of The Case "Bob's Baloney" (UVA-F-1942)Документ4 страницыThis Spreadsheet Supports STUDENT Analysis of The Case "Bob's Baloney" (UVA-F-1942)LAWZ1017Оценок пока нет

- People v. Lamahang CASE DIGESTДокумент2 страницыPeople v. Lamahang CASE DIGESTRalson Mangulabnan Hernandez100% (1)

- StrykerДокумент10 страницStrykerVeer SahaniОценок пока нет

- StrykerДокумент15 страницStrykerManu Arora17% (6)

- Caso 2 Excel 1Документ8 страницCaso 2 Excel 1Carolina NunezОценок пока нет

- Mercury Athletic Footwear: Joel L. Heilprin Harvard Business School © 59 Street Partners LLCДокумент15 страницMercury Athletic Footwear: Joel L. Heilprin Harvard Business School © 59 Street Partners LLCkarthikawarrierОценок пока нет

- Lipman Bottle CompanyДокумент20 страницLipman Bottle CompanySaswata BanerjeeОценок пока нет

- Stryker Case - BriefДокумент4 страницыStryker Case - BriefCorinne Williams0% (4)

- Case 5 Joan Holtz Answer KeyДокумент5 страницCase 5 Joan Holtz Answer KeyAashima GroverОценок пока нет

- This Study Resource Was: Forner CarpetДокумент4 страницыThis Study Resource Was: Forner CarpetLi CarinaОценок пока нет

- Too Soon To IPO?: Case Study AnalysisДокумент13 страницToo Soon To IPO?: Case Study Analysispratz1996100% (1)

- ABC QuestionsДокумент14 страницABC QuestionsLara Lewis Achilles0% (1)

- Case 5-3Документ2 страницыCase 5-3ragil1988Оценок пока нет

- Amerbran Company A Final1Документ6 страницAmerbran Company A Final1Rio TanОценок пока нет

- Amerbran Company (B) SolutionДокумент10 страницAmerbran Company (B) SolutionHeruCakraОценок пока нет

- Barilla - CaseДокумент14 страницBarilla - CaseSevana YadegarianОценок пока нет

- As Sig Ment 2 PrivateДокумент138 страницAs Sig Ment 2 PrivateluisОценок пока нет

- Case SolutionДокумент20 страницCase SolutionKhurram Sadiq (Father Name:Muhammad Sadiq)Оценок пока нет

- Executive SummaryДокумент17 страницExecutive SummaryAzizki WanieОценок пока нет

- Chemalite Cash Flow StatementДокумент2 страницыChemalite Cash Flow Statementrishika rshОценок пока нет

- Garanti Payment Systems:: Digital Transformation StrategyДокумент12 страницGaranti Payment Systems:: Digital Transformation StrategySwarnajit SahaОценок пока нет

- Cafe Monte BiancoДокумент21 страницаCafe Monte BiancoWilliam Torrez OrozcoОценок пока нет

- Cost Accounting ReportДокумент12 страницCost Accounting ReportSYED WAFIОценок пока нет

- Seligram, IncДокумент5 страницSeligram, IncAto SumartoОценок пока нет

- Target CorporationДокумент20 страницTarget CorporationAditiPatilОценок пока нет

- Case Study Coca Cola Vs PepsiДокумент13 страницCase Study Coca Cola Vs PepsiAlyaYusof50% (2)

- Dan ShuiДокумент12 страницDan ShuiSai KiranОценок пока нет

- Case Lewis CorporationДокумент2 страницыCase Lewis CorporationSumit VakhariaОценок пока нет

- Salem Analytics Panera Bread Company Final ReportДокумент31 страницаSalem Analytics Panera Bread Company Final ReportCecille TaguiamОценок пока нет

- Hospital SupplyДокумент3 страницыHospital SupplyJeanne Madrona100% (1)

- Report 2Документ4 страницыReport 2Trang PhamОценок пока нет

- Toyota Case StudyДокумент19 страницToyota Case StudyDat BoiОценок пока нет

- Baldwin Bicycle CompanyДокумент19 страницBaldwin Bicycle CompanyMannu83Оценок пока нет

- The ALLTEL Pavilion Case - Strategy and CVP Analysis PDFДокумент7 страницThe ALLTEL Pavilion Case - Strategy and CVP Analysis PDFPritam Kumar NayakОценок пока нет

- Cash Flow Statements IIДокумент7 страницCash Flow Statements IIChris RessoОценок пока нет

- Home Depot Case Group 2Документ10 страницHome Depot Case Group 2Rishabh TyagiОценок пока нет

- Patagonia CaseДокумент1 страницаPatagonia CaseArmyandre Rossel SanchezОценок пока нет

- O.M Scott and Sons Case SummaryДокумент2 страницыO.M Scott and Sons Case SummarySUSHMITA SHUBHAMОценок пока нет

- Daktronics E Dividend Policy in 2010Документ26 страницDaktronics E Dividend Policy in 2010IBRAHIM KHANОценок пока нет

- Case Study: Delwarca Software Remote Support UnitДокумент2 страницыCase Study: Delwarca Software Remote Support UnitrjОценок пока нет

- Chap 026Документ17 страницChap 026Neetu Rajaraman100% (2)

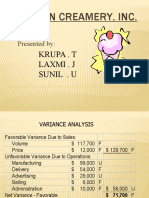

- Boston Creamery CaseДокумент9 страницBoston Creamery Caselion_heart3001100% (1)

- Vaibhav Maheshwari Merrimack Tractors 2011pgp926Документ3 страницыVaibhav Maheshwari Merrimack Tractors 2011pgp926studvabzОценок пока нет

- Millichem Solution XДокумент6 страницMillichem Solution XMuhammad JunaidОценок пока нет

- Forest Laboratories, Inc.Документ4 страницыForest Laboratories, Inc.sommer_ronald5741Оценок пока нет

- Journal of Finance Case Research: Volume 9 2007 Number 2Документ8 страницJournal of Finance Case Research: Volume 9 2007 Number 2Robert IronsОценок пока нет

- FRA Assignment MYДокумент4 страницыFRA Assignment MYAminaОценок пока нет

- DIY InvestingДокумент2 страницыDIY Investingsommer_ronald5741Оценок пока нет

- 2010 Win Some Lose SomeДокумент2 страницы2010 Win Some Lose Somesommer_ronald5741Оценок пока нет

- Starting Lineup For 2011Документ3 страницыStarting Lineup For 2011sommer_ronald5741Оценок пока нет

- LubrizolДокумент2 страницыLubrizolsommer_ronald5741Оценок пока нет

- Inter Digital ProfileДокумент2 страницыInter Digital Profilesommer_ronald5741Оценок пока нет

- Tractor SupplyДокумент2 страницыTractor Supplysommer_ronald5741Оценок пока нет

- GT SolarДокумент2 страницыGT Solarsommer_ronald5741Оценок пока нет

- ComTech Telecom SummaryДокумент3 страницыComTech Telecom Summarysommer_ronald5741Оценок пока нет

- Astrazeneca SummaryДокумент1 страницаAstrazeneca Summarysommer_ronald5741Оценок пока нет

- Hawkins IncДокумент2 страницыHawkins Incsommer_ronald5741Оценок пока нет

- Sorl Auto Parts Inc. - No Stopping HereДокумент2 страницыSorl Auto Parts Inc. - No Stopping Heresommer_ronald5741Оценок пока нет

- Techne Corporation (TECH) - Good Risk/Reward PropositionДокумент8 страницTechne Corporation (TECH) - Good Risk/Reward Propositionsommer_ronald5741Оценок пока нет

- AIR T AnalysisДокумент5 страницAIR T Analysissommer_ronald5741Оценок пока нет

- Amdocs LTDДокумент4 страницыAmdocs LTDsommer_ronald5741Оценок пока нет

- Forest Laboratories, Inc.Документ4 страницыForest Laboratories, Inc.sommer_ronald5741Оценок пока нет

- SnapLogic - Market Leader 3 Industry Reports Jan 2019Документ5 страницSnapLogic - Market Leader 3 Industry Reports Jan 2019dharmsmart19Оценок пока нет

- Complaint Affidavit Pag Ibig FundДокумент3 страницыComplaint Affidavit Pag Ibig FundHaider De LeonОценок пока нет

- Final Managerial AccountingДокумент8 страницFinal Managerial Accountingdangthaibinh0312Оценок пока нет

- DRAFT FY2014-FY2018 Transportation Capital Investment PlanДокумент117 страницDRAFT FY2014-FY2018 Transportation Capital Investment PlanMassLiveОценок пока нет

- Symbiosis Law School, PuneДокумент6 страницSymbiosis Law School, PuneVarun MenonОценок пока нет

- Bank Reconciliation StatementДокумент5 страницBank Reconciliation StatementjithaОценок пока нет

- Chapter 1: Introduction: 1. Distribution of Powers To Local Government As Limitation To Political AuthorityДокумент33 страницыChapter 1: Introduction: 1. Distribution of Powers To Local Government As Limitation To Political AuthorityJoseph GabutinaОценок пока нет

- JibranДокумент15 страницJibranMuhammad Qamar ShehzadОценок пока нет

- G.R. No. 68166 February 12, 1997 Heirs of Emiliano Navarro, Petitioner, Intermediate Appellate Court & Heirs of Sinforoso Pascual, RespondentsДокумент3 страницыG.R. No. 68166 February 12, 1997 Heirs of Emiliano Navarro, Petitioner, Intermediate Appellate Court & Heirs of Sinforoso Pascual, RespondentssophiabarnacheaОценок пока нет

- Account Summary Contact Us: Ms Angela Munro 201 3159 Shelbourne ST Victoria BC V8T 3A5Документ4 страницыAccount Summary Contact Us: Ms Angela Munro 201 3159 Shelbourne ST Victoria BC V8T 3A5Angela MunroОценок пока нет

- Vocabulary Monologue Your JobДокумент2 страницыVocabulary Monologue Your JobjoseluiscurriОценок пока нет

- ES MT 0106 - REV1.30 - 24122019 - 6021282 DIAM 4100 Rev 1 30 - EN 2Документ64 страницыES MT 0106 - REV1.30 - 24122019 - 6021282 DIAM 4100 Rev 1 30 - EN 2Paix AvousОценок пока нет

- Answer: Appellate-Procedure-Codified-11-September-2019.Pdf?Ch1T.Thkbkbo74Vls5Tgg0Zvrf3PckgwДокумент5 страницAnswer: Appellate-Procedure-Codified-11-September-2019.Pdf?Ch1T.Thkbkbo74Vls5Tgg0Zvrf3PckgwWilliam JamesОценок пока нет

- YehДокумент3 страницыYehDeneree Joi EscotoОценок пока нет

- Case 20Документ6 страницCase 20Chelle Rico Fernandez BOОценок пока нет

- PACQUIAOebookДокумент150 страницPACQUIAOebookpugnar100% (1)

- 1 Fundamental Concepts of Fluid Mechanics For Mine VentilationДокумент29 страниц1 Fundamental Concepts of Fluid Mechanics For Mine VentilationRiswan RiswanОценок пока нет

- Sample Blogger Agreement-14Документ3 страницыSample Blogger Agreement-14api-18133493Оценок пока нет

- Shrimp Specialists V Fuji-TriumphДокумент2 страницыShrimp Specialists V Fuji-TriumphDeaОценок пока нет

- Executive Summary: Source of Commission: PMA Date of Commission: 16 March 2009 Date of Rank: 16 March 2016Документ3 страницыExecutive Summary: Source of Commission: PMA Date of Commission: 16 March 2009 Date of Rank: 16 March 2016Yanna PerezОценок пока нет

- Learning Module: Community Colleges of The PhilippinesДокумент41 страницаLearning Module: Community Colleges of The PhilippinesGianina De LeonОценок пока нет

- Chapter 17 - Supply Chains (17th Edition)Документ23 страницыChapter 17 - Supply Chains (17th Edition)meeshakeОценок пока нет

- Intermediate To Advance Electronics Troubleshooting (March 2023) IkAДокумент7 страницIntermediate To Advance Electronics Troubleshooting (March 2023) IkAArenum MustafaОценок пока нет

- Activity 2:: Date Account Titles and Explanation P.R. Debit CreditДокумент2 страницыActivity 2:: Date Account Titles and Explanation P.R. Debit Creditemem resuentoОценок пока нет

- Fares Alhammadi 10BB Death Penatly Argumentative EssayДокумент7 страницFares Alhammadi 10BB Death Penatly Argumentative EssayFares AlhammadiОценок пока нет

- Basis OF Judicial Clemency AND Reinstatement To The Practice of LawДокумент4 страницыBasis OF Judicial Clemency AND Reinstatement To The Practice of LawPrincess Rosshien HortalОценок пока нет

- MMD Political Overview CroatiaДокумент3 страницыMMD Political Overview CroatiaMmd SEE100% (2)

- A Guide To: Commons in ResearchДокумент7 страницA Guide To: Commons in ResearchAna PaulaОценок пока нет