Вам также может понравиться

- Locgov Finals 2010-AДокумент7 страницLocgov Finals 2010-ADustin GonzalezОценок пока нет

- Cover Page AnnexesДокумент1 страницаCover Page AnnexesDustin GonzalezОценок пока нет

- Philippine Priority Chemicals List PCLДокумент7 страницPhilippine Priority Chemicals List PCLDustin GonzalezОценок пока нет

- Agreement Among The Government of Brunei Darussalam PDFДокумент7 страницAgreement Among The Government of Brunei Darussalam PDFDustin GonzalezОценок пока нет

- 83 Protecting Post-Mortem Privacy: Reconsidering The Privacy Interests of The deДокумент37 страниц83 Protecting Post-Mortem Privacy: Reconsidering The Privacy Interests of The deDustin GonzalezОценок пока нет

- 2011+ +FRIA+Outline+ +ALS+Commercial+Law+ReviewДокумент19 страниц2011+ +FRIA+Outline+ +ALS+Commercial+Law+ReviewmanzzzzzОценок пока нет

- Philippine Administrative Law EssentialsДокумент18 страницPhilippine Administrative Law EssentialsMary Louise Villegas79% (29)

- June-October law course calendarДокумент6 страницJune-October law course calendarDustin GonzalezОценок пока нет

- Galvez v. Court of Appeals - Directors convicted of estafa for deceiving bank into believing two companies were same entityДокумент2 страницыGalvez v. Court of Appeals - Directors convicted of estafa for deceiving bank into believing two companies were same entityDustin Gonzalez100% (1)

- Fqar 04-30-2012 PDFДокумент1 страницаFqar 04-30-2012 PDFDustin GonzalezОценок пока нет

- Foreign Judgments in ASEAN - A ProposalДокумент14 страницForeign Judgments in ASEAN - A ProposalDustin GonzalezОценок пока нет

- Political Law 2014 Bar SyllabusДокумент13 страницPolitical Law 2014 Bar SyllabusMarge RoseteОценок пока нет

- Bahais v. Pascual DigestДокумент2 страницыBahais v. Pascual DigestErla ElauriaОценок пока нет

- Structural Steel Angle Bar Section PropertiesДокумент3 страницыStructural Steel Angle Bar Section PropertiesDustin GonzalezОценок пока нет

- 2014 Bar Civil LawДокумент14 страниц2014 Bar Civil LawAries BautistaОценок пока нет

- National Plumbing Code Fo The PhilippinesДокумент57 страницNational Plumbing Code Fo The Philippinesjayson_pam98% (40)

- Rectangular Tube: Description Item # ThicknessДокумент1 страницаRectangular Tube: Description Item # ThicknessDustin GonzalezОценок пока нет

- RA 1378 - Master Plumber LawДокумент5 страницRA 1378 - Master Plumber LawFzoe YambaoОценок пока нет

- Uap Document 301Документ9 страницUap Document 301Dustin GonzalezОценок пока нет

- PROPERTY - BLOCK 1 - Title III: Co-Ownership, 208-256 - PageДокумент23 страницыPROPERTY - BLOCK 1 - Title III: Co-Ownership, 208-256 - PageDustin GonzalezОценок пока нет

- Builder BuilderДокумент6 страницBuilder BuilderDustin GonzalezОценок пока нет

- PROPERTY - BLOCK 1 - Title III: Co-Ownership, 208-256 - PageДокумент23 страницыPROPERTY - BLOCK 1 - Title III: Co-Ownership, 208-256 - PageDustin GonzalezОценок пока нет

- Status Update of The IAI Work Plan I (2002-2008)Документ3 страницыStatus Update of The IAI Work Plan I (2002-2008)Dustin GonzalezОценок пока нет

- Firecode SummaryДокумент3 страницыFirecode SummaryDustin GonzalezОценок пока нет

- Mid-Term Review of ASEAN Initiative for Integration Work PlanДокумент124 страницыMid-Term Review of ASEAN Initiative for Integration Work PlanDustin GonzalezОценок пока нет

- Technical Specifications - PlumbingДокумент19 страницTechnical Specifications - PlumbingVicVicОценок пока нет

- UAP Architects Philippines Standards Ethics EducationДокумент1 страницаUAP Architects Philippines Standards Ethics EducationDustin GonzalezОценок пока нет

- Banking and finance case digestsДокумент2 страницыBanking and finance case digestsDustin GonzalezОценок пока нет

- O o o o o o O: IndividualsДокумент17 страницO o o o o o O: IndividualsDustin GonzalezОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Tax Reform GhanaДокумент13 страницTax Reform GhanaAdlu AbdilahОценок пока нет

- British Airways Vs CIR (Actually This Is CIR Vs BOAC)Документ2 страницыBritish Airways Vs CIR (Actually This Is CIR Vs BOAC)Ton Ton CananeaОценок пока нет

- Skyquad Electronics Pay Slip TitleДокумент2 страницыSkyquad Electronics Pay Slip Titlerahul rahulОценок пока нет

- Compliance Manual F.Y. 2020 21 A.Y.2021 22 PDFДокумент52 страницыCompliance Manual F.Y. 2020 21 A.Y.2021 22 PDFTHERMAL TECH ENGINEERINGОценок пока нет

- IQAC MAIN-Aug21Документ3 страницыIQAC MAIN-Aug21Mohan RajОценок пока нет

- Chapter 27 Sales Interstate Exempted EntryДокумент3 страницыChapter 27 Sales Interstate Exempted EntryTEJA SINGHОценок пока нет

- #60 CIR vs. TMX SalesДокумент2 страницы#60 CIR vs. TMX SalesJan Rhoneil SantillanaОценок пока нет

- Module 01 Fundamrental Principles of TaxationДокумент21 страницаModule 01 Fundamrental Principles of TaxationRieXDОценок пока нет

- PACOR V BIR GR No. 215427Документ1 страницаPACOR V BIR GR No. 215427Latjing SolimanОценок пока нет

- Holiday and Wage Record SpreadsheetДокумент2 страницыHoliday and Wage Record SpreadsheetpasangbhpОценок пока нет

- Taxation+I+General+Principles+Reviewer+for+Atty +monteroДокумент27 страницTaxation+I+General+Principles+Reviewer+for+Atty +monteroMars SacdalanОценок пока нет

- Notes Dalton Case StudyДокумент1 страницаNotes Dalton Case StudyAMОценок пока нет

- Dtaa - Double Taxation Avoidance AgreementsДокумент17 страницDtaa - Double Taxation Avoidance AgreementsShubhankar Johari100% (1)

- 0456 Business TaxationДокумент4 страницы0456 Business Taxationpsycho_bhoot86Оценок пока нет

- Allegations Cancellation Notice For Aditya TelengДокумент3 страницыAllegations Cancellation Notice For Aditya TelengAaditya TelangОценок пока нет

- Company Info - Print Financials2Документ2 страницыCompany Info - Print Financials2rojaОценок пока нет

- ACCO 340 - Course Outline - FALL 2023 - Midterm Date SUN OCT 29, 2023 9AM TO NOONДокумент6 страницACCO 340 - Course Outline - FALL 2023 - Midterm Date SUN OCT 29, 2023 9AM TO NOONbushrasaleem5699Оценок пока нет

- Group Assignment - April 23Документ16 страницGroup Assignment - April 23DIVA RTHINIОценок пока нет

- Quotation Cum Proforma Invoice: Packaging and ForwardingДокумент1 страницаQuotation Cum Proforma Invoice: Packaging and ForwardingDHIRAJ ANAND SHINDEОценок пока нет

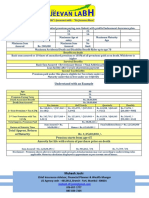

- LIC Jeevan LabhДокумент1 страницаLIC Jeevan LabhMukesh JoshiОценок пока нет

- Modjy 2003en F PDFДокумент14 страницModjy 2003en F PDFIRVINGSОценок пока нет

- Concept and Purpose of TaxationДокумент5 страницConcept and Purpose of TaxationNaiza Mae R. Binayao100% (1)

- Delinquent Tax Sale: Real EstateДокумент3 страницыDelinquent Tax Sale: Real EstateUSA TODAY100% (2)

- New Exchange/Segment Activation Request Form: To, Angel Broking LimitedДокумент2 страницыNew Exchange/Segment Activation Request Form: To, Angel Broking LimitedasdfОценок пока нет

- Gran Turismo Mon 21 Aug 1815 TicketsДокумент2 страницыGran Turismo Mon 21 Aug 1815 TicketsJohn John EstiponaОценок пока нет

- OrderAck - CV AnboДокумент2 страницыOrderAck - CV AnboAndi ApriadiОценок пока нет

- Government of India Receipt Budget 2022-23Документ81 страницаGovernment of India Receipt Budget 2022-23Shubham JhaОценок пока нет

- Recover Bad Debts Tax RulesДокумент7 страницRecover Bad Debts Tax RulesRonHilarioОценок пока нет

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Документ1 страницаTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Ayush NarayanОценок пока нет

- Final Report RohiniДокумент31 страницаFinal Report RohiniSagar BitlaОценок пока нет