Вам также может понравиться

- Chapter 10 5eДокумент31 страницаChapter 10 5eChrissa Marie VienteОценок пока нет

- InstructionsДокумент36 страницInstructionsjhouvan50% (6)

- Solution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 9Документ46 страницSolution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 9jasperkennedy086% (22)

- ABC CostingДокумент28 страницABC CostingKiraYamatoОценок пока нет

- Cost Acctg ReviewerДокумент106 страницCost Acctg ReviewerGregory Chase83% (6)

- Cost Accounting CHPTR 2Документ6 страницCost Accounting CHPTR 2Keisha Lynch75% (4)

- 222Документ3 страницы222Carlo ParasОценок пока нет

- Blue Mountain Coffee ADBUDG ME For Excel Case Version 1.0.5Документ8 страницBlue Mountain Coffee ADBUDG ME For Excel Case Version 1.0.5cerky6972100% (1)

- Toán Ứng Dụng Giáo TrìnhДокумент123 страницыToán Ứng Dụng Giáo TrìnhHoàng SơnОценок пока нет

- Cfa Level 1 Mock TestДокумент34 страницыCfa Level 1 Mock TestAnonymous P1xUTHstHT100% (5)

- 209384Документ14 страниц209384Jayson HoangОценок пока нет

- Chapter Eleven: Standard Costs and Variance AnalysisДокумент43 страницыChapter Eleven: Standard Costs and Variance AnalysisnnonscribdОценок пока нет

- COMA - 04 Variaance PDFДокумент49 страницCOMA - 04 Variaance PDFAbhishekОценок пока нет

- Standard Cost Variance AnalysisДокумент48 страницStandard Cost Variance AnalysisLight knightОценок пока нет

- Multiple ChoiceДокумент15 страницMultiple ChoiceChristian Kim MedranoОценок пока нет

- Multiple ChoiceДокумент15 страницMultiple ChoiceChristian Kim MedranoОценок пока нет

- STD CSTGДокумент42 страницыSTD CSTGsanam20191Оценок пока нет

- CH 11Документ48 страницCH 11Amanda SaffouriОценок пока нет

- Standard Costing: A Standard Cost Is A Carefully - Unit Cist Which Is Prepared For Each Cost UnitДокумент23 страницыStandard Costing: A Standard Cost Is A Carefully - Unit Cist Which Is Prepared For Each Cost UnitHarshОценок пока нет

- Standard Costing and Variance AnalysisДокумент7 страницStandard Costing and Variance AnalysisNicko CrisoloОценок пока нет

- TEST 1 TRUE/FALSE Write TRUE If The Statement Is Correct and FALSE If It Is Wrong. Avoid ErasuresДокумент30 страницTEST 1 TRUE/FALSE Write TRUE If The Statement Is Correct and FALSE If It Is Wrong. Avoid ErasuresSuga kpopОценок пока нет

- God of AllДокумент9 страницGod of AllRaphael Dean Vitug DesturaОценок пока нет

- TB ch11Документ15 страницTB ch11Pola PolzОценок пока нет

- Assignment 3 - Standard CostingДокумент4 страницыAssignment 3 - Standard CostingJayhan PalmonesОценок пока нет

- Quiz Standard Costing 2222012 PrintДокумент52 страницыQuiz Standard Costing 2222012 PrintexgayssОценок пока нет

- SCM Discussion 6Документ10 страницSCM Discussion 6M4ZONSK1E OfficialОценок пока нет

- Chap 010Документ100 страницChap 010hertzberg 1Оценок пока нет

- Cost Accounting Raiborn and Kinney Solman Chapter 07 CompressДокумент35 страницCost Accounting Raiborn and Kinney Solman Chapter 07 CompressMa. Paula JabunganОценок пока нет

- Chapter 16 - AnswerДокумент14 страницChapter 16 - AnswerMarlon A. RodriguezОценок пока нет

- Standard Cost and Operating Performance MeasuresДокумент3 страницыStandard Cost and Operating Performance MeasuresShaik Hasnat IsfarОценок пока нет

- Cost Accounting (1) AnswersДокумент5 страницCost Accounting (1) AnswersMelissa Kayla ManiulitОценок пока нет

- Chapter 8 Standard Cost Accounting CompressДокумент13 страницChapter 8 Standard Cost Accounting CompressJohn Kenneth Jarce CaminoОценок пока нет

- Standard Costing PDFДокумент36 страницStandard Costing PDFRamesh ShriОценок пока нет

- Quizz C3Документ10 страницQuizz C3Thanh NgânОценок пока нет

- Quiz 2.2Документ6 страницQuiz 2.2els emsОценок пока нет

- Std. Cost & Var 2014Документ10 страницStd. Cost & Var 2014Aj de CastroОценок пока нет

- Standard-Costing-Review-Material FinalДокумент8 страницStandard-Costing-Review-Material Finaljoneth.duenasОценок пока нет

- Chapter 10 SolutionsДокумент68 страницChapter 10 SolutionsMasha LankОценок пока нет

- Standard Costing and Variance AnalysisДокумент13 страницStandard Costing and Variance AnalysisSigei Leonard100% (1)

- Standard Costing Summary For CA Inter, CMA Inter, CS ExecutiveДокумент5 страницStandard Costing Summary For CA Inter, CMA Inter, CS Executivecd classes100% (1)

- Module 2 Sub Mod 2 Standard Costing and Material Variance FinalДокумент31 страницаModule 2 Sub Mod 2 Standard Costing and Material Variance Finalmaheshbendigeri5945Оценок пока нет

- Chapter 9Документ8 страницChapter 9AbdulAzeemОценок пока нет

- Accg200 L12Документ11 страницAccg200 L12Nikita Singh DhamiОценок пока нет

- Product Cost - CostingДокумент84 страницыProduct Cost - CostingpankajmayОценок пока нет

- 2the NotesДокумент85 страниц2the Notesnairpooja94Оценок пока нет

- CLASSIFICATION OF COSTS: ManufacturingДокумент84 страницыCLASSIFICATION OF COSTS: Manufacturingbhartu10Оценок пока нет

- Variance AnalysisДокумент31 страницаVariance AnalysisGift ChaliОценок пока нет

- Colegio de San Gabriel Arcangel: Learning Module in Strategic Cost Management Unit TitleДокумент8 страницColegio de San Gabriel Arcangel: Learning Module in Strategic Cost Management Unit TitleC XОценок пока нет

- Study Material: Management Accounting Bba Sem ViДокумент42 страницыStudy Material: Management Accounting Bba Sem ViAman MallОценок пока нет

- Analysis of Variances From Standard Costs - Solutions PDFДокумент39 страницAnalysis of Variances From Standard Costs - Solutions PDFHikariОценок пока нет

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageОт EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageРейтинг: 5 из 5 звезд5/5 (1)

- Finance for Non-Financiers 2: Professional FinancesОт EverandFinance for Non-Financiers 2: Professional FinancesОценок пока нет

- Measuring and Marking Metals for Home Machinists: Accurate Techniques for the Small ShopОт EverandMeasuring and Marking Metals for Home Machinists: Accurate Techniques for the Small ShopРейтинг: 4 из 5 звезд4/5 (1)

- Practical Guide To Production Planning & Control [Revised Edition]От EverandPractical Guide To Production Planning & Control [Revised Edition]Рейтинг: 1 из 5 звезд1/5 (1)

- Business Ratios and Formulas: A Comprehensive GuideОт EverandBusiness Ratios and Formulas: A Comprehensive GuideРейтинг: 3 из 5 звезд3/5 (1)

- Gen Banking LawДокумент11 страницGen Banking LawDaniel John Cañares LegaspiОценок пока нет

- Scatter Plot: 10000 F (X) 7.6826983136x 2 - 10550.0630855715x + 10546.0342910681 R 0.9999999728Документ6 страницScatter Plot: 10000 F (X) 7.6826983136x 2 - 10550.0630855715x + 10546.0342910681 R 0.9999999728Daniel John Cañares LegaspiОценок пока нет

- The Trans-Pacific Partnership (Trade of Goods)Документ6 страницThe Trans-Pacific Partnership (Trade of Goods)Daniel John Cañares LegaspiОценок пока нет

- Chapter 5 Professional AudiДокумент35 страницChapter 5 Professional AudiDaniel John Cañares Legaspi100% (1)

- Bank Secrecy LawДокумент2 страницыBank Secrecy LawDaniel John Cañares LegaspiОценок пока нет

- Monday (November 24) : Men's& Women's Volleyball 12:30PM-5:00PM GYMДокумент2 страницыMonday (November 24) : Men's& Women's Volleyball 12:30PM-5:00PM GYMDaniel John Cañares LegaspiОценок пока нет

- City University of PasayДокумент2 страницыCity University of PasayDaniel John Cañares LegaspiОценок пока нет

- BEHASCIДокумент2 страницыBEHASCIDaniel John Cañares LegaspiОценок пока нет

- Certificate of Recognition: Charrevie M. TingsonДокумент2 страницыCertificate of Recognition: Charrevie M. TingsonDaniel John Cañares LegaspiОценок пока нет

- Candidates For Internship Program For 1st Term AY 2015-2016Документ1 страницаCandidates For Internship Program For 1st Term AY 2015-2016Daniel John Cañares LegaspiОценок пока нет

- Federatio N Year: Prof. Osler T AquinoДокумент1 страницаFederatio N Year: Prof. Osler T AquinoDaniel John Cañares LegaspiОценок пока нет

- 23 Marcon, Louise Margarette 24 Millar, AllyssaДокумент2 страницы23 Marcon, Louise Margarette 24 Millar, AllyssaDaniel John Cañares LegaspiОценок пока нет

- Chapter 3. Decision Analysis Section 3.1. Decision Trees With Conditional ProbabilitiesДокумент12 страницChapter 3. Decision Analysis Section 3.1. Decision Trees With Conditional ProbabilitiesDaniel John Cañares LegaspiОценок пока нет

- Partnership ReviewerДокумент21 страницаPartnership ReviewerDaniel John Cañares Legaspi100% (1)

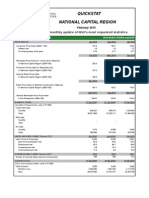

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsДокумент3 страницыQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiОценок пока нет

- PhotoshootДокумент1 страницаPhotoshootDaniel John Cañares LegaspiОценок пока нет

- Del Mundo Q and AДокумент2 страницыDel Mundo Q and ADaniel John Cañares LegaspiОценок пока нет

- SMCДокумент12 страницSMCDaniel John Cañares LegaspiОценок пока нет

- Sampoerna - Marketing Plan-Gc BonchonДокумент13 страницSampoerna - Marketing Plan-Gc BonchonDaniel John Cañares Legaspi50% (2)

- Federatio N Year: Prof. Osler T AquinoДокумент2 страницыFederatio N Year: Prof. Osler T AquinoDaniel John Cañares LegaspiОценок пока нет

- House Rules: 1. English Only PolicyДокумент2 страницыHouse Rules: 1. English Only PolicyDaniel John Cañares LegaspiОценок пока нет

- Grand Academic Congress 2015 (Responses) - v7Документ14 страницGrand Academic Congress 2015 (Responses) - v7Daniel John Cañares LegaspiОценок пока нет

- APS For Peer MentoringДокумент2 страницыAPS For Peer MentoringDaniel John Cañares LegaspiОценок пока нет

- Cost of Production Report First Department: Quantity ScheduleДокумент4 страницыCost of Production Report First Department: Quantity ScheduleDaniel John Cañares LegaspiОценок пока нет

- Corporate Valuation A Guide For Analysts Managers and Investors PDFДокумент358 страницCorporate Valuation A Guide For Analysts Managers and Investors PDFMalcomОценок пока нет

- Lecture 10 Relevant Costing PDFДокумент49 страницLecture 10 Relevant Costing PDFShweta Sridhar57% (7)

- Group 4 - The City As A Growth MachineДокумент15 страницGroup 4 - The City As A Growth MachineDaffa AlweeОценок пока нет

- The Heathland School Sixth Form ProspectusДокумент33 страницыThe Heathland School Sixth Form Prospectusifernandes2911Оценок пока нет

- A Critique Paper On The Journal "Impacts of Units Pricing of Solid Waste Collection and Disposal in Olongapo City, Philippines"Документ3 страницыA Critique Paper On The Journal "Impacts of Units Pricing of Solid Waste Collection and Disposal in Olongapo City, Philippines"Danissa Lambon100% (1)

- Economics Project: Expected ChecklistДокумент2 страницыEconomics Project: Expected ChecklistMùkûl RãjpütОценок пока нет

- TA-Bar Chart InterpretationДокумент12 страницTA-Bar Chart InterpretationPaulo IlustreОценок пока нет

- JHU Spring2009 FinalExamSolutionsДокумент14 страницJHU Spring2009 FinalExamSolutionsJB 94Оценок пока нет

- Hull RMFI4 e CH 07Документ18 страницHull RMFI4 e CH 07jlosamОценок пока нет

- Chapter 1Документ25 страницChapter 1មនុស្សដែលខកចិត្ត ជាងគេលើលោកОценок пока нет

- Oligopoly HandoutДокумент36 страницOligopoly HandoutSarat ChandraОценок пока нет

- Intermediate Micro Review NoteДокумент73 страницыIntermediate Micro Review NoteKaiyuan HuangОценок пока нет

- Learning OutcomesДокумент6 страницLearning OutcomesRajesh GargОценок пока нет

- Chapter 4Документ2 страницыChapter 4Azi LheyОценок пока нет

- Market Analysis Course NotesДокумент3 страницыMarket Analysis Course Notesudbhav786100% (1)

- Chapter 7 PEMДокумент28 страницChapter 7 PEMMr. Viki Modi GeneralОценок пока нет

- Price Discrimination ApplicationsДокумент22 страницыPrice Discrimination ApplicationsAmine El AzdiОценок пока нет

- Forecasting and Demand MeasurementДокумент22 страницыForecasting and Demand Measurementthefallenangels100% (5)

- IMM PowerPoint PresentationДокумент10 страницIMM PowerPoint PresentationRakesh SrivastavaОценок пока нет

- GDP Deflator Vs CpiДокумент6 страницGDP Deflator Vs CpiAli HasanОценок пока нет

- Institute of Business and Public AffairsДокумент7 страницInstitute of Business and Public AffairsFatima BagayОценок пока нет

- Lecture 8.2 (Capm and Apt)Документ30 страницLecture 8.2 (Capm and Apt)Devyansh GuptaОценок пока нет

- Conrail Valuation: Valuation in A Competitive Bidding SituationДокумент8 страницConrail Valuation: Valuation in A Competitive Bidding SituationHarsh trivediОценок пока нет

- Economics 2019 v1.1: IA1 Sample Assessment InstrumentДокумент19 страницEconomics 2019 v1.1: IA1 Sample Assessment InstrumentAahz MandiusОценок пока нет

- HCMДокумент17 страницHCMJim MathilakathuОценок пока нет

- Module - 4 National Income Accounting: Reference: Ahuja - PG 15-35Документ31 страницаModule - 4 National Income Accounting: Reference: Ahuja - PG 15-35chunmaina10mbaОценок пока нет

- Robert W Kolb Series Energy Finance and Economics Analysis and Valuation Risk Management and The Future of Energy 1Документ12 страницRobert W Kolb Series Energy Finance and Economics Analysis and Valuation Risk Management and The Future of Energy 1Jerry ChiangОценок пока нет

![Practical Guide To Production Planning & Control [Revised Edition]](https://imgv2-1-f.scribdassets.com/img/word_document/235162742/149x198/2a816df8c8/1709920378?v=1)

![Practical Guide To Work Study [Revised Edition]](https://imgv2-2-f.scribdassets.com/img/word_document/245836753/149x198/e8597dfaef/1709916910?v=1)