Вам также может понравиться

- 03 Special Types of Customers of A Bank CasesДокумент4 страницы03 Special Types of Customers of A Bank CasesVikashKumarОценок пока нет

- SVP Donna P. Shotwell: Head, Human Resources Management GroupДокумент1 страницаSVP Donna P. Shotwell: Head, Human Resources Management GroupVenessa Salazar BarbiranОценок пока нет

- SSS Handbook PDFДокумент45 страницSSS Handbook PDFsarahОценок пока нет

- School Head Change LetterДокумент1 страницаSchool Head Change LetterRickОценок пока нет

- Receipts and CollectionsДокумент93 страницыReceipts and CollectionsKathleen100% (1)

- Notice of AcceptanceДокумент2 страницыNotice of AcceptanceFranz Raphael Chavez100% (1)

- Case Study Writing TA ASS 2Документ9 страницCase Study Writing TA ASS 2Sravya teluОценок пока нет

- Affidavit of Loss Drivers LicenseДокумент2 страницыAffidavit of Loss Drivers LicenseMelMel Bernardino100% (1)

- Credit PolicyДокумент10 страницCredit PolicyAyesha KhanОценок пока нет

- Point of Sale SystemДокумент15 страницPoint of Sale SystemSpencer TracyОценок пока нет

- HRM Group5 Case Study 1Документ3 страницыHRM Group5 Case Study 1DyenОценок пока нет

- Statement of Profit and LossДокумент2 страницыStatement of Profit and Lossradhika100% (1)

- Code of Business Ethics PolicyДокумент5 страницCode of Business Ethics PolicyVIJAY SINGH RAGHAVОценок пока нет

- Phil PlansДокумент1 страницаPhil PlansAtty Ron Rod0% (3)

- Assessor LetterДокумент4 страницыAssessor LetterMichael Dixon100% (1)

- Bank's Mudra Loan FormДокумент4 страницыBank's Mudra Loan FormRAM NAIDU CHOPPAОценок пока нет

- Dallas Auto Impound Release AuthorizationДокумент1 страницаDallas Auto Impound Release AuthorizationTyler BealsОценок пока нет

- Transportation Waiver and Release of LiabilityДокумент1 страницаTransportation Waiver and Release of LiabilityAnonymous iBVKp5Yl9A100% (1)

- Data Commentary For Table and FigureДокумент2 страницыData Commentary For Table and FigureAralc Balmes100% (1)

- Direct Incorporation CCM MyCoid PDFДокумент21 страницаDirect Incorporation CCM MyCoid PDFSanjevee NathanОценок пока нет

- Sample Letter Request For Returning of Undisbursed FundДокумент1 страницаSample Letter Request For Returning of Undisbursed FundMarl Louie SeminianoОценок пока нет

- Request LetterДокумент2 страницыRequest LetterprahladjoshiОценок пока нет

- Special Power of AttorneyДокумент1 страницаSpecial Power of Attorneyblueclouds veraОценок пока нет

- Robert Smith: Service CrewДокумент1 страницаRobert Smith: Service CrewEricka Rivera SantosОценок пока нет

- How To AnswerДокумент10 страницHow To AnswerRamavanitha Palaniapan VanithaОценок пока нет

- PassagesprojectДокумент7 страницPassagesprojectapi-340007824Оценок пока нет

- 2022 10 17 Credit Card Dispute Form For Project 8 9d25d04abcДокумент2 страницы2022 10 17 Credit Card Dispute Form For Project 8 9d25d04abcRommel100% (1)

- Agency Procurement RequestДокумент6 страницAgency Procurement RequestMARCIAL ASADAОценок пока нет

- 1604CДокумент1 страница1604CNguyen LinhОценок пока нет

- Lec Credit and Collection LettersДокумент8 страницLec Credit and Collection LettersAidiene GalachicoОценок пока нет

- Asst. Secretary COVER LETTER - Commonwealth SecДокумент2 страницыAsst. Secretary COVER LETTER - Commonwealth SecMichael KanuОценок пока нет

- Basic Rules and Regulations On Collections and DepositsДокумент15 страницBasic Rules and Regulations On Collections and DepositsLalaine Castillo100% (1)

- Complaint Against CondoДокумент43 страницыComplaint Against CondoQueens PostОценок пока нет

- Chapter 2 - Recording Business TransactionsДокумент6 страницChapter 2 - Recording Business TransactionsHa Phuoc HauОценок пока нет

- Sample SEcretary's Letter To The BankДокумент3 страницыSample SEcretary's Letter To The BankArria XiannaОценок пока нет

- DLSU Grad Activities 2018Документ4 страницыDLSU Grad Activities 2018Darren Goldwin DavidОценок пока нет

- Business Administration Course Description1Документ20 страницBusiness Administration Course Description1The Non-metaОценок пока нет

- Application For Services Rev 7-30-11Документ3 страницыApplication For Services Rev 7-30-11api-344400595Оценок пока нет

- Exercises On EERДокумент1 страницаExercises On EERMa Sheila A MagbooОценок пока нет

- Bilal Cover LetterДокумент1 страницаBilal Cover LetterbilalОценок пока нет

- REPUBLIC ACT 8972 (Solo Parents' Welfare Act of 2000)Документ5 страницREPUBLIC ACT 8972 (Solo Parents' Welfare Act of 2000)Wilchie Dane OlayresОценок пока нет

- BDO Business Online Banking FAQsДокумент4 страницыBDO Business Online Banking FAQsJuly FermiaОценок пока нет

- Name change request credit cardДокумент1 страницаName change request credit cardIsse NvrroОценок пока нет

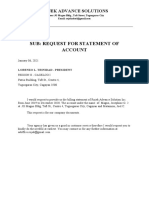

- Request Electricity Bill Statement for Rojek Advance SolutionsДокумент1 страницаRequest Electricity Bill Statement for Rojek Advance SolutionsJämes ScarlétteОценок пока нет

- Authorization Letter To Issue Death Certificate PDFДокумент1 страницаAuthorization Letter To Issue Death Certificate PDFBian RojasОценок пока нет

- Cash Flow Task RubricДокумент3 страницыCash Flow Task RubricNevin Spinosa100% (1)

- Letter of Intent For Statement of AccountДокумент1 страницаLetter of Intent For Statement of AccountZhaun Andrew LanoОценок пока нет

- Affidavit of Two Disinterested PersonsДокумент1 страницаAffidavit of Two Disinterested PersonsCeciliaОценок пока нет

- Authority To DebitДокумент1 страницаAuthority To DebitAlfredo Garcia100% (2)

- Annex FДокумент1 страницаAnnex FredjanneОценок пока нет

- Payment Reminder LetterДокумент1 страницаPayment Reminder Letterruhi jainОценок пока нет

- The Debt Collection PolicyДокумент3 страницыThe Debt Collection PolicyGulshan KumarОценок пока нет

- Gsis Loan of Deped EmployeesДокумент11 страницGsis Loan of Deped EmployeesJoy Manaog100% (1)

- Loan AgreementДокумент1 страницаLoan AgreementCarol Glitz100% (1)

- Job Description of Branch StaffДокумент3 страницыJob Description of Branch StaffEleanor JamcoОценок пока нет

- Collection letter templatesДокумент5 страницCollection letter templatesxzyl21100% (1)

- Habitual TardinessДокумент3 страницыHabitual TardinessGe NeОценок пока нет

- Lending Process - Loan Recovery, Delinquency ManagementДокумент26 страницLending Process - Loan Recovery, Delinquency ManagementSam KОценок пока нет

- ALM: Management of NPA: Sk. Nazibul Islam Faculty Member, BIBMДокумент43 страницыALM: Management of NPA: Sk. Nazibul Islam Faculty Member, BIBMrajin_rammsteinОценок пока нет

- Strategies of Recovering Default LoansДокумент7 страницStrategies of Recovering Default LoansMariam Adams100% (1)

- Young MindsДокумент60 страницYoung Mindsnevers23Оценок пока нет

- Phil-IRI Form 1 PretestДокумент2 страницыPhil-IRI Form 1 Pretestnevers23Оценок пока нет

- Active StudyДокумент2 страницыActive StudyAnke NemirovskyОценок пока нет

- Tet ChecДокумент2 страницыTet Checnevers23Оценок пока нет

- The Role of The Account Off in The Microfinance Loan ProcessДокумент12 страницThe Role of The Account Off in The Microfinance Loan Processnevers23Оценок пока нет

- 7 Attendance Sheet For Seminars and TrainingДокумент1 страница7 Attendance Sheet For Seminars and Trainingnevers23Оценок пока нет

- Amla Four AnswerДокумент1 страницаAmla Four Answernevers23Оценок пока нет

- Post Doc Letters ExamplesДокумент2 страницыPost Doc Letters ExamplesPriyance NababanОценок пока нет

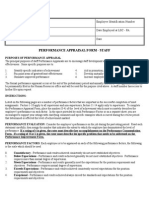

- Performance AppraisalsДокумент4 страницыPerformance Appraisalsnevers23Оценок пока нет

- Order of Adjectives PDFДокумент2 страницыOrder of Adjectives PDFSonia González UzОценок пока нет

- CorporateДокумент37 страницCorporatenevers23Оценок пока нет

- Competency InterviewДокумент13 страницCompetency InterviewMark ParsonsОценок пока нет

- Sample Safety Rules FinalДокумент2 страницыSample Safety Rules Finalnevers23Оценок пока нет

- GRE Math Review 2 AlgebraДокумент86 страницGRE Math Review 2 AlgebraJessica AngelinaОценок пока нет

- Sample of Letter To Request Reasonable AccommodationДокумент1 страницаSample of Letter To Request Reasonable Accommodationnevers23Оценок пока нет

- PHILOSOPHERS KnowThyselFДокумент68 страницPHILOSOPHERS KnowThyselFnevers23Оценок пока нет

- A Guide To The Foundational Beliefs N Practices of The Christian - Faith Essentials Fall 06 - Version 2Документ79 страницA Guide To The Foundational Beliefs N Practices of The Christian - Faith Essentials Fall 06 - Version 2itisme_angelaОценок пока нет

- Higher Order Thinking Skills Definition, Teaching Strategies & AssessmentДокумент177 страницHigher Order Thinking Skills Definition, Teaching Strategies & AssessmentRazak Kadir100% (6)

- 4CR A1.5, FFFДокумент73 страницы4CR A1.5, FFFnevers23Оценок пока нет

- Aaa Animal Scramble Babies and Adult SAMPLEДокумент4 страницыAaa Animal Scramble Babies and Adult SAMPLEnevers23Оценок пока нет

- Minutes of Friends of the Manitous Board MeetingДокумент5 страницMinutes of Friends of the Manitous Board Meetingnevers23Оценок пока нет

- Helpful Hints For Effective MeetingsДокумент33 страницыHelpful Hints For Effective Meetingsnevers23Оценок пока нет

- Requirements for Teachers Returning to PracticeДокумент1 страницаRequirements for Teachers Returning to Practicenevers23Оценок пока нет

- 2014.10.26 Blessed To Bless - Walk by Faith Focus On GodДокумент2 страницы2014.10.26 Blessed To Bless - Walk by Faith Focus On Godnevers23Оценок пока нет

- 01 Math - Grade - 2Документ110 страниц01 Math - Grade - 2Versoza NelОценок пока нет

- Academic Vocabulary ListДокумент42 страницыAcademic Vocabulary ListHarunVeledarОценок пока нет

- GOODYEAR PHILIPPINES v. SyДокумент5 страницGOODYEAR PHILIPPINES v. SyShiela MagnoОценок пока нет

- Concubinage AdulteryДокумент2 страницыConcubinage Adultery111111Оценок пока нет

- Gov Uscourts Nysd 362805 394 0Документ2 страницыGov Uscourts Nysd 362805 394 0Grant SternОценок пока нет

- 1st CasesДокумент50 страниц1st Cases001nooneОценок пока нет

- Atty's Misconduct in Notarizing Fake Land DocДокумент3 страницыAtty's Misconduct in Notarizing Fake Land DocAleph JirehОценок пока нет

- Lorenzo Shipping Corp V BJ MarthelДокумент19 страницLorenzo Shipping Corp V BJ Marthelmonkeypuzzle93Оценок пока нет

- Offer Letter EPIQ-RN Jojomol PDFДокумент13 страницOffer Letter EPIQ-RN Jojomol PDFJojomol AbrahamОценок пока нет

- August 2, 2017 - G.R.No.185597Документ12 страницAugust 2, 2017 - G.R.No.185597Anonymous yKUdPvwjОценок пока нет

- Judge James E. Towery and The Superior Court of California, County of Santa Clara - Response To ComplaintДокумент11 страницJudge James E. Towery and The Superior Court of California, County of Santa Clara - Response To ComplaintBen Z.Оценок пока нет

- Pal vs. Santos, Jr.Документ4 страницыPal vs. Santos, Jr.KaiОценок пока нет

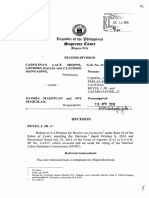

- Shopee Vs Maquilin PDFДокумент9 страницShopee Vs Maquilin PDFIm reineОценок пока нет

- Pariso, Philip JamescpltДокумент4 страницыPariso, Philip Jamescpltamannix3112Оценок пока нет

- Hagenbuch v. Komatsu AmericaДокумент12 страницHagenbuch v. Komatsu AmericaPriorSmartОценок пока нет

- Decision Letter-Poor PerformanceДокумент2 страницыDecision Letter-Poor Performancerosalyn michelle bacabacОценок пока нет

- Case Digest - Swedish Match v. CA, GR No. 128120, 2004-10-20Документ3 страницыCase Digest - Swedish Match v. CA, GR No. 128120, 2004-10-20graceОценок пока нет

- Techtronic Power Tools Tech. v. Harbor Freight - ComplaintДокумент47 страницTechtronic Power Tools Tech. v. Harbor Freight - ComplaintSarah BursteinОценок пока нет

- Property - Full Text - Co-OwnershipДокумент80 страницProperty - Full Text - Co-OwnershipElaine Belle OgayonОценок пока нет

- Hassel v. Oconee County Jail Et Al - Document No. 5Документ4 страницыHassel v. Oconee County Jail Et Al - Document No. 5Justia.comОценок пока нет

- KAUSNER Et Al v. BOMBARDIER, INC. Et Al DocketДокумент3 страницыKAUSNER Et Al v. BOMBARDIER, INC. Et Al DocketbombardierwatchОценок пока нет

- Medical Marijuana Rules - 19c30-95 - 6.30.2020Документ31 страницаMedical Marijuana Rules - 19c30-95 - 6.30.2020jimpeckhamОценок пока нет

- Philippine marriage nullity case psychological incapacity disputeДокумент13 страницPhilippine marriage nullity case psychological incapacity disputecagayatОценок пока нет

- Crim Pro DigestДокумент12 страницCrim Pro DigestChrysta FragataОценок пока нет

- Another D.C. Gun LawsuitДокумент40 страницAnother D.C. Gun LawsuitmaustermuhleОценок пока нет

- 02 Arriola V Pilipino Star NgayonДокумент3 страницы02 Arriola V Pilipino Star NgayonArtemisTzy100% (1)

- File Complaint State AgencyДокумент6 страницFile Complaint State Agencypujoe1076Оценок пока нет

- Rodrigo Gabuya V. Antonio Layug: G.R. No. 104846 - 23 November 1995Документ2 страницыRodrigo Gabuya V. Antonio Layug: G.R. No. 104846 - 23 November 1995Hariette Kim TiongsonОценок пока нет

- Montemayor v. BundalianДокумент27 страницMontemayor v. Bundalianmerlyn gutierrezОценок пока нет

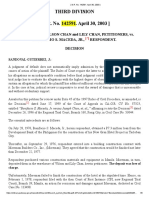

- 3) Chan vs. MacedaДокумент8 страниц3) Chan vs. MacedaElsha DamoloОценок пока нет

- Fyre Festival Ja Rule DismissalДокумент32 страницыFyre Festival Ja Rule DismissaldanielrestoredОценок пока нет

- FaceTime Break Class-Action SuitДокумент36 страницFaceTime Break Class-Action SuitMikey Campbell100% (1)