Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- EstimatingДокумент309 страницEstimatingFauzankalibata92% (24)

- Raft Slab DesignДокумент5 страницRaft Slab DesignLekins Sefiu Yekini100% (2)

- Manuale Injectors Delphi 15-23-2 Ediz IngДокумент7 страницManuale Injectors Delphi 15-23-2 Ediz IngKary Shito100% (2)

- Prepared For: Puan Khair Shakira Bustamam Prepared By: Anis Shahireen Effah Atiqah Fatinah Husna Nur FatinДокумент9 страницPrepared For: Puan Khair Shakira Bustamam Prepared By: Anis Shahireen Effah Atiqah Fatinah Husna Nur FatinFatinah Husna100% (2)

- Building MaterialsДокумент13 страницBuilding MaterialsPriyanka BasuОценок пока нет

- Inspection and Requalification of Flywheels Before Remounting - 09197Документ5 страницInspection and Requalification of Flywheels Before Remounting - 09197Mark ChapmanОценок пока нет

- Geological Storage Site Screening and ApprovalДокумент56 страницGeological Storage Site Screening and ApprovalIbukun OpeyemiОценок пока нет

- Untitled 66Документ6 страницUntitled 66radislamyОценок пока нет

- GSM Frequency Bands (Examples)Документ3 страницыGSM Frequency Bands (Examples)radislamyОценок пока нет

- 2.7. R T C F M D: Isks Hreatening The ASH Low and The Ethods of EfenceДокумент6 страниц2.7. R T C F M D: Isks Hreatening The ASH Low and The Ethods of EfenceradislamyОценок пока нет

- Technology and Innovation and Performance of Women Sses in Urban KenyaДокумент45 страницTechnology and Innovation and Performance of Women Sses in Urban KenyaradislamyОценок пока нет

- Young, Single Middle-Aged Couple With Children : 2.5. T C F L CДокумент5 страницYoung, Single Middle-Aged Couple With Children : 2.5. T C F L CradislamyОценок пока нет

- HTTPS://WWW - Scribd.com/presentation/136873757/huawei eRAN3 0 CSFB Feature IntroductionДокумент6 страницHTTPS://WWW - Scribd.com/presentation/136873757/huawei eRAN3 0 CSFB Feature IntroductionradislamyОценок пока нет

- 2.2. T H L C T H: HE Uman IFE Ycle Hroughout IstoryДокумент5 страниц2.2. T H L C T H: HE Uman IFE Ycle Hroughout IstoryradislamyОценок пока нет

- 2.2. T H L C T H: HE Uman IFE Ycle Hroughout IstoryДокумент5 страниц2.2. T H L C T H: HE Uman IFE Ycle Hroughout IstoryradislamyОценок пока нет

- Chapter 35Документ5 страницChapter 35radislamyОценок пока нет

- Life Insurance StructureДокумент6 страницLife Insurance StructureradislamyОценок пока нет

- 1.4. T A L T: HE Nalysis of The IFE AbleДокумент5 страниц1.4. T A L T: HE Nalysis of The IFE AbleradislamyОценок пока нет

- 1.4. T A L T: HE Nalysis of The IFE AbleДокумент5 страниц1.4. T A L T: HE Nalysis of The IFE AbleradislamyОценок пока нет

- Chapter34 PDFДокумент5 страницChapter34 PDFradislamyОценок пока нет

- Chapter 30Документ3 страницыChapter 30radislamyОценок пока нет

- Chapter 30Документ3 страницыChapter 30radislamyОценок пока нет

- Chapter 31Документ4 страницыChapter 31radislamyОценок пока нет

- Chapter 27 Leveling The Net Single PremiumДокумент19 страницChapter 27 Leveling The Net Single PremiumradislamyОценок пока нет

- Chapter 31Документ4 страницыChapter 31radislamyОценок пока нет

- Understanding Life Insurance OptionsДокумент3 страницыUnderstanding Life Insurance OptionsradislamyОценок пока нет

- Understanding Life Insurance OptionsДокумент3 страницыUnderstanding Life Insurance OptionsradislamyОценок пока нет

- Common provisions of annuities explainedДокумент3 страницыCommon provisions of annuities explainedradislamyОценок пока нет

- Chapter 1Документ33 страницыChapter 1radislamyОценок пока нет

- Life Insurance Contractual ProvisionsДокумент23 страницыLife Insurance Contractual Provisionsradislamy-1Оценок пока нет

- Understanding Life Insurance OptionsДокумент3 страницыUnderstanding Life Insurance OptionsradislamyОценок пока нет

- Understanding Life Insurance OptionsДокумент3 страницыUnderstanding Life Insurance OptionsradislamyОценок пока нет

- Chapter 10Документ2 страницыChapter 10umeshОценок пока нет

- Chapter 10Документ26 страницChapter 10radislamyОценок пока нет

- Strategy Formulation - FinalДокумент29 страницStrategy Formulation - FinalradislamyОценок пока нет

- ReadmeДокумент1 страницаReadmeradislamyОценок пока нет

- D Error codes - Engine diagnostic troubleshooting guideДокумент151 страницаD Error codes - Engine diagnostic troubleshooting guideValeriОценок пока нет

- Design and analyze a non-inverting op-amp circuit with gain of 10Документ7 страницDesign and analyze a non-inverting op-amp circuit with gain of 10Mandeep KaloniaОценок пока нет

- 15 Step Guide to Build Simple Electric GeneratorДокумент13 страниц15 Step Guide to Build Simple Electric GeneratorSeindahNyaОценок пока нет

- R&D Lorenzo-Siciliano ENIДокумент11 страницR&D Lorenzo-Siciliano ENIinterponОценок пока нет

- Android Snake With Kivy, PythonДокумент14 страницAndroid Snake With Kivy, Pythontsultim bhutiaОценок пока нет

- IssabelPBX AdministrationДокумент9 страницIssabelPBX AdministrationDaniel VieceliОценок пока нет

- Enum Types JavaДокумент3 страницыEnum Types JavaAmandeep PuniaОценок пока нет

- Fujitsu-General ASYG07-12 LLC 2014Документ2 страницыFujitsu-General ASYG07-12 LLC 2014Euro-klima BitolaОценок пока нет

- N48H Grade Neodymium Magnets DataДокумент1 страницаN48H Grade Neodymium Magnets DataSteve HsuОценок пока нет

- KATANA 5040R/5055R: High-End ImagesetterДокумент4 страницыKATANA 5040R/5055R: High-End ImagesetterAgence CreapubОценок пока нет

- J Control - DX 9100 Digital ControllerДокумент104 страницыJ Control - DX 9100 Digital Controlleramhosny640% (1)

- Anixter Wire&Cable Catalog Armored Cables PDFДокумент42 страницыAnixter Wire&Cable Catalog Armored Cables PDFAhmed H. HassanОценок пока нет

- District Sales Manager or Territory Manager or Regional ManagerДокумент3 страницыDistrict Sales Manager or Territory Manager or Regional Managerapi-121327024Оценок пока нет

- Architectural Design of Bangalore Exhibition CentreДокумент24 страницыArchitectural Design of Bangalore Exhibition CentreVeereshОценок пока нет

- State Bank of India - Recruitment of Probationary Officers PDFДокумент2 страницыState Bank of India - Recruitment of Probationary Officers PDFTapas Kumar NandiОценок пока нет

- Fluid Mechanics CalculationsДокумент3 страницыFluid Mechanics CalculationsandreagassiОценок пока нет

- Manual CleviteДокумент180 страницManual CleviteJacko JaraОценок пока нет

- Minimum drilling supplies stockДокумент3 страницыMinimum drilling supplies stockAsif KhanzadaОценок пока нет

- JMeter OAuth SamplerДокумент3 страницыJMeter OAuth SamplerFredy NataОценок пока нет

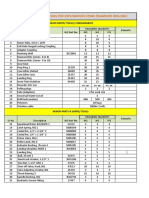

- Water Plant EstimateДокумент4 страницыWater Plant EstimateVishnu DasОценок пока нет

- Oracle® Database: 2 Day + Security Guide 11g Release 1 (11.1)Документ130 страницOracle® Database: 2 Day + Security Guide 11g Release 1 (11.1)arwahannanОценок пока нет

- VW T4 Automatic Gearbox Adapter Kit InstallationДокумент2 страницыVW T4 Automatic Gearbox Adapter Kit InstallationLuke HazelgroveОценок пока нет

- Lateral Earth Pressures For Seismic Design of Cantilever Retaining WallsДокумент8 страницLateral Earth Pressures For Seismic Design of Cantilever Retaining Wallsredpol100% (2)