Вам также может понравиться

- Bill French Case Submitted By: Sourabh Phanase Section: AДокумент2 страницыBill French Case Submitted By: Sourabh Phanase Section: AsourabhphanaseОценок пока нет

- Bill French Google Docs Group 5Документ7 страницBill French Google Docs Group 5Jay Florence DalucanogОценок пока нет

- Cost Management Accounting Assignment Bill French Case StudyДокумент5 страницCost Management Accounting Assignment Bill French Case Studydeepak boraОценок пока нет

- Bill French - Write Up1Документ10 страницBill French - Write Up1Nina EllyanaОценок пока нет

- Bill French AssignmentДокумент5 страницBill French Assignmenttechyuce100% (2)

- Bill FrenchДокумент5 страницBill Frenchabigail franciscoОценок пока нет

- Bill French CaseДокумент6 страницBill French CaseAnthonyTiuОценок пока нет

- Case-Bill FrenchДокумент3 страницыCase-Bill FrenchthearpanОценок пока нет

- CVP Analysis SolutionsДокумент23 страницыCVP Analysis SolutionsAdebayo Yusuff AdesholaОценок пока нет

- Bill FrenchДокумент6 страницBill FrenchRohit AcharyaОценок пока нет

- Bill French Case DataДокумент5 страницBill French Case Datadamanfromiran100% (1)

- Case ReichardДокумент23 страницыCase ReichardDesiSelviaОценок пока нет

- Hilton Case1Документ2 страницыHilton Case1Ana Fernanda Gonzales CaveroОценок пока нет

- Bill French SolutionДокумент5 страницBill French Solutionrics_alias087196Оценок пока нет

- Bill French Case - FINALДокумент6 страницBill French Case - FINALdamanfromiran0% (1)

- Sharing Sheet Hallstead JewelersДокумент11 страницSharing Sheet Hallstead JewelersHarpreet SinghОценок пока нет

- Forner Carpet CompanyДокумент7 страницForner Carpet CompanySimranjeet KaurОценок пока нет

- LIFO vs FIFO Impact on Merrimack TractorsДокумент3 страницыLIFO vs FIFO Impact on Merrimack TractorsstudvabzОценок пока нет

- Selligram Case Answer KeyДокумент3 страницыSelligram Case Answer Keysharkss521Оценок пока нет

- This Study Resource Was: Forner CarpetДокумент4 страницыThis Study Resource Was: Forner CarpetLi CarinaОценок пока нет

- Seligram 2Документ4 страницыSeligram 2Yvette YuanОценок пока нет

- MANAC II - Morrissey Forgings CaseДокумент8 страницMANAC II - Morrissey Forgings CaseKaran Oberoi100% (1)

- Huron Automotive Company ExcelllДокумент6 страницHuron Automotive Company Excelllmaximus0903Оценок пока нет

- Balakrishnan MGRL Solutions Ch14Документ36 страницBalakrishnan MGRL Solutions Ch14Aditya Krishna100% (1)

- Reichard Maschinen Plastic Ring TransitionДокумент23 страницыReichard Maschinen Plastic Ring TransitionAliefiah AZОценок пока нет

- Manufacturing Cost Analysis ReportДокумент5 страницManufacturing Cost Analysis Reportfelipe.com0% (1)

- Baldwin Bicycle CaseДокумент10 страницBaldwin Bicycle CaseDhurjati Majumdar100% (1)

- Superior ManufacturingДокумент5 страницSuperior ManufacturingCordel TwoKpsi TaildawgSnoop Cook100% (4)

- Cafe Monte BiancoДокумент21 страницаCafe Monte BiancoWilliam Torrez OrozcoОценок пока нет

- Wlatham SolutionДокумент3 страницыWlatham Solutionadi_santhi100% (7)

- Sol Wellington Chemicals DivisionДокумент3 страницыSol Wellington Chemicals DivisionRahul Goyal100% (1)

- Berkshire Toy CompanyДокумент25 страницBerkshire Toy CompanyrodriguezlavОценок пока нет

- Yuvraj Patil Section B 2010PGP435 Case: Bill French Mac IiДокумент4 страницыYuvraj Patil Section B 2010PGP435 Case: Bill French Mac Iiyuveesp5207Оценок пока нет

- Mile HighДокумент8 страницMile HighFaizan Ul HaqОценок пока нет

- Unitron CorporationДокумент7 страницUnitron CorporationERika PratiwiОценок пока нет

- ACCY 302 Danshui Plant Budget AnalysisДокумент1 страницаACCY 302 Danshui Plant Budget Analysisptanoy8Оценок пока нет

- ExercisesДокумент19 страницExercisesbajujuОценок пока нет

- Group 7 - Morrissey ForgingsДокумент10 страницGroup 7 - Morrissey ForgingsVishal AgarwalОценок пока нет

- Marvin Co Financial StatementsДокумент4 страницыMarvin Co Financial StatementsVaibhav KathjuОценок пока нет

- Hilton Manufacturing Company 1201326783827489 2Документ6 страницHilton Manufacturing Company 1201326783827489 2julijulijulioОценок пока нет

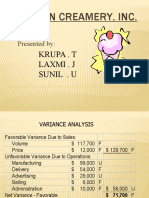

- Boston Creamery CaseДокумент9 страницBoston Creamery Caselion_heart3001100% (1)

- Hallstead Jewelers Breakeven AnalysisДокумент7 страницHallstead Jewelers Breakeven Analysisanon_839867152Оценок пока нет

- Tijuana Bronze MachiningДокумент9 страницTijuana Bronze MachiningNikhilesh Sirsikar75% (4)

- Analysis of Fastener Manufacturing Costs and ProfitsДокумент13 страницAnalysis of Fastener Manufacturing Costs and ProfitsKaran Oberoi33% (6)

- Case 26-2Документ3 страницыCase 26-2NishaОценок пока нет

- 19B135 Hallstead Jewellers CaseДокумент23 страницы19B135 Hallstead Jewellers CaseEashaa SaraogiОценок пока нет

- Reichard Maschinen DocumentДокумент5 страницReichard Maschinen DocumentLucille Ausborn100% (1)

- Final Test Accounting - DestinДокумент8 страницFinal Test Accounting - DestinRandy MarzeindОценок пока нет

- Johnson BeverageДокумент6 страницJohnson BeverageShouib Mehreyar100% (1)

- Prestige Telephone CompanyДокумент2 страницыPrestige Telephone CompanyArbaz AbbasОценок пока нет

- Baldwin Bicycle Company Case AnalysisДокумент12 страницBaldwin Bicycle Company Case AnalysisSamrat KaushikОценок пока нет

- Elwy Melina-Sarah MHCДокумент7 страницElwy Melina-Sarah MHCpalak32Оценок пока нет

- Bill French Accountant: Case StudyДокумент4 страницыBill French Accountant: Case StudyYash Raj SinghОценок пока нет

- Unit-5 Cost Volume Profit AnalysisДокумент44 страницыUnit-5 Cost Volume Profit AnalysisAnonymous dfy2iDZОценок пока нет

- Bill FrenchДокумент4 страницыBill Frenchabigail franciscoОценок пока нет

- 1244 - Roshan Kumar Sahoo - Assignment 2Документ3 страницы1244 - Roshan Kumar Sahoo - Assignment 2ROSHAN KUMAR SAHOOОценок пока нет

- Case Bill FrenchДокумент3 страницыCase Bill FrenchROSHAN KUMAR SAHOOОценок пока нет

- CMA Presentation: Bill French CaseДокумент12 страницCMA Presentation: Bill French CaseSahaj SharmaОценок пока нет

- S2 CMA c02 Cost-Volume-Profit AnalysisДокумент25 страницS2 CMA c02 Cost-Volume-Profit Analysisdiasjoy67Оценок пока нет

- Bill French Case SolutionДокумент3 страницыBill French Case SolutionMurat Kalender80% (5)