Вам также может понравиться

- How To Wrestle - Instructions of Frank GotchДокумент66 страницHow To Wrestle - Instructions of Frank GotchDecameron100% (2)

- ChinnamastaДокумент184 страницыChinnamastaIoan Boca93% (15)

- Alluvial Diamonds Project Requires Investors in DR CongoДокумент25 страницAlluvial Diamonds Project Requires Investors in DR CongoLovemir Mauled100% (1)

- Quality Control + Quality Assurance + Quality ImprovementДокумент34 страницыQuality Control + Quality Assurance + Quality ImprovementMasni-Azian Akiah96% (28)

- Chapter 74 - Mining and QuarryingДокумент124 страницыChapter 74 - Mining and Quarryingbeku_ggs_bekuОценок пока нет

- Namibia Alluvial Diamond Project Seeking InvestorsДокумент24 страницыNamibia Alluvial Diamond Project Seeking InvestorsMauled Resources100% (1)

- RBS MoonTrading13Jun10Документ12 страницRBS MoonTrading13Jun10loreelyОценок пока нет

- Coal Investment Thailand enДокумент12 страницCoal Investment Thailand enKhan Ahmed MuradОценок пока нет

- Mining and Development in IndonesiaДокумент69 страницMining and Development in IndonesiaOlgi Kompresing100% (1)

- Data Analysis: What Will We Do With Our Data ?Документ38 страницData Analysis: What Will We Do With Our Data ?Linggar Kumara MurtiОценок пока нет

- Britmindogroupcompanyprofile PDFДокумент20 страницBritmindogroupcompanyprofile PDFSatia Aji PamungkasОценок пока нет

- Time and AttendanceДокумент5 страницTime and AttendancekgnmatinОценок пока нет

- Corporate Profile TanwinДокумент17 страницCorporate Profile TanwinSamsudin Puluhulawa100% (1)

- SME Internationalization in Emerging MarketsДокумент162 страницыSME Internationalization in Emerging MarketsKeyur DesaiОценок пока нет

- Type of DepositДокумент4 страницыType of DepositGuinevere RaymundoОценок пока нет

- The Neon Red Catalog: DisclaimerДокумент28 страницThe Neon Red Catalog: DisclaimerKarl Punu100% (2)

- CSR Project Report On NGOДокумент41 страницаCSR Project Report On NGOabhi ambre100% (3)

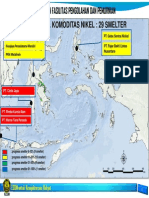

- Indo Nickel Mining and Industry Move ForwardДокумент29 страницIndo Nickel Mining and Industry Move Forwardone_peaceОценок пока нет

- Oil Production in South Sudan Summary Report DEF LRS 1Документ32 страницыOil Production in South Sudan Summary Report DEF LRS 1zubair1951Оценок пока нет

- Junior Copper ReportДокумент59 страницJunior Copper Reportkaiselk100% (1)

- Coal Trading Basics & Risk ManagementДокумент2 страницыCoal Trading Basics & Risk ManagementBisto MasiloОценок пока нет

- Coal Sales - PSBДокумент24 страницыCoal Sales - PSBGigih Marda PradanaОценок пока нет

- Reporting Coal Exploration FriederichM July09Документ73 страницыReporting Coal Exploration FriederichM July09Andrei Antariksa HadijayaОценок пока нет

- Kalimantan Coal Railway ProjectДокумент23 страницыKalimantan Coal Railway ProjectmimandapiconeОценок пока нет

- Investment Opportunity of Mineral and Coal in IndonesiaДокумент26 страницInvestment Opportunity of Mineral and Coal in IndonesiaKrisdanyolan SimarmataОценок пока нет

- Coal Trading Summary ProjectДокумент7 страницCoal Trading Summary ProjectFinda RaniОценок пока нет

- Pt. Jayeon SejahteraДокумент52 страницыPt. Jayeon SejahteraTrends Property100% (1)

- Indonesia's Nickel, Bauxite, Iron and Other Metal SmeltersДокумент8 страницIndonesia's Nickel, Bauxite, Iron and Other Metal SmeltersOki Hermansyah FebriantoОценок пока нет

- Indonesian Silica Sand ContractДокумент10 страницIndonesian Silica Sand ContractAudy McKayОценок пока нет

- Sukses Berkarir Di Industri TambangДокумент32 страницыSukses Berkarir Di Industri TambangFaishol UmarОценок пока нет

- Report on Consulting Services for Coal Sourcing, Transportation and Handling of Power Plants in BangladeshДокумент497 страницReport on Consulting Services for Coal Sourcing, Transportation and Handling of Power Plants in Bangladeshদেওয়ানসাহেবОценок пока нет

- Mining Companies PDFДокумент6 страницMining Companies PDFCristina Ortega CidОценок пока нет

- Implementasi Izin Usaha Pertambangan untuk Mengendalikan Kerusakan Lingkungan akibat Pertambangan Pasir di Kabupaten SlemanДокумент16 страницImplementasi Izin Usaha Pertambangan untuk Mengendalikan Kerusakan Lingkungan akibat Pertambangan Pasir di Kabupaten SlemankhfikdОценок пока нет

- Bintan Industrial Estate ProjectДокумент30 страницBintan Industrial Estate ProjectFazri FadillahОценок пока нет

- Reporting Coal Exploration FriederichMДокумент73 страницыReporting Coal Exploration FriederichMDadan100% (1)

- 0275 - IBG Ironbark Zinc Presentation June 2012 (20 06 12)Документ22 страницы0275 - IBG Ironbark Zinc Presentation June 2012 (20 06 12)poitan2100% (1)

- Maximizing Value Through Operational ExcellenceДокумент280 страницMaximizing Value Through Operational ExcellenceAsti MarianaОценок пока нет

- APAC ProspectusДокумент84 страницыAPAC Prospectusshare818Оценок пока нет

- Xstrata Copper - Inf Sostenibilidad 2011Документ47 страницXstrata Copper - Inf Sostenibilidad 2011Arturo Pedro Salgado MedinaОценок пока нет

- Global Coal Trade Services: Deliverables and PricingДокумент4 страницыGlobal Coal Trade Services: Deliverables and PricingVikram NavaleОценок пока нет

- Exclusive Indonesian COAL Directory, 2013 - 2014Документ2 страницыExclusive Indonesian COAL Directory, 2013 - 2014Central Data MediatamaОценок пока нет

- Resume KP - BaДокумент1 страницаResume KP - BadadanОценок пока нет

- South Sudan Mining Brochure PDFДокумент2 страницыSouth Sudan Mining Brochure PDFAnyak2014Оценок пока нет

- Laporan Absensi Over Time Agustus 2022 1Документ3 страницыLaporan Absensi Over Time Agustus 2022 1adi wibowoОценок пока нет

- Company ProfileДокумент16 страницCompany Profilefaisalshafiq1Оценок пока нет

- Peningkatan Nilai Tambah MIneral PDFДокумент38 страницPeningkatan Nilai Tambah MIneral PDFIndraОценок пока нет

- Contract Sales Purchase Agreement - TJU, RRU - ChinaДокумент7 страницContract Sales Purchase Agreement - TJU, RRU - Chinagarut beraksiОценок пока нет

- Perencanaan TambangДокумент41 страницаPerencanaan TambangSetiady MaruliОценок пока нет

- Mining EquipДокумент2 страницыMining Equipgaurav_mahajan1402Оценок пока нет

- The Mining CycleДокумент36 страницThe Mining CycleFernandes LatoxОценок пока нет

- Indonesian Coal Exporter - +62 8122 031 6492Документ5 страницIndonesian Coal Exporter - +62 8122 031 6492Konsultan Ekspor ImporОценок пока нет

- Kaolin and Zircon Quotation for REGIT-U CorporationДокумент3 страницыKaolin and Zircon Quotation for REGIT-U CorporationAbimanyu Sutanegara100% (1)

- KCI Biz Plan 2010Документ23 страницыKCI Biz Plan 2010A M Joko WinotoОценок пока нет

- Jingtang Port Expansion EiaДокумент82 страницыJingtang Port Expansion EiaSyed Noman AhmedОценок пока нет

- 11-SPA-draft - , Kks-Buyer 2020Документ9 страниц11-SPA-draft - , Kks-Buyer 2020fajarОценок пока нет

- Perbandingan Harga Kontrak Kerja Pt. Laman Mining & Pt. PBPNДокумент1 страницаPerbandingan Harga Kontrak Kerja Pt. Laman Mining & Pt. PBPNBlack CavannaОценок пока нет

- MDO Tender Format PDFДокумент61 страницаMDO Tender Format PDFVivek RanganathanОценок пока нет

- Proposal Biaya Survey Soil Investigation & Topography, Bathymetry, Soil Resistivity & Traffic CountingДокумент2 страницыProposal Biaya Survey Soil Investigation & Topography, Bathymetry, Soil Resistivity & Traffic CountingjlpinemОценок пока нет

- Company Profile PT Bintang Agro Sentosa English Standard Version PDFДокумент24 страницыCompany Profile PT Bintang Agro Sentosa English Standard Version PDFSkandinavia ApartmentОценок пока нет

- International Trade Course 5Документ34 страницыInternational Trade Course 5Sudershan ThaibaОценок пока нет

- July 2014Документ56 страницJuly 2014Gas, Oil & Mining Contractor MagazineОценок пока нет

- Maputo Development CorridorДокумент18 страницMaputo Development CorridorRaimundo Paulo Langa100% (1)

- COAL MINING TAKEAWAYSДокумент8 страницCOAL MINING TAKEAWAYSrikkiapОценок пока нет

- Mining Investment and Taxation Guide 2010Документ98 страницMining Investment and Taxation Guide 2010Michael Heng100% (1)

- Start Up Costs For A Sand & Gravel Mining Business - What You Need To Start & Succeed - State & LocalДокумент7 страницStart Up Costs For A Sand & Gravel Mining Business - What You Need To Start & Succeed - State & LocalFrank FreemanОценок пока нет

- Summary of The Article Making A Case For The Publishing of Petroleum Contracts in NigeriaДокумент4 страницыSummary of The Article Making A Case For The Publishing of Petroleum Contracts in Nigeriadamilola babadeОценок пока нет

- The End of an Era: Indonesia's Gross-Split PSC ModelДокумент20 страницThe End of an Era: Indonesia's Gross-Split PSC ModelCasual ThingОценок пока нет

- CIC Gold ProspectusДокумент104 страницыCIC Gold ProspectusFraserОценок пока нет

- Churchill MiningДокумент1 страницаChurchill MiningFraserОценок пока нет

- Carry Trade Dynamics Under Capital Controls: The Case of ChinaДокумент49 страницCarry Trade Dynamics Under Capital Controls: The Case of ChinaFraserОценок пока нет

- Disclaimer For EMCДокумент3 страницыDisclaimer For EMCFraserОценок пока нет

- MOG Investor PresentationДокумент34 страницыMOG Investor PresentationFraserОценок пока нет

- Demerger BLTДокумент38 страницDemerger BLTFraserОценок пока нет

- Morning Mumble Contrarian Gold & CU Were Told... + Ahhh'fren + AO. World + SHFTДокумент2 страницыMorning Mumble Contrarian Gold & CU Were Told... + Ahhh'fren + AO. World + SHFTFraserОценок пока нет

- Churchill Mining PLC & Planet Mining Pty LTD vs. Republic of Indonesia Document InspectionДокумент7 страницChurchill Mining PLC & Planet Mining Pty LTD vs. Republic of Indonesia Document InspectionFraserОценок пока нет

- Churchill Mining Posts To Date March 2013Документ23 страницыChurchill Mining Posts To Date March 2013FraserОценок пока нет

- Analysis of Glencore Xstrata's Sale of The Las Bambas Copper ProjectДокумент4 страницыAnalysis of Glencore Xstrata's Sale of The Las Bambas Copper ProjectFraserОценок пока нет

- Mark Bristow Randgold ResourcesДокумент24 страницыMark Bristow Randgold ResourcesFraserОценок пока нет

- Mines Online Metrics For Las BambasДокумент4 страницыMines Online Metrics For Las BambasFraserОценок пока нет

- Churchill Mining The Case So FarДокумент98 страницChurchill Mining The Case So FarFraserОценок пока нет

- Extraordinary General Meeting 07th March 2014Документ19 страницExtraordinary General Meeting 07th March 2014FraserОценок пока нет

- ShareSoc Press023 Faroe PetroleumДокумент2 страницыShareSoc Press023 Faroe PetroleumFraserОценок пока нет

- T1ps - CHLДокумент2 страницыT1ps - CHLFraserОценок пока нет

- UBS White Paper WEF 2014 CДокумент16 страницUBS White Paper WEF 2014 CTBP_Think_TankОценок пока нет

- Claimants Post-Hearing Brief (31 May 2013)Документ63 страницыClaimants Post-Hearing Brief (31 May 2013)Fraser100% (1)

- Bolivian Award Decision - Website RNS Final 01-02-14Документ2 страницыBolivian Award Decision - Website RNS Final 01-02-14FraserОценок пока нет

- Award For Bolivia & RurelecДокумент198 страницAward For Bolivia & RurelecFraserОценок пока нет

- Practice Guideline 6 JurisidictionДокумент19 страницPractice Guideline 6 JurisidictionFraserОценок пока нет

- UBS White Paper WEF 2014 CДокумент16 страницUBS White Paper WEF 2014 CTBP_Think_TankОценок пока нет

- Been Gone PDFДокумент2 страницыBeen Gone PDFmorriganssОценок пока нет

- Some Common Abbreviations in Newspapers and TestsДокумент2 страницыSome Common Abbreviations in Newspapers and TestsIrfan BalochОценок пока нет

- Mapping Active Directory Using Bloodhound: Blue Team EditionДокумент26 страницMapping Active Directory Using Bloodhound: Blue Team EditionFatonОценок пока нет

- Lesson 01: Communication: Process, Principles and Ethics: OutcomesДокумент9 страницLesson 01: Communication: Process, Principles and Ethics: OutcomesMaricris Saturno ManaloОценок пока нет

- Midtern Exam, Living in IT EraДокумент43 страницыMidtern Exam, Living in IT EraJhazz Landagan33% (3)

- FCE Rephrase and Word FormationДокумент5 страницFCE Rephrase and Word FormationMonicaОценок пока нет

- How To Write An ArticleДокумент9 страницHow To Write An ArticleNati PesciaОценок пока нет

- Assignment No. 3: Name: Sunandan Sharma Id: 181070064Документ3 страницыAssignment No. 3: Name: Sunandan Sharma Id: 181070064Sunandan SharmaОценок пока нет

- Objectives of Community Based RehabilitationДокумент2 страницыObjectives of Community Based Rehabilitationzen_haf23Оценок пока нет

- Ningam Siro NR Parmar OverruledДокумент32 страницыNingam Siro NR Parmar OverruledSardaar Harpreet Singh HoraОценок пока нет

- Test 1Документ13 страницTest 1Hoàng VũОценок пока нет

- Taqvi: Bin Syed Muhammad MuttaqiДокумент4 страницыTaqvi: Bin Syed Muhammad Muttaqiمحمد جواد علىОценок пока нет

- Ncube W No Pleasure Without ResponsibilityДокумент6 страницNcube W No Pleasure Without ResponsibilityPanganayi JamesОценок пока нет

- Exam Kit Extra Practice Questions (Suggested Answers)Документ3 страницыExam Kit Extra Practice Questions (Suggested Answers)WasangLi100% (2)

- Plant Layout Decision GuideДокумент31 страницаPlant Layout Decision GuideSagar PhullОценок пока нет

- SBPD Discipline MatrixДокумент8 страницSBPD Discipline MatrixLeah MoreauОценок пока нет

- Cervo Neue Font - FontlotcomДокумент10 страницCervo Neue Font - FontlotcomontaarabОценок пока нет

- Medical Audit Checklist Active File AuditДокумент2 страницыMedical Audit Checklist Active File AuditCOO TOP STARОценок пока нет

- Lecture-1 (General Introduction) Indian Penal CodeДокумент12 страницLecture-1 (General Introduction) Indian Penal CodeShubham PhophaliaОценок пока нет

- Endorsement Letter From The Head of InstitutionДокумент2 страницыEndorsement Letter From The Head of InstitutionkavinОценок пока нет

- NeqasДокумент2 страницыNeqasMa. Theresa Enrile100% (1)

- Ventana Research S&OP Study Results For Oliver WightДокумент31 страницаVentana Research S&OP Study Results For Oliver WightDavid RennieОценок пока нет

- Human Resource Management 14th Edition Mathis Test BankДокумент23 страницыHuman Resource Management 14th Edition Mathis Test BankLindaClementsyanmb100% (13)