Вам также может понравиться

- A Comprehensive Report On Consumer Research On FMCG Sector With Reference To Packed FoodДокумент60 страницA Comprehensive Report On Consumer Research On FMCG Sector With Reference To Packed FoodAKANKSHAОценок пока нет

- FMCG Sector HistoryДокумент1 страницаFMCG Sector HistoryVaibhav Autade100% (5)

- Vishal Mega Mart 1Документ49 страницVishal Mega Mart 1shyamgrwl5Оценок пока нет

- A Project Report OnДокумент19 страницA Project Report OnTanvi Mudhale100% (2)

- Lakme ProductДокумент50 страницLakme ProductRithik ThakurОценок пока нет

- Ankit Sharma - Mayank Jain - Nikhil Kumar - Prashant Pandey - Ridhi Arora - Saquib AliДокумент15 страницAnkit Sharma - Mayank Jain - Nikhil Kumar - Prashant Pandey - Ridhi Arora - Saquib Aliworld_ridhiОценок пока нет

- HALDIRAM Looking For Right Marketing MixДокумент9 страницHALDIRAM Looking For Right Marketing MixkristokunsОценок пока нет

- Entrepreneurship Project of New Product LaunchingДокумент52 страницыEntrepreneurship Project of New Product LaunchingDhannu Rawani50% (2)

- Analysis of Retail IndustryДокумент9 страницAnalysis of Retail IndustrySyreeta SheltonОценок пока нет

- Final Ready To Eat PDFДокумент39 страницFinal Ready To Eat PDFAbhishek Verma50% (2)

- A Study On The Effect of BTL Marketing On Consumer Purchase Decisions in Top Three FMGC Secter in IndiaДокумент4 страницыA Study On The Effect of BTL Marketing On Consumer Purchase Decisions in Top Three FMGC Secter in IndiaMelky BОценок пока нет

- Parle G CompareДокумент7 страницParle G Compareabhijitj555Оценок пока нет

- Kellogs and MaricoДокумент18 страницKellogs and MaricoDISHA SACHAN Student, Jaipuria LucknowОценок пока нет

- Indian Biscuit MarketДокумент15 страницIndian Biscuit MarketRitushree RayОценок пока нет

- Equity Research On Automobile Sector of IndiaДокумент15 страницEquity Research On Automobile Sector of IndiaHitesh Thapar50% (2)

- MDH Supply ChainДокумент16 страницMDH Supply Chainskyisallyours100% (3)

- A Study On Capital Structure: With Reference To FMCG CompaniesДокумент36 страницA Study On Capital Structure: With Reference To FMCG CompaniesArpit KulshreshthaОценок пока нет

- RTC QuestionnaireДокумент3 страницыRTC QuestionnaireSunil Ranjan MohapatraОценок пока нет

- Surf - STPДокумент4 страницыSurf - STPGunjanОценок пока нет

- Food Survey of IndiaДокумент258 страницFood Survey of Indiameenx100% (1)

- Food Processing Industry in IndiaДокумент28 страницFood Processing Industry in IndiaFarhan Khan50% (2)

- A Study On Customer Satisfaction Towards Organic India of Gproducts in Lucknow City GeetikaДокумент89 страницA Study On Customer Satisfaction Towards Organic India of Gproducts in Lucknow City GeetikaRishabh DhawanОценок пока нет

- Retail Marketing ProjectДокумент8 страницRetail Marketing ProjectDebashish MaityОценок пока нет

- The Taste of Tradition: Submitted byДокумент14 страницThe Taste of Tradition: Submitted byvijay malikОценок пока нет

- Lta06 FMCGДокумент82 страницыLta06 FMCGHemendra GuptaОценок пока нет

- Dabur: - Dedicated To The Health and Well Being of Every Household - Aman YadavДокумент18 страницDabur: - Dedicated To The Health and Well Being of Every Household - Aman YadavJyoti YadavОценок пока нет

- Business Environment ProjectДокумент41 страницаBusiness Environment ProjectNikhil Manocha100% (1)

- New Product Launch MR - Potato ChipsДокумент37 страницNew Product Launch MR - Potato ChipsVVMОценок пока нет

- MaricoДокумент28 страницMaricoSiddhantSethia100% (1)

- Project On RecessionДокумент10 страницProject On Recessionjaswantmaurya0% (1)

- India Food Retailing - Major PlayersДокумент17 страницIndia Food Retailing - Major PlayersShailley FirdousОценок пока нет

- Growth and Challenges of Retail Industry in India: An AnalysisДокумент14 страницGrowth and Challenges of Retail Industry in India: An AnalysisJyotika KodwaniОценок пока нет

- Big Bazaar Vs Spar: Gaurav Kumar - 08PG304Документ10 страницBig Bazaar Vs Spar: Gaurav Kumar - 08PG304Gaurav KumarОценок пока нет

- Minor Project FutureДокумент12 страницMinor Project Futuresourabijoy royОценок пока нет

- Hypothesis Organized RetailДокумент17 страницHypothesis Organized RetailManish Patel100% (1)

- DR Reddy PharmaceuticalsДокумент17 страницDR Reddy PharmaceuticalstnschandraОценок пока нет

- NCHMCT Jee: Sample QuestionsДокумент5 страницNCHMCT Jee: Sample QuestionsAnonymous 0IWTmWjBОценок пока нет

- Kanishka Specialisation TopicДокумент42 страницыKanishka Specialisation TopickanishkОценок пока нет

- University of Lucknow Department of Business Administration: Submitted To: Submitted By: Dr. JK Sharma Srinath Verma'Документ22 страницыUniversity of Lucknow Department of Business Administration: Submitted To: Submitted By: Dr. JK Sharma Srinath Verma'srinathОценок пока нет

- EPC and ECGCДокумент2 страницыEPC and ECGCShubhajit Nandi100% (1)

- CB CasesДокумент10 страницCB Caseschitral2285Оценок пока нет

- "Scope of Ready-To-Cook/eat Food Products in India and Consumer Behaviour Towards The SameДокумент84 страницы"Scope of Ready-To-Cook/eat Food Products in India and Consumer Behaviour Towards The Samebook worm foreverОценок пока нет

- Fundamental Analysis of Indian Pharmaceutical Companies: June 2018Документ25 страницFundamental Analysis of Indian Pharmaceutical Companies: June 2018Prakhar BhatnagarОценок пока нет

- HUL ProjectДокумент47 страницHUL Projectpothupalepu prabhuОценок пока нет

- The Plight of Indian FarmersДокумент15 страницThe Plight of Indian FarmersGaurav SavlaniОценок пока нет

- Final ProjectДокумент78 страницFinal ProjectNitin singhОценок пока нет

- Organized Retailing in Kerala - Key Issues and ChallengesДокумент11 страницOrganized Retailing in Kerala - Key Issues and ChallengesSiva Prakash100% (1)

- Presented By:: Anvita Misra Mohd. Ghazi Pankhuri Gupta Trimester 6Документ14 страницPresented By:: Anvita Misra Mohd. Ghazi Pankhuri Gupta Trimester 6शुभम त्रिवेदीОценок пока нет

- Demand Survey of Hyundai Motors Ltd.Документ5 страницDemand Survey of Hyundai Motors Ltd.Prince KaliaОценок пока нет

- Title: - To Study in Detail The Production Process of Making Various Suhana Masala. Name of Company: - Suhana Masala, Pune ObjectivesДокумент12 страницTitle: - To Study in Detail The Production Process of Making Various Suhana Masala. Name of Company: - Suhana Masala, Pune ObjectivesPranav Bedmutha100% (1)

- Technical Analysis of TATA STEELДокумент6 страницTechnical Analysis of TATA STEELshalintrivedi28Оценок пока нет

- HaldiramДокумент18 страницHaldiramStany D'melloОценок пока нет

- Indian Edible Oil Market: Trends and Opportunities (2014-2019) - New Report by Daedal ResearchДокумент13 страницIndian Edible Oil Market: Trends and Opportunities (2014-2019) - New Report by Daedal ResearchDaedal ResearchОценок пока нет

- HaldiramДокумент5 страницHaldiramSnehal JoshiОценок пока нет

- Consumer Awareness and Behavior Towards Nutraceutical Products in IndiaДокумент78 страницConsumer Awareness and Behavior Towards Nutraceutical Products in IndiaSarathKumar0% (1)

- Ready To Eat Food MRP DraftДокумент29 страницReady To Eat Food MRP DraftYo Yo Moyal RajОценок пока нет

- Food RetailingДокумент49 страницFood RetailingankitОценок пока нет

- Food and GroceryДокумент8 страницFood and GroceryprasannaОценок пока нет

- Trends, Challenges and Opportunities in Global RetailingДокумент14 страницTrends, Challenges and Opportunities in Global RetailingDipak K. SahОценок пока нет

- RDM Project Anupam UppalДокумент11 страницRDM Project Anupam UppalkhurppОценок пока нет

- Companies ListДокумент3 страницыCompanies ListJitendra Baviskar100% (1)

- PNB Overseas Directory PDFДокумент7 страницPNB Overseas Directory PDFReah Liza Padaoan SalvinoОценок пока нет

- 5 Global LogisticsДокумент36 страниц5 Global LogisticsAlex Mason100% (1)

- Labeling, Handling and Collection of Healthcare WasteДокумент28 страницLabeling, Handling and Collection of Healthcare WasteKanze AhiuОценок пока нет

- Manual de Gramática Básica Y Avanzada Del Español: D. Thomas & I. McalisterДокумент154 страницыManual de Gramática Básica Y Avanzada Del Español: D. Thomas & I. McalisterGingerОценок пока нет

- There Were No Winners in This Govt Shutdown.Документ4 страницыThere Were No Winners in This Govt Shutdown.My Brightest Star Park JisungОценок пока нет

- AN Analysis of Impact of Crude Oil Prices On Indian EconomyДокумент28 страницAN Analysis of Impact of Crude Oil Prices On Indian EconomySrijan SaxenaОценок пока нет

- SA Climate Action and Adaptation PlanДокумент92 страницыSA Climate Action and Adaptation PlanDavid IbanezОценок пока нет

- FI-Access To Banking Services-BSBD - 10062019Документ2 страницыFI-Access To Banking Services-BSBD - 10062019bhawani shankar SharmaОценок пока нет

- Corporate Finance NPV and IRR SolutionsДокумент3 страницыCorporate Finance NPV and IRR SolutionsMark HarveyОценок пока нет

- Fox Entertainment GroupДокумент4 страницыFox Entertainment GrouplaughingjoeyОценок пока нет

- Civil Engg Cos List - MajorsДокумент10 страницCivil Engg Cos List - MajorsGp MishraОценок пока нет

- Isint BrochureДокумент12 страницIsint BrochureCristian GuerraОценок пока нет

- Profiting With Ichimoku CloudsДокумент46 страницProfiting With Ichimoku Cloudsram100% (2)

- Micro Finance AppendicesДокумент42 страницыMicro Finance AppendicesJiya PatelОценок пока нет

- SWOT of Indian Banking SectorДокумент10 страницSWOT of Indian Banking SectorRashi AroraОценок пока нет

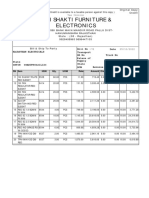

- Shri Shakti Furniture & Electronics: Credit OrginalДокумент1 страницаShri Shakti Furniture & Electronics: Credit OrginalRahul BansalОценок пока нет

- Application Form For BusinessesДокумент1 страницаApplication Form For Businessesentabs20160% (1)

- Diajukan OlehДокумент23 страницыDiajukan OlehdheaОценок пока нет

- Canara - Epassbook - 2023-11-02 200708.530629Документ95 страницCanara - Epassbook - 2023-11-02 200708.530629manojsailor855Оценок пока нет

- Rs. 20 Lakh Crore Haryana Realestate ScamДокумент53 страницыRs. 20 Lakh Crore Haryana Realestate ScamSrini KalyanaramanОценок пока нет

- Industry Projections 2020: Australian Cattle - April UpdateДокумент7 страницIndustry Projections 2020: Australian Cattle - April UpdateMark RippetoeОценок пока нет

- Wealth Management in Asia 2016 PDFДокумент240 страницWealth Management in Asia 2016 PDFChristamam Herry WijayaОценок пока нет

- Contoh Biaya ProduksiДокумент6 страницContoh Biaya ProduksiRobbenWОценок пока нет

- Arbitration CaselistДокумент12 страницArbitration CaselistDaniel FordanОценок пока нет

- Usfda-Generic Drug User Fee Act - A Complete ReviewДокумент15 страницUsfda-Generic Drug User Fee Act - A Complete ReviewijsidonlineinfoОценок пока нет

- Sale Deed EnglishДокумент4 страницыSale Deed Englishnavneet0% (1)

- Kotak Mahindra ProjectДокумент79 страницKotak Mahindra Project98108992% (24)

- Fundamental and Technical Analysis of - Dabur IndiaДокумент24 страницыFundamental and Technical Analysis of - Dabur Indiaramji80% (5)

- JBC Travel and ToursДокумент15 страницJBC Travel and ToursArshier Ching0% (1)