Вам также может понравиться

- Mithilesh Trivedi Batch: - PGP/SS/13-15/T2Документ53 страницыMithilesh Trivedi Batch: - PGP/SS/13-15/T2RaviGajjarОценок пока нет

- Airlines Sector in India and Its Contribution in Indian GDPДокумент11 страницAirlines Sector in India and Its Contribution in Indian GDPAnshuman UpadhyayОценок пока нет

- Industry Analysis Project (Indigo)Документ30 страницIndustry Analysis Project (Indigo)amar82% (11)

- Indigo AirlinesДокумент34 страницыIndigo AirlinesRavi Jaisinghani100% (1)

- India's Aviation Sector StrugglesДокумент5 страницIndia's Aviation Sector StrugglesRonit GuptaОценок пока нет

- Indian Aviation Industry Growth Hindered by Economic RecessionДокумент8 страницIndian Aviation Industry Growth Hindered by Economic RecessionHemant KumarОценок пока нет

- Indian Airline Industry - Group1Документ58 страницIndian Airline Industry - Group1Shankho BaghОценок пока нет

- IndigoДокумент58 страницIndigoKaran Wasan75% (4)

- Analyzing Vistara's Strategic Positioning in the Indian Aviation IndustryДокумент11 страницAnalyzing Vistara's Strategic Positioning in the Indian Aviation IndustryShailendra PrajapatiОценок пока нет

- Future Outlook of Aviation Industry: ConclusionДокумент5 страницFuture Outlook of Aviation Industry: Conclusionmanjunath4708Оценок пока нет

- Air India Business Overview and FinancialsДокумент13 страницAir India Business Overview and FinancialsgirishimmortalОценок пока нет

- Financial Derivatives Help Manage Aviation Industry RiskДокумент7 страницFinancial Derivatives Help Manage Aviation Industry RiskFrancis JohnsonОценок пока нет

- National Civil Aviation PolicyДокумент6 страницNational Civil Aviation PolicyMd Sarfaraz NawazОценок пока нет

- Consumer Behavior Analysis of The Airline Sector: A Case of Air IndiaДокумент16 страницConsumer Behavior Analysis of The Airline Sector: A Case of Air IndiaRohtash Singh RathoreОценок пока нет

- Business AviationДокумент3 страницыBusiness AviationVikash PandeyОценок пока нет

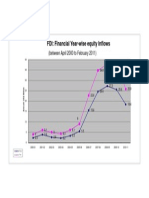

- Fdi in Aviation (Im)Документ27 страницFdi in Aviation (Im)Mohit VermaОценок пока нет

- Market SizeДокумент3 страницыMarket Sizerishabh lohiyaОценок пока нет

- Industry AnalysisДокумент16 страницIndustry AnalysisShashwat MishraОценок пока нет

- Air Asia's Low-Cost Airline Entry into the Growing Indian MarketДокумент18 страницAir Asia's Low-Cost Airline Entry into the Growing Indian MarketPrathapОценок пока нет

- A Spicy AffairДокумент16 страницA Spicy AffairPravin SinghОценок пока нет

- Future of Work in Aviation Industry Concept PaperДокумент8 страницFuture of Work in Aviation Industry Concept PaperPalak Makhija100% (1)

- Indian Aviation IndustryДокумент7 страницIndian Aviation IndustryAMAN KUMARОценок пока нет

- Enhancing Air Connectivity: 4 International Conference On Civil AviationДокумент52 страницыEnhancing Air Connectivity: 4 International Conference On Civil AviationRakkuyil SarathОценок пока нет

- PWC FICCI Knowledge Paper in Aviation Wings 2022 1648497337Документ40 страницPWC FICCI Knowledge Paper in Aviation Wings 2022 1648497337Manoj ShettyОценок пока нет

- Research and Analysis of Indian AirlinesДокумент48 страницResearch and Analysis of Indian AirlinesArpana KarnaОценок пока нет

- Aviation SectorДокумент19 страницAviation SectorUdayan SikdarОценок пока нет

- Introduction of Aviation SectorДокумент15 страницIntroduction of Aviation Sectorpoojapatil90Оценок пока нет

- AviationДокумент37 страницAviationDeepika RaoОценок пока нет

- Jet - EtihadДокумент21 страницаJet - EtihadPooja KhandwalaОценок пока нет

- Aviation in India - InsightsДокумент24 страницыAviation in India - InsightsDebabratta PandaОценок пока нет

- Air AsiaДокумент20 страницAir AsiaAngela TianОценок пока нет

- C I B A P: Ndian ViationДокумент3 страницыC I B A P: Ndian ViationEshan ShailendraОценок пока нет

- Strategic Management: Industry-Aviation Company - IndigoДокумент27 страницStrategic Management: Industry-Aviation Company - IndigoSatwik GinodiaОценок пока нет

- Airline Sector ReportДокумент33 страницыAirline Sector ReportshraktuОценок пока нет

- SWOT Analysis of Air India Highlights Strengths and Opportunities for GrowthДокумент8 страницSWOT Analysis of Air India Highlights Strengths and Opportunities for GrowthAjay KrishnaОценок пока нет

- Automotive Supply ChainДокумент13 страницAutomotive Supply Chaincoolprashant220% (1)

- ReferenceДокумент29 страницReferenceAbhi ShiqthОценок пока нет

- Business Communication: Sector: AviationДокумент6 страницBusiness Communication: Sector: AviationGunadeep ReddyОценок пока нет

- Challenges Faced by Airlines SectorДокумент2 страницыChallenges Faced by Airlines SectorTanoj PandeyОценок пока нет

- Growing Aviation Industry in IndiaДокумент41 страницаGrowing Aviation Industry in IndiaAastha ChhatwalОценок пока нет

- Biographical Note: Address For CorrespondenceДокумент11 страницBiographical Note: Address For CorrespondenceDebasish BatabyalОценок пока нет

- India's Growing Aviation SectorДокумент3 страницыIndia's Growing Aviation SectorSaransh MahajanОценок пока нет

- Name:-Mousumi Sharma Roll No.: - 08 SUBJECT: - Study of Aviation Sector of IndiaДокумент23 страницыName:-Mousumi Sharma Roll No.: - 08 SUBJECT: - Study of Aviation Sector of IndiaSUDIPTA GHOSHОценок пока нет

- Flag For Inappropriate Content Back To Top Englishchange LanguageДокумент33 страницыFlag For Inappropriate Content Back To Top Englishchange Languageutkarsh gargОценок пока нет

- Indian Aviation SectorДокумент14 страницIndian Aviation SectorSunny RaoОценок пока нет

- A Case Study On Indian Aviation IndustryДокумент7 страницA Case Study On Indian Aviation IndustryManish Singh50% (2)

- Pest Analysis of Tourisum Industry: Political/LegalДокумент14 страницPest Analysis of Tourisum Industry: Political/LegalBhavin MandaliyaОценок пока нет

- Comparison of Indigo & Spicejet AirlinesДокумент30 страницComparison of Indigo & Spicejet AirlinesSubhoshree Goswami50% (2)

- Aviation InsuranceДокумент34 страницыAviation InsuranceAlisha FernandesОценок пока нет

- Marketing Management: Market Analysis of Aviation IndustryДокумент21 страницаMarketing Management: Market Analysis of Aviation IndustryKamal MehtaОценок пока нет

- Industry Analysis Project IndigoДокумент29 страницIndustry Analysis Project IndigopurushottamОценок пока нет

- Airlines IndustryДокумент17 страницAirlines IndustryRITIKAОценок пока нет

- Airport Construction Management: Prof. Abhishek ShrivasДокумент31 страницаAirport Construction Management: Prof. Abhishek Shrivasben hurОценок пока нет

- Open Sky Di IndiaДокумент8 страницOpen Sky Di IndiaDila NoorОценок пока нет

- The Goals For Aviation Sector State Is Aiming at Are As UnderДокумент10 страницThe Goals For Aviation Sector State Is Aiming at Are As UnderPanchal Abhishek JagdishchandraОценок пока нет

- PEST Analysis - AviationДокумент2 страницыPEST Analysis - AviationMansi DhamijaОценок пока нет

- Business Policy - PESTLE Analysis of Aviation IndustryДокумент6 страницBusiness Policy - PESTLE Analysis of Aviation IndustryAbhishek Mishra100% (2)

- Review and Assessment of the Indonesia–Malaysia–Thailand Growth Triangle Economic Corridors: Indonesia Country ReportОт EverandReview and Assessment of the Indonesia–Malaysia–Thailand Growth Triangle Economic Corridors: Indonesia Country ReportОценок пока нет

- Troubled Skylines: Travails of Nigerian Commercial AviationОт EverandTroubled Skylines: Travails of Nigerian Commercial AviationРейтинг: 3 из 5 звезд3/5 (1)

- Policies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportОт EverandPolicies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportОценок пока нет

- Union Government Has Identified 305 Cities and Towns Across 9 States For Implementation of Its FlagshipДокумент2 страницыUnion Government Has Identified 305 Cities and Towns Across 9 States For Implementation of Its FlagshipssoodОценок пока нет

- 10 Taxes You Should Know About - Business Standard NewsДокумент8 страниц10 Taxes You Should Know About - Business Standard NewsAnkaj MohindrooОценок пока нет

- Blockchain in HRДокумент2 страницыBlockchain in HRAnkaj MohindrooОценок пока нет

- Supply Chain Fundamentals Class ScheduleДокумент2 страницыSupply Chain Fundamentals Class ScheduleAnkaj MohindrooОценок пока нет

- Payment BanksДокумент7 страницPayment BanksAnkaj MohindrooОценок пока нет

- Consulting PowerPoint Presentations - 4 Steps - Consultants MindДокумент4 страницыConsulting PowerPoint Presentations - 4 Steps - Consultants MindAnkaj MohindrooОценок пока нет

- Block ChainДокумент1 страницаBlock ChainAnkaj MohindrooОценок пока нет

- UpiДокумент1 страницаUpiAnkaj MohindrooОценок пока нет

- Block ChainДокумент1 страницаBlock ChainAnkaj MohindrooОценок пока нет

- Top 35 News Related To Rbi This Year.Документ3 страницыTop 35 News Related To Rbi This Year.Ankaj MohindrooОценок пока нет

- Supply Chain Fundamentals Class ScheduleДокумент2 страницыSupply Chain Fundamentals Class ScheduleAnkaj MohindrooОценок пока нет

- Final Guidelines For Payment BanksДокумент3 страницыFinal Guidelines For Payment BanksAnkaj MohindrooОценок пока нет

- Asian Banks Must Rethink IT Apr 2014 Tcm80-152209Документ5 страницAsian Banks Must Rethink IT Apr 2014 Tcm80-152209Ankaj MohindrooОценок пока нет

- Bank FraudsДокумент1 страницаBank FraudsAnkaj MohindrooОценок пока нет

- Payment BanksДокумент7 страницPayment BanksAnkaj MohindrooОценок пока нет

- Framework For Dealing With Domestic Systemically Important Banks (D-Sibs) - Draft For CommentsДокумент18 страницFramework For Dealing With Domestic Systemically Important Banks (D-Sibs) - Draft For CommentsAnkaj MohindrooОценок пока нет

- Sourcing ModelsДокумент11 страницSourcing ModelsAnkaj Mohindroo0% (1)

- The Model Dilemma - How Should You Manage Your ProgramДокумент9 страницThe Model Dilemma - How Should You Manage Your ProgramAnkaj MohindrooОценок пока нет

- Outsourcing - Key Legal Issues and Contractual ProtectionsДокумент5 страницOutsourcing - Key Legal Issues and Contractual ProtectionsAnkaj MohindrooОценок пока нет

- Thailand Hazardous Substance Control Act (HSCA) - ChemicalДокумент9 страницThailand Hazardous Substance Control Act (HSCA) - ChemicalAnkaj MohindrooОценок пока нет

- Names of Payment BanksДокумент3 страницыNames of Payment BanksAnkaj MohindrooОценок пока нет

- (Studyplan) RBI Grade B Officers (Preliminary) Objective Phase-I Exam - Booklist, Strategy, Previous Question Paper - MrunalДокумент35 страниц(Studyplan) RBI Grade B Officers (Preliminary) Objective Phase-I Exam - Booklist, Strategy, Previous Question Paper - MrunalAnkaj MohindrooОценок пока нет

- Orissa in 1955: An Agrarian State with Little IndustryДокумент1 страницаOrissa in 1955: An Agrarian State with Little IndustryAnkaj MohindrooОценок пока нет

- Examples of Indian Campus AbroadДокумент3 страницыExamples of Indian Campus AbroadAnkaj MohindrooОценок пока нет

- Keec 109Документ17 страницKeec 109KarthikPrakashОценок пока нет

- Fdi Flows in IndiaДокумент1 страницаFdi Flows in IndiaAnkaj MohindrooОценок пока нет

- Profile of Indian Labour in USДокумент21 страницаProfile of Indian Labour in USAnkaj MohindrooОценок пока нет

- Abstract Mechanical Locks Report 2014Документ2 страницыAbstract Mechanical Locks Report 2014Ankaj MohindrooОценок пока нет

- The Pyramid Principle TrainingДокумент22 страницыThe Pyramid Principle TrainingAnkaj Mohindroo100% (1)

- Shutdown SIS Previous ScreenДокумент2 страницыShutdown SIS Previous ScreenArmando Vara ChavezОценок пока нет

- Maple Leaf Case Study AssignmentДокумент7 страницMaple Leaf Case Study AssignmentafzaalmoinОценок пока нет

- FTECH 4422 - 001 Post-Harvest HandlingДокумент14 страницFTECH 4422 - 001 Post-Harvest HandlingJoann David100% (1)

- Signature Global BlogДокумент2 страницыSignature Global BlogOmkar kumarОценок пока нет

- 03 Comm 308 Final Exam (Fall 2008) SolutionsДокумент16 страниц03 Comm 308 Final Exam (Fall 2008) SolutionsAfafe ElОценок пока нет

- Us Consumer Discretionary Equities PreferenceДокумент52 страницыUs Consumer Discretionary Equities PreferenceTung NgoОценок пока нет

- Joe Mark P. Salvadora BSED FILIPINO 1 Contemporary ACTIVITYДокумент4 страницыJoe Mark P. Salvadora BSED FILIPINO 1 Contemporary ACTIVITYJoe Mark Periabras SalvadoraОценок пока нет

- 1NH18MBA42Документ44 страницы1NH18MBA42Hà NhiОценок пока нет

- Contemporary World FINALДокумент100 страницContemporary World FINALChelsie Pearl OcampoОценок пока нет

- Department of Public Works and Highways: Central OfficeДокумент1 страницаDepartment of Public Works and Highways: Central OfficeEngr'Shemaiah JimenezОценок пока нет

- CRM 4Документ25 страницCRM 4Zankhana BhosleОценок пока нет

- Globalization of Markets and The Internationalization of The FirmДокумент50 страницGlobalization of Markets and The Internationalization of The FirmArif RazaОценок пока нет

- Tutorial 5 Capital BudgetingДокумент5 страницTutorial 5 Capital BudgetingAhmad Azim HazimiОценок пока нет

- Í Qhhoè Genovia Joshuaâââââââ M Ç0) '84zî Mr. Joshua Magbanua GenoviaДокумент3 страницыÍ Qhhoè Genovia Joshuaâââââââ M Ç0) '84zî Mr. Joshua Magbanua GenoviaJoshua M. GenoviaОценок пока нет

- Economics ActivitiesДокумент5 страницEconomics ActivitiesDaisy OrbonОценок пока нет

- DRC-Uganda Cross-Border Road ProjectsДокумент28 страницDRC-Uganda Cross-Border Road ProjectsasdasdОценок пока нет

- India's BOP Crisis: Myths, Paradoxes & External ReformsДокумент72 страницыIndia's BOP Crisis: Myths, Paradoxes & External ReformsNaman SharmaОценок пока нет

- SM (Case Study..)Документ3 страницыSM (Case Study..)gyanesh8375% (4)

- Annual Program Agric Advisory and Services Unit FOR YEAR 2021Документ15 страницAnnual Program Agric Advisory and Services Unit FOR YEAR 2021Rose Asman Samsul BahrinОценок пока нет

- Introduction TeaДокумент2 страницыIntroduction Teaeziest123Оценок пока нет

- Lesson 1 - Contemporary World: Why Do You Need To Study The World?Документ23 страницыLesson 1 - Contemporary World: Why Do You Need To Study The World?RachelleОценок пока нет

- AEON BINH DUONG CANARY CONSTRUCTION SCHEDULEДокумент4 страницыAEON BINH DUONG CANARY CONSTRUCTION SCHEDULELantОценок пока нет

- Economics: Prices and Markets Tutorial: Elasticity: Multiple Choice QuestionsДокумент2 страницыEconomics: Prices and Markets Tutorial: Elasticity: Multiple Choice QuestionsBloss MaromeОценок пока нет

- JDP Introduction - Rev 3 - 04 Dec 2019Документ24 страницыJDP Introduction - Rev 3 - 04 Dec 2019TeatimerobОценок пока нет

- Issue 2 SMДокумент3 страницыIssue 2 SMAlisa AwaludinОценок пока нет

- Computation of Total Income Income From Salary (Chapter IV A) 1696258Документ3 страницыComputation of Total Income Income From Salary (Chapter IV A) 1696258amit22505Оценок пока нет

- Multiple Choice Questions and Answers (MCQ) On Financial MarketДокумент7 страницMultiple Choice Questions and Answers (MCQ) On Financial Marketheena100% (1)

- DISMANTLING AND PACKING OF GE Fr.9E Gas Turbine Plant - Eng ProposalДокумент6 страницDISMANTLING AND PACKING OF GE Fr.9E Gas Turbine Plant - Eng Proposalvarun100% (1)

- Lead QuesДокумент2 страницыLead QuesKameshwara RaoОценок пока нет

- Rani MAJOR Report On ComparativeДокумент41 страницаRani MAJOR Report On ComparativeaksrinivasОценок пока нет